Sharing the note written for Advisory members about this stock sometime back.

Igarashi Motor India Limited is a Japanese MNC which owns 75% share in the company through another holding company. The company makes various actuators for automobiles and industry.

It is 75% owned by Igarashi Electric Works Limited, a small multi-national company (revenue US$ 300 million) based out of Japan. The Indian listed entity was sold by Igarashi in 2010 (after global financial crisis) to HBL Power Systems. Later it was acquired by Blackstone but within 2 years of acquiring, Blackstone sold it back to Igarashi, Japan at 2X valuation. In 2015, Igarashi bought back 53.84% and rest 21% was owned by P. Mukund, the erstwhile Managing Director of Igarashi, India. In 2019, Igarashi, Japan raised its stake to 75% when they bought back entire stake of Mr. Mukund at Rs. 238.70/-. So, effectively, the complete control of Igarashi India came back in hands of Japanese parent in October 2019, just before the onset of pandemic.

The company till 2019 was mainly a contract manufacturer and supplier for a sub category of Torque Actuator Motors (TAM) known as Electronic Throttle Control (ETC) or Electronic Throttle Valve (ETV). It is a low value critical item which helps in giving consistent output from engine irrespective of ambient temperature, altitude or payload. The business was mostly export oriented and only 20% revenue was derived from India. Due to myriad problems faced by Automotive sector, the company has done miserably over last few years. The chip shortage, delay in new program implementation by OEMs, commodity inflation, belt tightening by Tier 1 OEM vendors affected the company badly. But the automobile demand is unlike many other sector (like a hotel room or an airline seat) — It doesn’t disappear but gets delayed. So, hopefully, when supply situation normalizes, they will possibly start doing well.

But during this challenging period company developed many new electronic valve products in TAM segment, namely, EGR (Exhaust Gas Recirculation), WGA (Waste Gate Actuator), VGT (Variable Geometry Turbocharger), CCV (Coolant Control Valve) and few types of TAM for 2W segment. The uses of the electric motors are increasing in engine management for controlling emission and ensuring ride smoothness.

The other segment where the company is gradually bringing products to market after long cycle of testing and approval from Tier 1 suppliers and OEMs are in Comfort Actuator Motor (CAM) space. The small actuator motors work for seat adjustment, reclining, window shuttering, seat – belt alarm, HVAC management, tailgate opening / closing and similar rider comfort functionalities. The margin and revenue from these products are low now as full range is yet to be rolled out at scale. Also, the competition in this area is higher as criticality involved in these areas are low. But the company expects to increase its market share in both the above segments going ahead due to their large capacity and close association with Tier 1 suppliers like BOSCH (who buys 38% of total TAM and CAM motors made by Igarashi), Vitesco Technologies (16%), Inteva Products (10%), Borg Warner (13%), Dellorto (8%) and few others. Presently they utilise less than 45% capacity in both these segments. Peak utilization level is 80% and most capacities are fungible.

In 2021, they introduced Brushless DC Motors (BLDC) for ceiling fans. From 1st January 2023, energy rating for ceiling fans will be mandatory and BLDC motor reduces power consumption by more than 50% for fans compared to conventional induction motors. For higher end, heavier usage or fancy categories, increased cost is compensated in 2 years. They have already tied up with Crompton, Havells, Usha, V-Guard and few others. They already sold more than 7.5L fans over 2 years through Crompton and supply to others commenced recently. They are in advanced stage of discussion with Orient and Bajaj Electricals. These are imported from China and also made by few unorganized players. In BLDC motor segment, Atomberg makes their own BLDC motors and some other fan manufacturer may also start manufacturing it if the volume picks up. India sells almost 4 cr fans a year and at least 25% fans would be BLDC in next few years.

In other development, company is in last stage of development of two new categories, Electronic Power Brake Valve for 4W and complete Truck Opening and Closing Device (TOCD), which they expect in next 2 years.

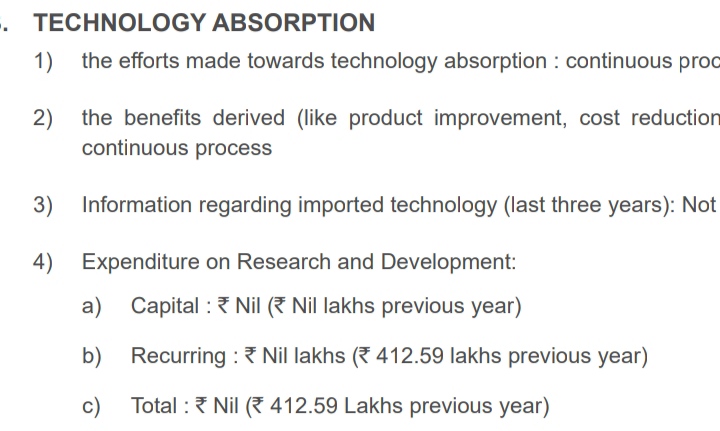

The present financials, in our view, doesn’t reflect the full potential of the company and as the cycle turns, the margin will go back to minimum 15% level. It’s tough to reach the 25% + margin level of 2017 because in those years company sold high margin design and tooling for a few clients. Those opportunities are episodic and comes at peak of a cycle. When the cycle reaches its peak in next upturn, they may (or may not) reach that level. Our valuation is not basing on that.

They are also developing few products for EV segment but those are a long time away.

They route all their overseas sale through the parent company and pay 1.25% composite royalty on this sale. In return, they get complete technical, marketing and after sales support from the parent.

The company, in its recent AGM has said that they expect to reach minimum Rs. 1000 cr revenue latest by 2026 from present Rs. 551 crores and expect a margin of 17% and ROCE of 25%. They are having a net debt of around Rs. 40 cr.

Disclosure: The author is a SEBI Registered Investment Adviser (RIA). The stock has been recommended at a much lower price level to members of www.aveksatequity.com and author is also invested in the stock. Views may be biased. It is not an investment advice. Do your own due diligence if you plan to invest in this company.