I dunno if it will be same with idfc… but with Vodafone what I noticed was … especially at lower prices ie sub 6. A lot of people used to leverage a huge quantity of shares and buy and sell at 0.05 on nse. Ie they used to buy at 4 and sell at 4.05/sell at 4.05 and buy at 4 for a cool profit all day long. Maybe the same is currently happening with idfc since it’s cheap and has huge liquidity and is range bound. Could be anything but I’d bet it’s that. Happened with ncc too earlier.

5 Likes

I know that stocks connected to finance look a bad bet with impending npas etc on the way but here’s my list of reasons why imo even in the short term idfc looks good. There’s no secret that everyone is expecting npas everywhere to increase in September so its a matter of who shows the least npas and who shows the most hope over the next few months. While other banks and nbfcs are priced at high P/Es idfc is priced at below its book value. So firstly expectations are not high for idfc. For the other banks and nbfcs they need to outperform to justify their PEs. If they don’t do that in September then they fall since they need to be revaluated to justify slower future growth. Idfc just needs to show it’s capability to survive since it’s not rated at all considering its current valuation so the only thing that will cause it to crash is if it looks like it’s going bankrupt.

They’ve already prepared for these quarters by

- Keeping a huge amount of provisions over and above what the RBI recommended

- Raising equity capital of 2000 crore in may to strengthen capital adequacy to 15.5 percent

- Being the only bank that offers saving accounts at 7 percent interest and one of the few banks that allows you to open an account purely online and without any visits to the banks required

- Less reliance on wholesale loans as compared to a few quarters ago

- They have already got the revenues. Infact their interest income is just half of kotak Mahindra. So while other small banks still need to worry about growing idfc just need to worry about cleaning their books and making profits without worrying about revenue increase and top line growth.

- Catering to a huge amount of rural population who deal in jobs connected to needs not wants ie travel/entertainment (This point is just my personal view. All the 4 above are based on facts).

I can see a financial crash happening in a few months… I think everyone can and hence why financials have barely risen… however, I also see people rushing towards stocks which show any sign of good news. And a bank that offers safety in high provisions and capital adequacy and increasing customers due to its high interest rates and use of technology which is priced at under its book value seems a safe bet.

Disclosure: bought at around 19 with the above logic and it makes up a huge percentage of my portfolio. Will be keeping a close eye on management commentary post the next quarter to make sure the story above continues unfolding. Will exit if I find it doesn’t and take a position again later.

17 Likes

If anyone wants to see how this works ie Volume greater than a Crore yet a slow rise(it’s pretty fascinating) open money control and open idfc first bank. Firstly look at the volumes… as usual they are huge. It’s because a LOT of people are using leverage to buy stocks for intraday. Hence why you’ll see the delivery is always around 20 percent and below too. Then look at the very predictable graph. On nse idfc goes up from 26.3 to 26.35 or falls to 26.25. once it reaches those levels it stabilises. So what these intraday traders do is they buy a ton of stock via leverage at 26.3 and sell at 26.35. and they keep a stop loss of 26.24. it’s that simple. If you do this through out the day you win more than you lose easily. This is what they do with any stock that has high volume and is cheap. On bull days they buy and one bear days they sell. Overall it’s harmless since the stock moves up or down long term independant of this… but long term owners can get frustrated looking at the high volumes/low delivery/slow movement. So understanding this makes it easier to hold too.

Note: I know this because Ive sold stocks in frustration before due to it. Once I understood what was going on i stopped getting annoyed or frustrated. Btw Once idfc first bank reaches a new high ie above 28 or so they’ll start short selling(and you’ll see the money control forums plagued with sell spam).

15 Likes

The bank has released its Annual Report.

I am adding a few summary points from first few pages of the AR. I will not cover the numbers a lot because they are already very well covered in all aspects on the thread (and if not would be covered by others too). My focus would be on the softer aspects of the bank and I will seek to learn all I can from this AR. All pages are in terms of pages of pdf.

