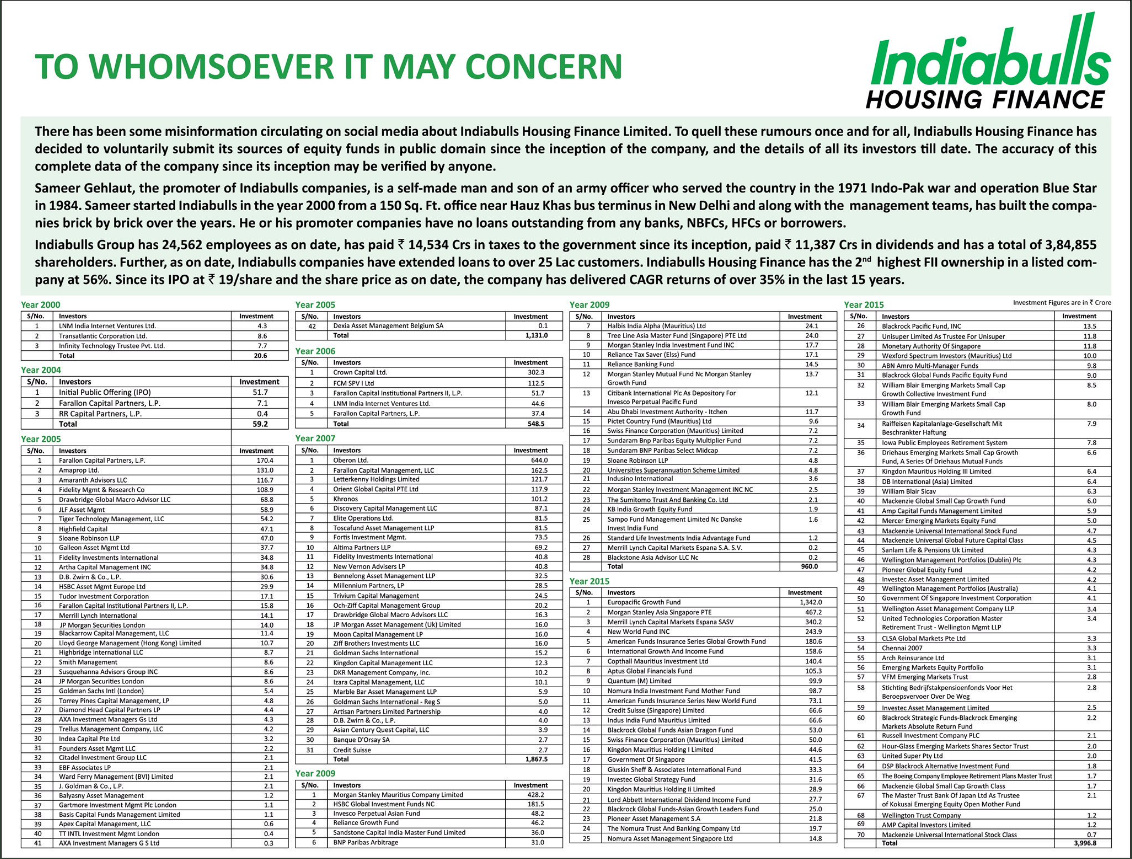

Right. The earlier Supreme Court allegations were made on 8th June. This letter is dated 28th June. I think some of the documents alleging the money laundering, etc probably reached Dr Swamy during this time (i remember IBulls saying that the blackmailers are circulating docs with allegations to multiple govt agencies and politicians) and he is acting based on those very same docs. I went through the letter written by Dr Swamy and there’s no detail at all on any of the allegations except that Congress politicians were in cahoots with the RBI, Min of Corp Affairs and the NHB in the alleged money laundering. Also, some of the language seems a little crazy (“Indiabulls is on the verge of sinking”). Seems far fetched to be honest . Dr Swamy makes a LOT of sensational allegations , many of which never see the light of the day as far as any official action is concerned. Also, the letter is written on 28th June itself but being made public now for some reason?

