There is no new clarification nor new complaint … in the one single clarification given by company they mentioned about both complainants …

am not investor here … but people should go for panic selling only on right news… after all its their hard earned money.

A few thing that i found odd/weird about this whole issue :

- Alleging Rs 98000 crore is kind of ridiculous for a balance sheet / Co size of IBHF. Any monetary misappropriations of this size would be practically impossible.

- Plea alleges connivance between directors-mgmt, auditors, rating agencies and govt departments. If these many number of people were involved, very likely that this would have come out much earlier.

- The language used in the plea (as quoted by media outlets) seems quite sensationalist (words like mercilessly, heinously, etc have been used). Looks more like an amateurish attempt at blackmail as the co claims it is.

By doing the LVB deal, IBHF has voluntarily opened its books to deep RBI scrutiny. While the NBFC environment is indeed tight, the Co could easily have survived as a standalone housing finance co at lower growth & profitability. I’d imagine that if there were indeed big issues with their books (in terms of NPAs or anything else for that matter), mgmt would not have done this voluntarily.

The Co has already denied allegations and claims that another person from this racket has already been arrested. On the face of it, i would believe the Co given the ridiculous nature of the allegations but i guess in the short term (till the SC junks the plea), the market will take a “guilty until proven innocent” view on IBHF stock. How long that takes is anybody’s guess. Till such a time, the stock will also remain susceptible to wjhatsapp rumors of all sorts. Unfortunately, they’ve always had murmurs of corporate governance which makes this easier to fear. Something like this wouldnt have dented a HDFC/Kotak Bank/Bajaj Finance kind of pedigree.

Having said that, i think eventually this too shall pass. How long it takes and how low the stock goes based on rumors/updates in the near term is anyone’s guess though.

Just out of curiosity -

Do you think Indian Supreme Court is a place where someone can walk in a place a writ/ special leave petition with absolutely no merit? - I believe if the answer to this question is yes, then India should not be counted as a place to make any sort of investment ever! and if the answer to this question is no, we should ideally see the people behind this in jail for a period longer than they would ever imagine and a penalty that would exceed the amount of money they would have ever thought of amassing.

Disclosure: Existed my position today.

I am not sure as to the procedure but until the SC rules on it, looks like even the most ridiculous pleas can technically be “filed”.

Example : https://newsd.in/ridiculous-pil-sc-dismisses-plea-seeking-ban-on-red-dresses-in-india/

“Amid the long queue of serious cases, came a bizarre plea that left the Chief Justice of India (CJI) red faced. The Supreme Court on Monday dismissed a PIL calling it “ridiculous”. The plea sought a direction to ban all red colored dresses across India.”

If the SC does indeed dismiss this case for lack of any evidence, that would be the end of it. Those knowing more about these procedures can comment further.

I wonder how this Vikas Shekhar guy knows so much about these big scams (33000cr by DHFL and now 98000cr by Indiabulls.) It is also surprising how these announcements come at the right time (after ILFS scam for DHFL and before LVB merger application for IBHF).

You said it correctly that Indiabulls cannot merge with LVB without a detailed scrutiny and audit of their books by RBI and appointed Auditors. Since they have already been denied a banking license before, it becomes even more critical that they keep their books transparent.

My post sounds optimistic because it is clearly visible that the HFC sector is reeling in liquidity crisis as a whole. One cannot go ahead and label every HFC facing the heat of liquidity crisis as a thief. Also, doesn’t mean that they are plain innocent either.

Disc: Not invested.

Govt. Has to take some serious steps against such things…

Otherwise anybody come and blackmail promotors …this is 4th time i guess…

On the otherside if the promoters have done anything wrong than the dudhwala is doing right thing mr.sameer has to go jail…

My personal feeling says sameer gehlots history was not straight forward he has alleged in panama paper and swiss acc and all.

Moreover his lawyer mr.abhisek manu the hawala agent of congress

https://www.bseindia.com/xml-data/corpfiling/AttachLive/549e8fd3-ba10-48a6-a422-cb308460d6a7.pdf