- [Page 17] All scheduled banks are required to lend 40% of their loans to Priority sectors. IDFC First bank conservatively displays their Retalization of funded assets as 54% and adds as a footnote that including PSL certificates they hold, the retail assets are 61% of the entire book. The annual report seems to be written and presented in a conservative way.

- [Page 23] More instances of conservative accounting: VV: “In Q4 FY19, it came to light that two of our legacy wholesale banking accounts, Dewan Housing and Reliance Capital, where we had exposures of 1,784 crore, were in financial trouble. Though technically they were not yet NPA, we came forward and told the shareholders things as they stood, we did not hide behind client confidentiality or technicalities. We provided 15% of such principal exposure to the P&L and posted a pre-tax loss of

417 crore in Q4 FY19. In the next quarter (Q1 FY20), their condition deteriorated significantly. We promptly recognised these issues on our books in Q1 FY20, and took the total provision to1,097 crore, or 75% of then principal outstanding, which we believed was an appropriate market value for these bonds. We subsequently sold part of these exposures in the market at similar valuations so our estimate on valuation was correct.“ - [Page 24] On the increasing CASA: “So what did we do with 20,710 crore of Retail Deposits we raised during the last financial year? You might think we lent it out as any bank would. But no! We used this money to straightaway reduce our borrowings through Certificate of Deposits (CD). Retail Deposits are highly diversified across millions of customers and are stable, while CDs are low-cost short-term borrowings with tenures generally between 30 days to 180 days and usually subscribed by the Mutual Funds. The liabilities side of the Bank became very stable because of this swap we did during the last financial year”

- [page 25]: On Culture: “ For instance, when recently one private sector bank was in the news for wrong reasons, I wrote a mail to all our employees asking them not to chase down that bank’s customers to move their deposits to us, and not to talk ill about that bank or about any other bank for that matter. If you have to comment, respect other banks for their work. “

- [Page 26]: On Growth: “I agree we have not grown the overall loan book last year. It’s deliberate. Because as mentioned earlier, on the liability side we had low CASA ratio at merger. If we continue to grow the loan book, then this issue of low CASA ratio and low Retail Deposits % will never get fixed. I see it as my responsibility to get all our foundations firmly in place before we start growing the loan book, and retail liabilities is one of the foundational items for a bank.“

- [Page 26]: On safety first: “It is not without reason that CRISIL, India’s premier rating agency has evaluated and rated our fixed deposit programme FAAA, which is the rating category indicating highest degree of safety.“

- [Page 27]: Covid 19 impact: “During April and May 2020, our incremental lending volumes were practically nothing. Our book growth is therefore stalled this quarter. But as things begin to normalise, people will begin consuming again. We are beginning to see that consumption businesses like personal credit, two wheelers etc. have already picked up to about 50-70% of pre-COVID-19 volumes, where ever lockdown is lifted. Demand in SME lending is still low, say 20% of pre-COVID-19 levels. My sense is that we have lost about one year of book growth. Once we see through this phase, then India will be back to its growth phase, and we will be back to our growth ways. We provided moratorium to almost all customers who requested for it. Right now we are actively reaching customers and providing them funding under the Emergency Credit Line Guarantee Scheme from the GOI.“

- [Page 27]: why 7% interest makes sense: “Our Bank has a unique history because of two lending institutions merging with each other. Capital First’s borrowing cost for Q2 FY19 (quarter prior to the merger) was ~ 8.5%. IDFC Limited borrowings, specifically pertaining to infrastructure and long-term bonds that were transferred into IDFC Bank at de-merger, were at ~ 8.9%. Together, including some other similar borrowings, we are servicing ` 43,875 crore (as of March 31, 2020) of such borrowings at ~ 8.6% anyway. Hence seen in this light, 7% is pretty inexpensive money for us and is a positive trade for the Bank! Further, the business lines we have chosen for incremental lending comfortably support these rates.”