“Dear Sirs,

This is with reference to Shri Subramanian Swamy’s letter dated June 28th being circulated in social media, alleging embezzlement of more than rupees one lac crores from NHB. We wish to highlight the following facts regarding the same:

Loans outstanding as on date from NHB to Indiabulls Housing is zero.

Indiabulls Housing, in its history, has never taken any loan or refinancing facility from NHB.

The total loan book of Indiabulls Housing is approx. ₹ 87,000 Crores.

The details of companies that are availing refinance facilities from NHB is a matter of record at NHB: https://nhb.org.in/financing_post/refinance-to-housing-finance-companies/

Kindly take the above information on record.”

Mr. Swamy’s letter is likely to give us an opportunity to buy more at cheaper valuations. Other than damaging IBull’s chances of acquiring LVB I don’t see how the letter will have much impact.

May be the charges might be exaggerated, but there are no smoke without fire. Mr Swamy will just not cast allegation without any material evidence and we all also know about the quality of corporate governance and standard of ethics in India bulls.

I have heard people saying that it may turn out to be next DHFL .

Disclosure : Not invested tracking for learning purpose.

politics mixing with business right now. But, I would say this.

previously IBHFL license application was rejected. Not this time around. IBHFL has already formed the management to run the bank and purchased stake in the bank.

Also since IBHFL has applied for bank merger again, I am sure they have done their homework in cleaning their bad footsteps or making things right.

Point 14 of the NHB act does corroborate IBHF’s argument that NHB does not lend to any company in general but only banks and financing institutions for housing activities.

I don’t know if they have gone to NHB or not.

So is it really possible for IBHF to launder 1 lakh crore despite having total debt of 96000 crore at the end of march 2019?

Indiabulls housing management came out with all their borrowing in print to show that they mean what they say but markets are not believing them it seems.

It also has a character certificate of Management as well.

Balance sheet continue to shrink as disbursements of 8k for the quarter are not enough to replace maturing loans and loans that are being sold to pay liabilities.

Company is selling old loans to make new loans as it has trouble borrowing from markets. This cannot continue to for long otherwise there will be no new loans to sell.

Yields are holding at 12%. This is not bad actually as it means company is not holding on to risky loans and selling good ones

Cost of funds is ticking higher as liquidity is tight and funding mix is changing towards high cost debt.

Spreads are narrowing but still good. They have been able to pass on higher costs to borrowers.

Bad loans have gone up. First rise in a number of quarters . This may be interpreted as start of a credit cycle.

With lower balance sheet size, interest income is dropping pushing profits and dividends lower.

Overall, not very good results but given the circumstances, we could have seen even worse results.

Yes result is not good due to circumstances but in this crisis survival is equally important. When we compare results with current valuation, don’t you think it is priced in more than required?

Valuations become secondary when fundamentals are deteriorating. Company is shrinking in size and investors don’t see when is that going to end. On top of that quality of existing book is also going lower. When it comes to valuations, investors (especially analysts and institutional ones) have a tendency to take one quarterly results and extrapolate that to 10 years and value the stock accordingly. It works both ways. when we get few good quarters in a row, valuations go through the roof but when get few bad ones, valuations fall as if there is no bottom.

Unfortunately we are in the downcycle and there no visibility on when the cycle is going to end. Indiabualls also appears to be disproportionately impacted in this cycle as other HFCs (except Dewan and the microcaps) appear to be doing OK or not so badly. Big ones with better credit are doing just fine.

In this business, credit profile of the lender has to be several notches above credit profile of the borrower for the business to be profitable. that is under question now. We have to see IBHL raise a good amount of money from the market (borrowing on the book, not sell down) for the loan book to grow. They keep saying that they are able to raise money from the market (and provide evidence of that as well) however, balance sheet size (both on book and AUM) keeps shrinking.

Stock is not going to see a sustained rally unless there is some improvement in these metrics. Any rally will be short lived. this is going to test patience of investors and some of them will surely run out of it. Housing finance business is going to be here for the long term even for the sub-prime and LAP borrowers.Very viability of the business is not under question but the downcycle was not expected (it never is). Hopefully investors will see light at the end of the tunnel sooner or later.