IDFC Bank’s Rajiv Lall & Capital First’s V Vaidyanathan.

4 Likes

Just come across a new concept of micro ATM at Batala near Rly Station which can give an edge to bank for disproportionate growth

Old Coverage by edelweiss

Dear Valuepickrs what is your analysis of fy18 results?

Considering they want to de-grow their legacy infra book which was half of total book, having flat NIIs is not bad. Corporate book grew 35% while retail rose 2x. Stock is languishing near book value. NPA numbers are significantly better than Axis/ICICI which still trade at 2x book. Unlike them no controversial things regarding management. Has a securities and investment banking business i.e a full-fledged financial firm unlike Bandhan/RBL. What could be the overhangs with IDFC Bank?

Disc. Holding CapF

2 Likes

NPA numbers are significantly better than Axis/ICICI which still trade at 2x book

IDFC Bank’s NPA numbers are getting worser and income growth is flat. Axis and ICICI are in the category of big boys, and are too big to fail. The same cannot be said for IDFC bank, which requires higher growth and operational efficiency in the upcoming years.

I feel CASA ratio improvement is a big plus. Retail growth is encouraging. But retail play for the bank will be tougher going forward, since competition is very high, when you have NBFCs, SFBs, Non-institutional lenders

competing for the same pie.

Rise in NPAs, fall in NIMs, low ROEs - the story continues YoY! we will have to see if CapitalFirst merger can bring something to the table

5 Likes

What might the reasons for the steep fall in the stock price

Some observations regarding change in shareholding pattern of IDFCBank as of June 2018. (1) First let the obvious be out of the way. Promoter holding increased from 52.8 to 54.3% and public shareholding decreased from 47.2 to 45.7% (2) Among instt players FPI and mutual funds sold 14.5Cr and 3.02 Cr shares respectively where as corporate and financial instt and banks picked up 3.5Cr shares taking the net instt shareholding down by 13.9Cr shares. These were picked up by promoters (5.10 Cr shares), retail investors (4.79 Cr shares), and clearing member (4 Cr shares). Conclusion: So, as can been seen the major part of the selling was by FPIs. This has nothing to do with promoters playing with the stock. FPI have their own dynamics that has nothing to do with the company. I do not see any issues with the company fundamentals or the management. The FPIs sold close to 8.66% of public shareholding during Q1. regards,

1 Like

Stumbled upon this thread purely by chance. Having read the previous posts, I do not agree with this statement. There are a couple of posts which cast doubt, rightly IMHO, upon the credentials of the management. The management seems to have been riding the “hope” wave and have not delivered on their promises. Having said that, it may be that this company may yet turn out to be a multibagger, but the question evidently arises…when? I think, not in the next 3-4 years, based upon their performance.

Please feel free to correct me.