- [Page 27]: Creating Value: “The sandbox was very simple - the pitch was that significant value can be created if we can (a) create Intellectual Property (b) build a scalable business © grow at 25% (d) generate ROE of 16-18%, and support it by exceptional corporate governance. When I reflect on this sheet now, many years later, I find the word Customer Experience missing in this theme though, which is something I would fix if I were to remake this sheet today; I’d place the Customer Experience at the center of this sheet.“

- [Page 28]: On RoE: “I believe one of the core value drivers will be to have a certain level of profitability which comes blindfolded; i.e. it is in-built in our business model. Meaning the Core NII plus Core fees minus Normalised credit losses should take us to 16%-18% core return on equity. Core means not having sporadic one-time incomes from rainmakers. “

- [Page 29]: On customer experience anecdotes: “On one occasion, our customer, a respected septuagenarian, called us one day at the contact center, expressing urgency for his wife’s operation to be done, and needed cash urgently at the hospital. Our customer service executive reached out to the nearest Ahmedabad branch executive, who carried the FD liquidation form to customer at the hospital, and delivered cash at the hospital. The customer’s wife’s operation was successful and customer was thrilled. “

- [Page 29]: On CEO’s stake sale: “ I had purchased ESOP stocks on leverage in 2017, and was holding on to it since two years, and in March 2020, had exercised more options and wanted to hold it for four or five years as I was confident of what we are building. I thought that if held for longer period of time, substantial value can be created and I could square the position after a few years. In other words, I thought I could beat the cost of debt by appreciation in the stock. I had earlier leveraged the Capital First buyout successfully; i.e. leveraging the buyout and holding on to the stock for 6-7 years, and was following the same path. But COVID-19 waylaid the best laid plans, and margin calls were triggered. Also, the trading window was closing soon for Q4 FY20 quarterly results and trade by lenders would not be in order. It is my regret that I had to sell the stake under these circumstances. I hope the buyer, on the day I did the sale at COVID-19 prices, makes good returns.”

- [Page 40]: On covid related innovations: “The Bank also launched video KYC for its online Savings Accounts opening journey. The start-to-finish digital journey made Savings Account opening a delight, as it enabled customers to complete the paperless KYC process and avail industry’s best interest rates on savings balances. The zero contact method completely does away with paper work or biometric verification, thereby removing physical interaction between the Bank and customer from the KYC process”

- [Page 41]: “The Business Continuity Management (BCM) team is the second line of defence team that among other governance activities proactively monitors for potential threats. The BCM team kept track of the disease – COVID-19, as it initially developed into an epidemic and spread slowly outside of Wuhan - to the rest of China and subsequently outside of China. The team quickly assessed the potential of the disease to become a pandemic and spread across countries and continents and to India based on the trade, student exchange across the two countries as well as from other international travelers visiting India. As a result, BCM proactively sent the first Staff Advisory on January 22, 2020, much earlier than we saw any news of it in the Indian media or any advisory from the authorities.“

23 Likes

Cheers @sahil_vi … I’ve reached the point wherein I know these banks financials by heart lol so I was very interested in the management commentary more than anything else. The honesty pouring through that AR was unbelievable. After skimming through most of the AR What I’m convinced about is

- The bank is safe due to how conservative they are being.

- There will be no growth seen for a long time… which is fine… since tbh all that I want to see is cleaner books and safety first which looks like the priority

- Honesty… V.V. basically admitted no growth for a year and that their business was nil in May and loans are just 20 percent at present. While those figures look low atleast they wont come as a shock now. All estimates will be adjusted accordingly

- 7 percent savings accounts look safe for the foreseeable… when covid hit I was hoping they wouldnt change what would be one of their main draws and by the looks of it 7 percent is going nowhere

Overall as an investor I’m very happy. This bank makes me realise why the management is more important than anything else. On paper it’s a loss making stressed bank… but when you do a deep dive and understand the management and their vision it all makes sense. This is the only stock I’ve ever owned that doesn’t have EPS lol. Anyway, from now on I won’t live in fear and will use any more dips as opportunities to buy more. Cheers

16 Likes

Continuing with my AR summarization (this time with a few points also having some commentary, specially where I’m concerned):

