Revenue de-grew in the recent quarter, ACs are priced at a premium as compared to market, is that a reason for slow off takes of sales in that category, reviews seem good online.

is anyone tracking it actively? the margins have improved due to reduction in material cost in last quarter. wanted to know if this will be sustainable ?

2 Likes

But they still feel too low in their recent concall they mentioned that not many retailers display their A/C and to get shelf space is an issue, like the management they are very frank and upfront. They are facing competition in 9-10kg segment from LG and samsung.

2 Likes

Detailed q3fy24 inv ppt.

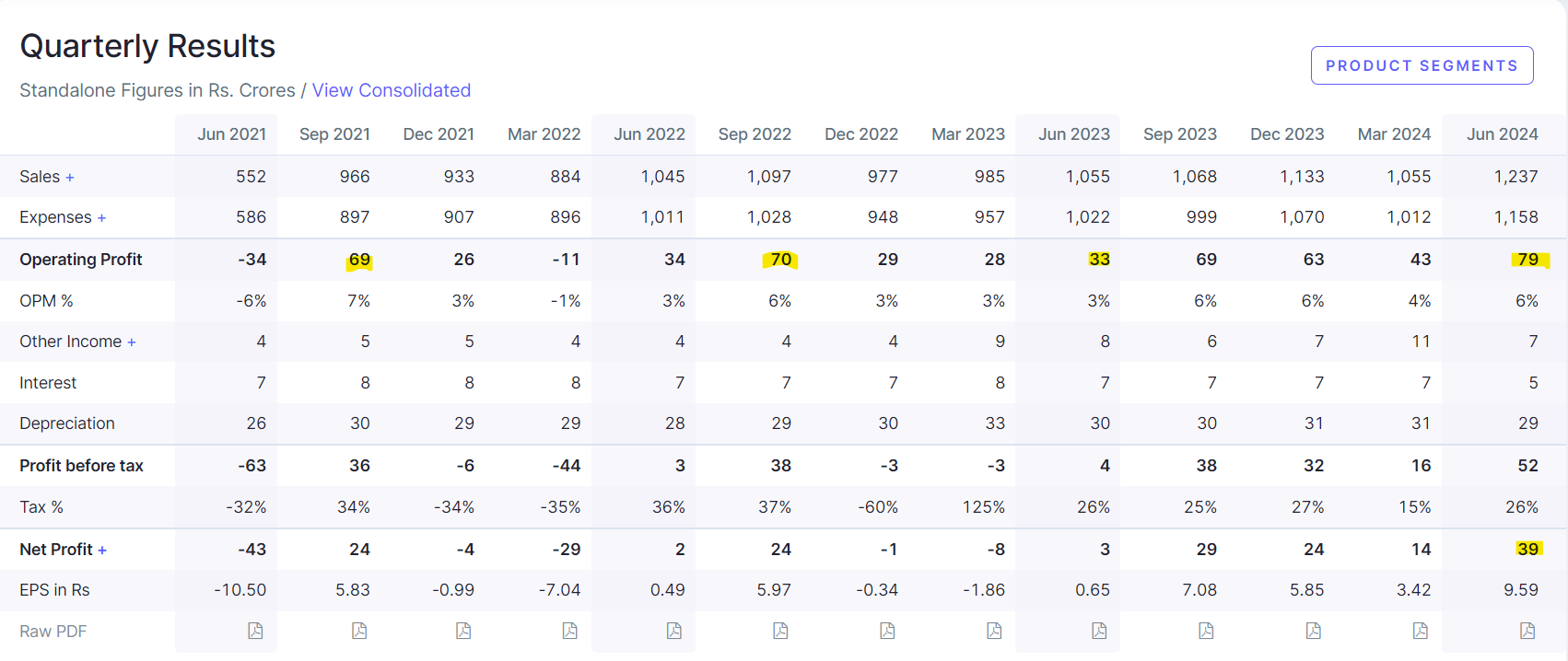

Q1 FY 25E results out.

Best quarterly performance at operational level and net profit level.

Waiting for deck on operational performance

1 Like

IFB Industries Investor presentation notes

- Revenue grew 17% in Q1 FY25 compared to Q1 FY24.

- AC sales were impacted in June '24 due to supply constraints, otherwise revenue growth would have been higher.

- EBITDA grew 113% in Q1 FY25 compared to Q1 FY24.

- EBITDA margin increased by 312 basis points compared to last year.

- EBITDA growth was driven by an increase in gross contribution and control over fixed expenditures.

- EBT and PAT grew significantly by 1376% and 1377% respectively.

- ROCE increased from 4.62% to 23.34%.

