No that’s the excess cash that was in the AMC, that is on top of the 4,500cr is my reading. So shareholders will get 4,750cr but I haven’t included it in my calculations.

1 Like

Now what would be the final cash post tax that will be with IDFC?

500 crores was cash reserves out of which 250 crores given as dividend

Out of 4.5k crores what will be applicable tax?

They have announced dividend of 250 crores. For roughly 160crs share it is only 160crores dividend. Where is other 90 crores will go?

“BFHL managing director Karni S Arha said the acquisition is expected to be completed in the next 9-12 months after getting all the regulatory approvals. “The completion of the acquisition will take time as all the consortium members will have to get these approvals individually,” Arha told FE.”

The time for completion of AMC sale itself is 9-12 months. Reverse merger would take another year. This is going to be a long long wait. Maybe time period for deal completion is one of the reason why stock price is not going anywhere close to its actual worth.

3 Likes

In hindsight, for those of us who have invested in IDFC Limited for IDFC First Bank’s story/shares, It would have been better to shift to IDFC First Bank few days back when price of IDFC Limited was 1.65 times the stock price of the Bank…I dont think we are going to get a better swap ratio than that if merger takes so much time as by then Bank’s stock price will run up a lot and that will impact swap ratio negatively for IDFC Limited shareholders…we will probably pay the price for lethargic management of the holding company which cared for their own salaries only.

4 Likes

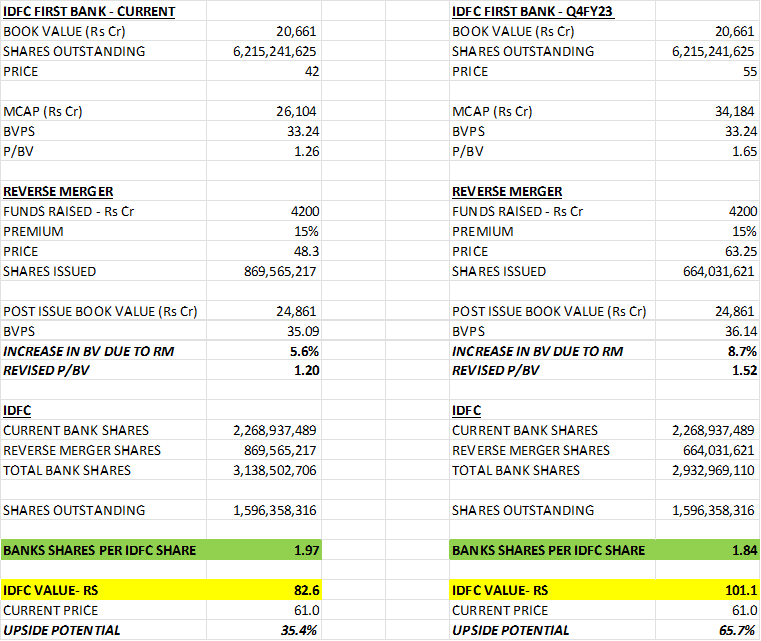

These are my revised workings for both IDFC and IDFCB. First scenario is based on the current price and the other is based on a price of Rs 55 for IDFCB which is what I am assuming the price might be at the time of the reverse merger closer to the end of this financial year. For the AMC the value is post-tax; we know that Rs 2,500cr was the indexed value for the AMC in Jan, 2020; I have assumed this is now Rs 2,800cr and the LTCG rate is 20%. Also assuming that shares for the AMC cash are issued at a 15% premium to the prevailing price.

The reverse merger is clearly beneficial to both set of shareholders with the book value per share going up by almost 9% in the second scenario.

4 Likes

Don’t you think assuming a stock price of 55 for the Bank at the time of merger is too pessimistic/optimistic depending upon which one of the twins one holds in his/her portfolio…??

.

In my view bank can make 2000 crores of profits next year and can trade at P/B of 2.5 to 3 atleast by the time of merger…that would translate to a price in the range of 80-90 by the time of merger…

1 Like

Yes it well might but for my analysis I just assumed a 20% higher price than today.

1 Like

Which site it is?it’s very clear info

Looks like Value Research.

1 Like

That seems like sizeable buying; any idea what the current mutual fund ownership is now vs last quarter?

HDFC Group ownership upto 5% in IDFC now. Trustee+Insurance

Also Mutual funds owning the stock up from 11 to 21 with ownership increasing to 9.63% from 4.73% in December.

March-

December-

3 Likes

RBI has just given its No-objection to the Equitas - Equitas SFB merger, filing here- https://www.bseindia.com/xml-data/corpfiling/AttachLive/4e7fffc2-2e21-4c89-b496-5d7d283163f9.pdf

What’s interesting is that RBI is alright with the Foundation that sits under Equitas Holdco being transferred to the SFB. This means that IDFC doesn’t necessarily need to get rid of its foundation prior to the merger. VV had clearly mentioned this was the main remaining holdup to the reverse merger process.

5 Likes

This is indeed a great development, removes the last hurdle for the merger. IDFC Ltd has a board meeting next Friday to finalize their results, hopefully they are able to agree the merger terms and announce the merger the same day. Shouldn’t be too difficult especially if the HDFC Group was able to finalise its merger over a weekend!

1 Like

Dont think they’ll take a call on reverse merger until the amc sale is closed plus idfc foundation is sorted

AMC sale is closed and they can go ahead with the reverse merger without selling the foundation as clarified by the RBI.

Deal is closed as binding offers have been recieved and deal amounts decided which is what is needed for the reverse merger to go ahead. Do study the Equitas Merger, they too are selling their technology subsidiary where regulatory and other approvals are still pending yet the reverse merger is progressing. They have decided the swap ratios and even recieved in principle approval from RBI recently. IDFC and IDFCF can go ahead with the reverse merger today if they want, there is nothing holding them back anymore.

3 Likes

Hi,

If possible, Can you please share probable reasons why IDFC is not making progress on merger front…,Atleast From VV’s one interview we can be sure IDFCB is quite open for merger any day.

They probably are discussing it which is why this week’s board meeting is going to be interesting as for all your know the announcement might come then.

1 Like

Merger is not speedy because of drag from either or both ends.

The drag from the banks end is logical, because in the next one year one expects four levers to come into action, for which the banks management had been planning for years prior to covid. Anyone following banks’ progress closely will agree.

All of the following four points will cause an unprecedented growth in EPS for the bank:

*Provisioning is going to reduce, post covid. Management had given this guidance earlier and we see it happen in this quarter. And possibly Toll Road provisioning is likely to be reversed.

*Operational expense are going to be lesser. Management has said it won’t grow branches as aggressively. And in-house credit card team expense is mostly done.

*NIMs are going to be better. The expected drag due to high cost borrowings wont give as much drag as earlier calculated due to higher interest rates regime.

*most importantly, the management is going to focus on loan book growth.

All of these are already in effect, due to which we will see EPS spike. Then would it not favor the shareholders of the bank to delay the merger by a whole year at least, and let these levers kick-in, and get a better bargain?

10 Likes