- [Page 46]: On Moratorium: “As the COVID-19 pandemic disrupted livelihoods and businesses in overwhelming proportions, the Bank recognised that moratorium was a means to ease liquidity concerns of borrowers and was key to sustainability of their businesses. Towards this, the Bank proactively communicated all necessary information related to moratorium to borrowers, through its website, SMSs, emails, social media and through conversations with its customer service teams. The process of availing moratorium was simplified by the Bank by enabling customers to apply digitally through multiple channels: website, SMS, email, phone banking and social media as well. The Bank’s online reputation management and customer service teams worked round-the-clock to respond to customer queries and ease their apprehensions.“

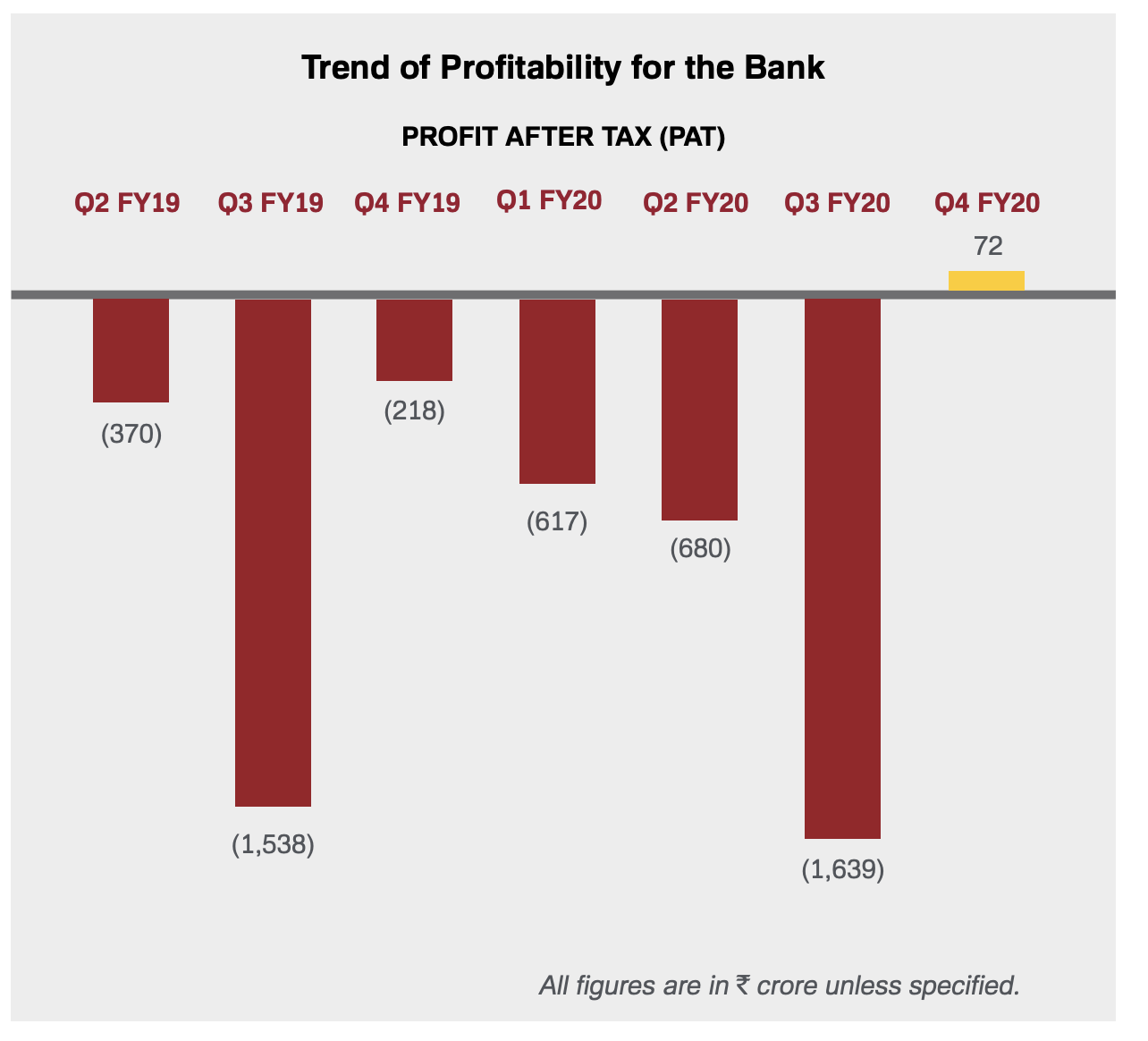

- [Page 75]: the bank completely discloses its myriad of ‘1 time problems’ that have slowly eroded its book value per share from Rs 38 in Q2-19 to 31 in Q4-20:

-

[Page 78]: As of March 31, 2020 after considering the moratorium impact, the Gross NPA % of the Retail Loan Book was at 1.77% (as compared to 2.26% as of December 31, 2019) and Net NPA % of the Retail Loan Book of the Bank was at 0.67% (as compared to 1.06% as of December 31, 2019). The Figures for the March 2020 include the benefit of the moratorium granted as per the RBI notification where the overdue accounts which might have slipped to become NPA in March 2020, have not been considered while computing the NPA figures as they have been granted moratorium and put under standstill status during the entire moratorium period. Even without such benefits in the computation of the NPA, the Gross and Net NPA of the Retail Loan Book of the Bank would have been stable at 2.22% and 0.99% respectively, lesser than the NPA figures as of December 31, 2019

-

[Page 79] “The Cost to Income Ratio (excluding Trading Gain) has improved to 76.54% in Q4 FY20 as compared to 80.68% in Q4 FY19.”

Sahil: This is one clear area for the bank to work and improve upon. We should not expect this to come down in next few quarters as the bank scales up the number of its physical branches, hires more employees to staff them. But once this expansion has finished, a further jump in earnings could be expected as the Cost to Income ratio Comes down. -

[Page 79]: On taking pro-active provisions: “ Following the RBI guidelines as provided in the notification as on April 17, 2020, the Bank was required to make COVID-19 related provision of 25 crore pertaining to accounts where asset classification benefit was given which was supposed to be distributed across Q4 FY20 and Q1 FY21. However, the Bank has provided the entire amount in Q4 FY20 itself. The Bank additionally took 200 crore of COVID-19 related provisioning proactively for over-dues of 1-89 days as of 29 February, 2020 taking total COVID-19 provisions to 225 crore.”