Regards

1 Like

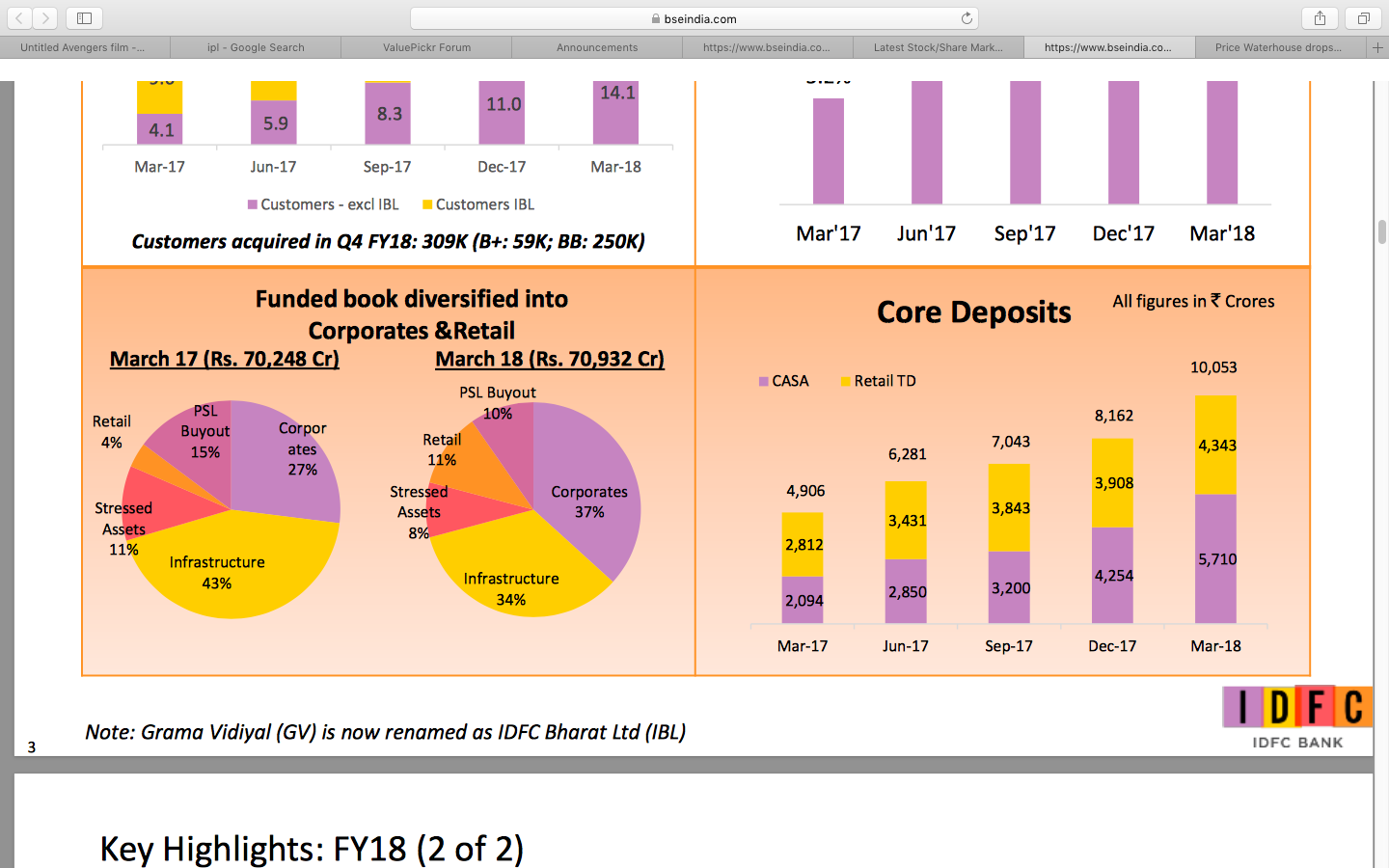

The bet is basically on new ceo mr vaidyanathan, who turned around capital first and on mr. avtar monga, coo and retail head. CASA for example has been showing good growth. 5700cr in fy18 n expected to cross 10,000 cr in fy19 as per management commentary. Retail assets are also growing fast. The merged entity with capital first would have 40-45% retail component out of the total loanbook on day 1.

Disclosure : invested from higher levels

2 Likes

This is not to correct you in anyway  Just some clarification (1) By company fundamentals I am saying the direction in which things are moving. I agree they have not been as successful as others but the retail book is growing and quite fast. The environment they started in has been challenging too. Others who had gathered the critical mass could deal with it better. But then this is a private sector bank that is available at public sector valuation. I believe the problems are priced in. (2) About management, I am talking relative to PCJ, Satyam or even Chanda Kochhar kind of management. (3) Lastly, like most others I invested not looking at the glorious(??) past but for the post merger entity. Perhaps it was better to invest in CAPF to enter the same entity but if I mistake not IDFCBank has more FnO volumes, higher IV and hence opportunities to hedge / earn some money. Advantage of CAPF is that given the merger ratio (13.9), CAPF is available at a discount - most of the times. regards,

Just some clarification (1) By company fundamentals I am saying the direction in which things are moving. I agree they have not been as successful as others but the retail book is growing and quite fast. The environment they started in has been challenging too. Others who had gathered the critical mass could deal with it better. But then this is a private sector bank that is available at public sector valuation. I believe the problems are priced in. (2) About management, I am talking relative to PCJ, Satyam or even Chanda Kochhar kind of management. (3) Lastly, like most others I invested not looking at the glorious(??) past but for the post merger entity. Perhaps it was better to invest in CAPF to enter the same entity but if I mistake not IDFCBank has more FnO volumes, higher IV and hence opportunities to hedge / earn some money. Advantage of CAPF is that given the merger ratio (13.9), CAPF is available at a discount - most of the times. regards,

Yes, I would agree. But being inherently cautious, I would prefer to watch at least the results of the next quarter, and look for positive and supporting signs in the BS. And it would be equally true to say that each person has his own strategy, but participating in discussions on VP has shown me a different perspective which has positively contributed to my learning process.

Thanks and regards

That is very true. Discussions here are much more informative. I agree, IDFCBank is more of a leap of faith for me but then the arguments put forward - retail sector growth, focus on technology, hub and spoke model instead of costly branch network will keep the costs low. The way I see it most of the staff in other banks does things that can be done by machines on a 24x7 basis - like accepting cash, cheques, and service requests, giving cash and printing passbooks. The banks will go down due to the cost of maintaining branches, creating forms/stationary, and not to mention over pampered staff thanks to unions. Since it is not easy to fire employees in India, I would bet on a bank that would keep these costs under wraps from the very start. That along with valuations and post merger promise sums up my investment rational. BTW, Vaidya had said bank will take 2-3 years for significant gains to shareholders so your estimate of 3-4 years is perfect. I am ready to wait for that long, so it works for me perfectly. regards,

5 Likes

About the management quality - when Mr. V Vaidyanathan was asked to grow the retail business at ICICI Bank, he had all of 50 employees in his division. By the time he left it after nine years, it had more than 26,000 employees at 1,500 branches in India. With his own stake in IDFCB, and age on his side, I do not doubt his leadership.

6 Likes

I admire Vaidyanathan a lot and thats the sole reason for me buying IDFC bank (small holding at moment). Has he started operations already or post merger he will operate as CEO of IDFC bank? Is he calling the shots already?

Also, with Capital first, the loan book will have retail component but how will they increase CASA needs to be seen…Capital first will not help them get deposits…or will it?