Divisional Highlights

Home Appliances : To increase revenue, the Division continues to expand its presence in the channel networks across India through better extraction and by increasing dealer billing count.

Engineering: Marketing strategy has been revisited to achieve an organic growth of 15%. A separate team has been made for M&A in order to achieve further growth.

Steel: Revenue growth will be achieved by way of improved capacity utilization, which will lead to better overhead absorption.

Motors: New project execution will help to boost revenue growth. Commercial production of BLDC appliances motors will be rolled out from FY 25.

- The debt position has further reduced to Rs.38.43Cr. as of July 31st, 2024.

- Total borrowing is of Rs.47.67Cr. which is primarily in the form of Term Loans.Loans were taken for capital expenditures by different divisions.

- As of June 30, 2024, the company had a positive net cash balance of Rs.282.63 crore after considering its total debts of Rs.47.67 crore.

- This positive balance is due to cash and bank balances of Rs.113.24 crore and investments in mutual funds of Rs.217.06 crore.

- Company has invested Rs.97 crore in its refrigeration subsidiary, IFBRL, to establish a state-of-the-art refrigerator plant in Pune. The plant commenced commercial production in May 2023. There Sales volumes have increases from 9,000 units in Q1 FY24 to 90,000 units in Q1 FY25.

- The company aims to achieve a monthly sales volume of 50,000 units by September-October 2024 and expand its OEM business.

Home Appliance Division

- Challenging market for washers, but growth in air conditioners and refrigerators.

- Focus on reducing material, indirect, and fixed costs.

- Introducing new product lines with advanced features to target high-end segments.

- Growth in order bookings for commercial laundry equipment.

- IFB Points is undergoing a redesign and expansion to 462 stores.

- Q2 and Q3 FY25 focus is to launching and expanding its new “Deep Clean Top Load Range”

- Q2 FY25: Launch of new platform configuration for 15 kg washer, 15 kg dryer, and 30 kg dryer.

- Q4 FY25: Introduction of new designs for 30 kg washer and calendar machines.

- Q1 FY26: Launch of stack configuration machines for laundromats.

- They are exporting into market like UAE, Africa, Russia and Exploring opportunities in Sri Lanka, Maldives, and CIS countries.

- There Air Conditioners have shown positive performance in Q1 FY 25 with sales growth compared to the previous quarter and the same period last year. However, the company is facing challenges in meeting sales targets due to supply chain issues and is working on improving inventory management.

Motor Division

- Production of BLDC motors for washing machines and ACs to start by December 2024.Expected financial improvement from FY26 onwards.Focus on cost reduction and new business opportunities.

- Acquiring new customers and developing new products to achieve a minimum monthly turnover of Rs.8 crore and an EBITDA margin of 10%.

- Expanding product range with the production of engine cooling fan motors for Nexon and blower controllers for FATC (Renault, Mahindra, Tata) by Q4 FY 25.

- Developing advanced BLDC motors for various automotive applications (engine cooling, battery cooling, seat ventilation) with expected implementation by Q2 FY 26.

Steel Division

- Sales for Q1 FY25 fell short of the target due to power outages and raw material delays.

- Production increased in June but also missed the target.

- Fine Blanking operations in Kolkata and Bangalore performed well.

1 Like

Anyone invested in this ticker and tracking? Do you see PE of 55 is not justified for 15% YoY growth?

The stock market is often seen as forward-looking, focusing on future expectations rather than past performance. Investors make decisions based on anticipated growth, potential earnings, and future developments, which is why markets react strongly to changes in forecasts, economic indicators, or company updates—essentially to any shift, or “delta,” in expectations.

For IFB Industries Ltd, the company performed well in September and October 2024, running at full capacity and facing a stock-out situation. This stock out situation arose due to inadequate planning and delays in procuring critical components from China, which disrupted their supply chain and limited their ability to meet demand.

Looking ahead, they have witnessed a very good demand for washers in the month of November. December is projected to see an increase in stocking of air conditioners (a low-margin product) by the dealers. For Q3 FY 2025, IFB anticipates margins in the high single digits. By Q4, the company expects to achieve the margin levels they had previously forecasted.

Regarding supply chain challenges, the management acknowledged that they need some better visibility on projected sales from market so that they can plan supply chain. Sometime parts are imported wherein there is a lead time of 90 days. They need better integration between front end and back end. Also, some IT integration is needed in supply chain. Management in their latest concall said that they are working on that.

Disc - Invested

2 Likes

Engineering division is targeting 30% growth over two years and plans to diversify beyond automotive and company remains focused on boosting technology-led products and maintaining competitive pricing, especially aiming for increased market share in ACs (targeting 5%) and refrigerators (targeting 7%). Plus the Boost from GST Reforms 2.0

2 Likes