-

[Page 80]: On Digital banking: “ The Bank recently launched watch banking, which enables customers to access their bank account and transact on their smart watch. The Bank’s digital platforms are easy to use and transact; 70% of the Bank’s active customer base is regularly transacting on various digital platforms. “

-

[Page 81]: “Mutual funds – With IDFC FIRST Bank mobile app, customers can invest in SIPs and lumpsum purchases online. The Bank also provides a list of recommended funds to choose from and help customers invest wisely. Further, user onboarding and investment account creation is instantaneous and online.”

Sahil: Does anyone know whether IDFC First bank offers direct or regular mutual funds? If it is regular funds, should we expect some small distributor-fee to come up in the bottomline? -

[Page 81]: “The Bank offers secured working capital facility under Kisan Credit Card (KCC) scheme to customers/ farmers involved in agricultural activities. The credit assessment is based on the cropping pattern, credit bureau and reference checks as well as legal and technical valuation of the security. This facility provides adequate and timely credit for crop cultivation, harvest expenses, machinery maintenance and household consumption. “

-

[Page 82]: Fintech innovation: “During FY20, our Bank embraced the fintech ecosystem through partnership with industry-leading players to make new and innovative credit products available for the masses. The partnership with Flipkart for its PayLater product enabling millions of customers across India gain access to credit, to fund their purchases in a most convenient manner. The Bank also enabled its customers with pre-approved loans to utilise this limit for funding purchases from various online and offline merchants”

-

[Page 83]: On corporate banking: “You will be pleased to know that the credit rating threshold for initiating a relationship with the Bank continues to be in a healthy zone with most of the business being initiated with the better performing Investment grade corporates. “

Sahil: The part about most of the businesses having investment grade among those that get loans from IDFCF worries me. I understand that bank could make more money by lending to below investment grade companies, but this is exactly the kind of shit-bomb that exploded in Yes bank’s face. I will certainly try to ask the management about this in the AGM if they allow me to.