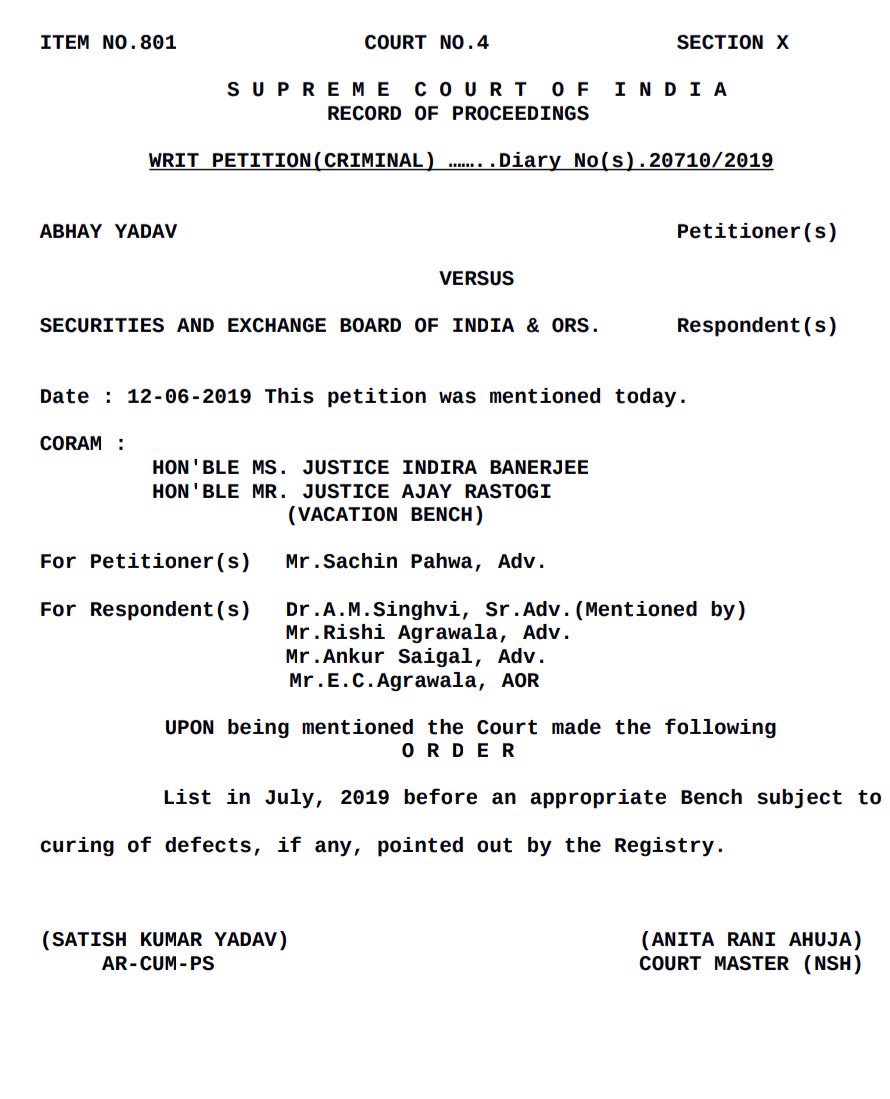

IBHF response to todays events in SC

what does it mean? He has withdrawn the petition and he will come up again? or did i miss anything?

I have no legal background and from my limited understanding of all things legal, I think what it means is that the petition is temporarily halted. The filing says that the petitioner admitted that their petition is defective in nature by which i understood that there is no proof/evidence to back up those claims as of now or at least that the technicalities of filing a genuine SC plea havent been met.

I did a quick search on this topic and it seems such frivolous cases filed in the SC often end up in this state (“petition is defective”) and do not proceed for several years. The filing says that “as and when the petitioner cures the application, the case will be eligible for listing”. However, it seems the SC has tons of cases where such petitions haven’t been cured for years. So this case may well go in that way. Those with a better understanding of the legal system can comment further.

Negative news related to the IB group. A clear cut tax evasion case. If this news is correct, one could safely assume that RBI will throw their merger application with LVB into the dustbin.

For a low NPA, moderately fast growing company that pays 50% of its profits as dividends and has a roe of 20%+, this fall to 1.3 times book value to Rs 530 is a bit hard to explain. Anybody wants to venture a guess?

While it is near-impossible to explain price fluctuations, the share price is a residual value for a debt-leveraged entity, and hence logically, big swings should not be a surprise.

As for paying half of profits as dividends, how is that a good strategy, since on the one hand, you are continuously raising funds, and on the other, paying lots of dividend distribution tax!

Your answer is logical but not very helpful in my view. Many a times the stock price is a leading indicator of the coming company problems.

I highlighted the dividend aspect only as an indication that the books and accounting are probably clean. I agree that it doesn’t seem to be the best capital allocation strategy.

its not a good strategy if you look at it with business point of view, but put yourself in promoters’ shoes, how else would you take out money from the company legally;

-

share buyback : if promoters participate in it and then later raise funds, fund manager would question the promoters’ intention and sustainability of business in long run leading to lower valuations at which funds can be raised.

-

Dividend: a good thing for investors/fund manager,even better for promoters. Investors are happy to receive money indicating existence of cash, fund manager are happy to invest in high dividend yielding business justifying investment, thus increasing the valuation. Promoters are very happy to receive the most of dividend while raising the fund at higher valuations without being questioned.Keep doing it until get caught up in liquidity problems.

What is the overall % of dividends paid vs funds raised or liquidity level?

In the AR, it says the

Company, during FY 2017-18 made a dividend pay-out of 41/- per equity shares (with a total outflow of 2,099 Crores, including Corporate Dividend Tax).

Seems big but for the company which claims to have Liquidity levels of over 15% of loan book which comes to 20K cr having addition few thousand crores will change market perspective?

There seems to be other larger issues plaguing the company!