3 Likes

He could have shown more profit by making 25cr provisions for covid19 impact as required by RBI and could have shown 275cr profits,instead he provided 200crs avore and above requirement of RBI for covid19 provisions .

1 Like

IDFC First Bank - Stock Analysis:

4 Likes

As mentioned above its now increasingly looking like Vodafone Idea will survive and the Google investment might be related to the ncds that mature in July. A 1600cr write back will take up CET to 17% and that is very high for a bank with just a 10% unsecured book. Bandhan Bank with a 90-100% unsecured book has a CET of around 23% and trades at 3x BV. If this happens IDFCB should trade close to atleast existing BV of Rs30 (excluding any Voda write back) and yet still have a provision buffer of 1600cr.

2 Likes

This will happen, if Google comes with all guns blazing and clean the entire balance sheet including AGR dues. 5% stake will not make any good to Google as the valuations go up for further increase. Idea presence is required to manage the Indian market. I waiting for official confirmation.

In banking stocks, I fail to see a better investment opportunity than IDFC first. It looks like a good prospect from every angle. The stock price will be limited by the size of equity. However it will not influence the direction. It is long term investment. Around three to five years.

Guys, Please see the risk also… Don’t go by the CEO’s interviews only. How do you know the quality of lending? If someone just sees the track record, it is always negative results with forward looking positive comments by THE man. I agree, he has tried to front load the bad news and blame legacy issues so that he can have a clean run in the next 3-5 years… But, let’s wait for a couple of quarters and then say this.

Discl:

Invested in IDFC (parent)

4 Likes

Saying “it’s always negative results” isn’t seeing the whole picture. One has to look at Why ? Why negative results .

This is because IDFC bank have said they are aggressively after growth. Number of bank branches have grown from 242 to 463 in last 1 year alone. The new 221 branch is all cost from employee to rental to security to IT to networking to other IT cost.

One can’t view just the “negative results” in isolation.

Strategy is clear

A) Increase branch , give aggressive interest , increase CASA, reduce CDs

B) Decrease infra/wholesale book , increase retail book

On everyone of their target set during merger, they are ahead of curve . Yes core business isn’t making profit. But every quarter every year the branch matures , more the increase in revenue per employee will be.

If I am not wrong, There is also IDFC stake sale by October on cards. Stock will have ups & downs. I am sipping this for now. My horizon is 3-5 years.

Let’s see the impact of Covid & see the resilience of business. But also let’s look at the big picture as well

9 Likes

Negative results are not because of Capex. It is because of provision they had to make for the wholesale book they inherited from IDFC.But considering bank is moving in the direction what they have planned it is a good sign. It is a risky best but worth the risk

1 Like

Agreed…Provisions are the most obvious parameter looked at , so didnt mention it. My larger point is the loss is bound to happen given the aggressive path taken. I hope bank slows down in this crisis & protect itself and consolidate.

Bank is certainly moving in right decision : Its almost like a consumer lending business arm of Capital First is now being backed by low cost of Bank CASA. If properly scaled up with proper risk management, potentially a very profitable bank is very much on cards. But patience required as a investor - this cant happen in a day given the legacy wholesale book & now Covid crisis.

Disc : Invested in small quantity

Here is a news from March 25 where Morgan stanley had cut the price target to 15 rupees in March 2020:

If they are cutting price target to 13 rupees now, I’m unsure how much anyone can trust their ‘targets’. Btw the report you sight is from before 26-5-2020 (Tuesday'S Top Brokerage Calls: Hdfc, Jsw Steel And More) and hence it is probably already being ignored by the stock market.

Vodafone Idea’s MCap is now 25,000cr, doesn’t seem like the market believes it is going to shut down anymore, far from it. Expecting a reversal of the provision within the next two quarters now. Book Value should go up close to 17,500cr or Rs 33. Bank trading at 0.75x BV even after the recent rally.

1 Like

Its a regular account for them therei is no default. Mr. Kumar Managalam Birla have to announce once again on stage or some forum or a letter, saying that they are doing fine to enable Mr. VV to take it as normal account. On a llighter note… ![]()

![]()

Thanks Puch, just wanted to understand how it works. At CMP (24.25), it is trading at 0.76 x BV, without taking into account the expected write back. Per your comment, if the amount does get written back, BV goes up to 33, and so the P x BV becomes 0.75?

I don’t understand how BV is calculated, but just wondering how such a large amount can make a difference from 0.76 to 0.75?

After the recent capital raise the BV is now around 30.5, so current P/BV is around 0.80x. With a 1600cr write back BV should increase around 10% so should go up to say around 33 and the P/BV multiple will then be around 0.74x.

1 Like

I think you are using the book value figure before the fund raise, after the fund raise BV has come down from 31.8 to 30.4 as new shares were issued at Rs 23.

Ah, I see. I’m using the money control numbers, but since the fund raise hasn’t formally gone through yet, I suspect you may be right.

Essentially as I understand it, the write back and the fund raise are going to cancel each other out in terms of BV, broadly speaking.

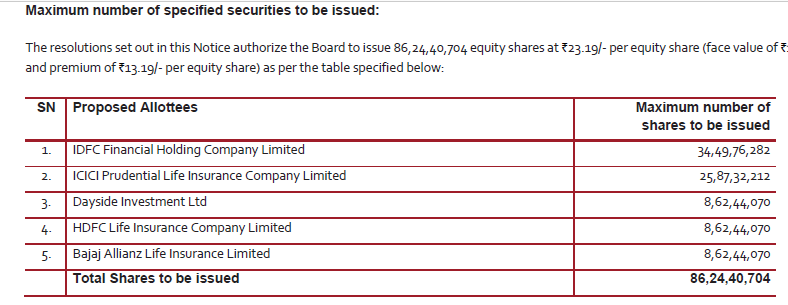

Actually it will be higher as dilution is not significant due to the capital raise. All numbers below from Company filings (sources below)-

31st March Shares Outstanding- 481cr

2000cr Capital Raise- Issue of New Shares- 86cr

Total Shares- 567cr

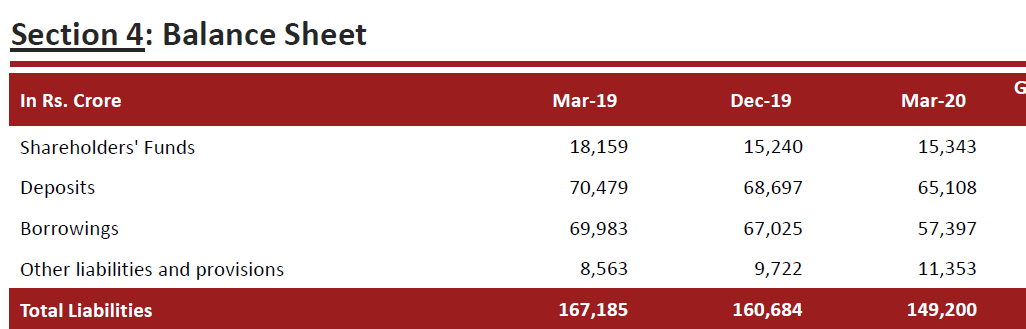

Book Value as on 31st March- 15,343

New Capital- 2000cr

Vodafone Write Back- 1600cr

Total Book Value- 18,943cr

Book Value Per Share- 18,943/567 = Rs 33.41

2 Likes