8 Likes

Can you please explain why is that a worry? Dealing with only investment grade companies is actually a good thing, right?

1 Like

They dont just deal with investment grade companies. Most of the companies are investment grade.

Technically that means >50% companies are investment grade. My questions are:

- What is the real percent? Is it close to 50% or 90% or 95%?

- Why is it not 100%? is it the case that some loans the bank disbursed were to investment grade companies which then became non-investment grade?

- does the bank disburse loans to non investment grade companies as well?

- If the answer to above is yes, then why? Are these legacy loans and what is the policy going forward?

5 Likes

Investment grade is the minimum rating grade required to get finance from lending institutions. This grade can be managed easily by borderline corporates and get the rating agencies to give them investment grade. This in no way should be considered as safe. Even AAA rating is not foolproof.

Indian corporate (especially small and medium) debt market is more of a rollover game. If new funds not coming in…most of them will default. In street language it is “iski topi uske sar”

As long as new funds are coming the system will work. If new funds (rollover) stops… defaults will be high.

Disc. Invested in IDFC (parent)

4 Likes

Two factors are in vital for loan repayments. ‘Ability to pay’ and even more importantly the ‘intention to pay’. The loan executives know about both the factors. In public sector banks it had turned into an open loot through conspiracy with large numbers of branch managers, regional managers and general managers and MDs themselves were compromised. In private banks it is not possible unless the top management itself gets involved. That is why the integrity and competency of the top man is so important.

7 Likes

This is good news for IDFC bank.

Hoping they are paying dues in FIFO manner. Does anyone know when IDFC is due for payment?

It’s more of an annual sort of a payment as far as I know(Not sure though) ,VV mentioned in one of his interviews .

IDFC has received payment for this year I believe.

1 Like

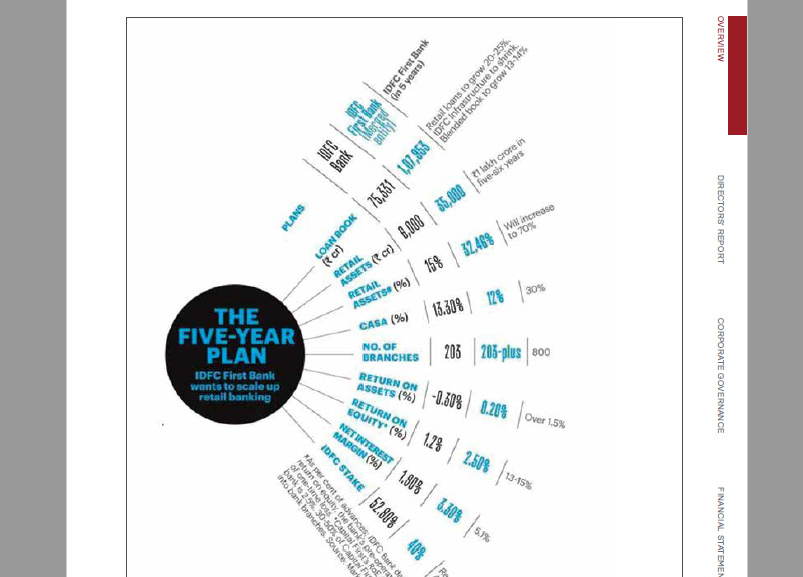

I was trying to do some valuation on this. Going by thr 5-yr plans, it seems the bank will have earnings of arnd Rs. 2000 crs. in 5-6 yrs from now.

A conservative multiple of 15 on that gives mkt cap. of Rs. 30,000 crs. so the IRR from current market cap comes out to be arnd 15%.

Given the risks of leverage and looming slowdown, isn’t this IRR less? Thoughts invited

1 Like

The earnings of 2,000 cr after 5 years seem too low as per my calculations. Can you please show your calculations for this?

Note that the bank already has 6,000 cr of NII with an improving cost to income ratio and improving balance sheet health. As per my calculations, a more realistic expectation for the earnings would be 3,000 to 4,000 cr.

3 Likes

The biggest factor for equity valuations is the introduction of an effective corona vaccine and how soon it is made available. I have a feeling that the economy will experience a boom for a couple of years as a huge amount of pent up demand would be released including travel, tourism and family and friends reunions apart from manufactured goods. As far as IDFC first is concerned, considering their performance in last 1 year, I feel that the bank should achieve their 5 year target in roughly 3 years or so.

1 Like

@sahil_vi : -

I estimated this from their AR '18-19 where they’ve laid out their 5-yr-plan. It mentioned Retail Assets to grow to 1 lakh crs. in 5 yrs and it will be 70% of total book. Thus, total Assets in 5-6 yrs. = 1,42,000 crs. (approx.). On this thr targeted ROA is ~ 1.5% thus 1.5% of 1,42,000 = approx. 2100 crs. including the provisions. Thus, I reached rough guess for Rs. 2000 crs.

Vl be glad to hear ur views on wat’s incomplete\missing in this.

1 Like

Price to Book is a better metric to value Banks/NBFCs. I expect P/B to go from 1x currently to atleast 3-5x as they start showing profit.

2 Likes

You are assuming that the loan book is the total assets which ofcourse is not the case. Better way to look at it would be through the ROE target of 13-15% in five years. The book value today is around 17300cr and close to 19000cr if we assume that Vodafone provision gets written back. To get a 15% ROE on this book value we we would require net profits of roughly 2900cr today. In five years the book would have grown, suppose we assume for simplicity it grows at 8-10% every year it will be roughly 50% higher at around 28000cr, so a 15% ROE would mean 4200cr in net profits.

1 Like

Thanks for sharing. This helps a lot.

The 4 critical numbers for your calculations are:

- RoA : 1.5%

- Retail assets (as a % of all assets): 70%

- Total assets: 1,42,000 cr

- MarketCap/NI of 15

on 1. you would agree on 2 things: the bank guided for CASA of 30% after 5 years and “RoA above 1.5%”. The bank has already achieved CASA of 30% after 1 year. I think the 1.5% RoA estimate is an underestimate. I would expect RoA to be closer to 2% after 5 years.

on 2. from 37% retail assets in 2018-2019, the bank is already at 61% of assets being retail assets. clearly, the trajectory is much faster than the very conservative estimates which were provided in 2018-2019.

3. Assuming a 20% CAGR for the retail assets, we would reach something like 1,35,000 cr retail assets in 4 more years. Of course, nothing stops them to stay at 70% of assets being retail. I fully expect this to be close to or maybe even above 80% in the future. Assuming 80%, we get total assets to be 1,68,000 cr. This gives us a NI of 3400cr.

4. Even at this trough of earnings represented by corona-impaired financial system, HDFC bank has a multiple of 19 on it’s NI. IDFC being much smaller and in growth phase, i think a multiple of 20 is reasonable.

This gives us a expected market cap of 68,000 cr, from roughly 15,000 cr right now. this gives a CAGR of 46%.

As you can see, valuation is not an easy game to play. The numbers could very well turn out to be somewhere close to what you have suggested, but i doubt that because the bank is achieving some of its 5 year targets after 1 year itself.

Each investor must do a valuation exercise they are comfortable in to understand how much CAGR they expect in future.

Disc: IDFCFB is my largest direct stock holding. I had written a short investment thesis some time ago: https://bit.ly/idfc-first-bank-sahil-investment-thesis please feel free to read this to better understand why i am so bullish on this company.

10 Likes