If we(shareholders) want to know about NPA percentage of a particular partnership (Flipkart Pay Later for example), will the bank tell us that data?

If yes, how to ask and what all to mention in the email

If we(shareholders) want to know about NPA percentage of a particular partnership (Flipkart Pay Later for example), will the bank tell us that data?

If yes, how to ask and what all to mention in the email

Stock started moving up only after sahil exited it. I don’t know why you exited the stock sahil. Can you give your thesis and what’s the course correction you want to do after this ,?

He probably has a better opportunity, and a compelling one. Otherwise, going by VV’s guidance, Opex will unleash around 2025.

Pl explain what u mean by “opex will unleash by 2025”?

It has been almost 3 months since an independent valuer for giving a fairness opinion on the swap ratio was appointed. Generally, it does not take this long to arrive at the swap ratio. To me it indicates that the 2 entities involved here are really negotiating hard for their respective shareholders.

Going by the recent trends in reverse mergers, a 14-15%(swap ratio of 140-142 for 100 shares of IdFC ltd) discount is a given in my view. IDFC First Bank could be asking for a higher discount of 17-18%((swap ratio of 135-136 for 100 shares of IdFC ltd).

Given RBI regulations, IDFC First bank has an upper hand in the negotiations in my view.

In my view, the ratio should be announced before the Q1 results.

@ishanagarwal89 14-15% discount of what? share price- share price, book value-book value, fair value - fairvalue

So as of now, each shareholder of IDFC Ltd indirectly holds 1.658 shares of the bank for every one share of the holding company. 15% discount means that every shareholder of IDFC Ltd will be issued (1.658*(1-15%) which is 1.409 shares of IDFC First Bank. If the discount is higher, IDFC Ltd shareholders will be issued lower number of shares. Hope it clears your doubt.

Everyone is talking about discount. I’m unable to understand this. Why do you want to have swap ratio? . Idfc is not having anything other than idfc first shares. They will just give of the share that they hold.

If they decide discount, after distribution shares. will idfc first will extinguish the extra shares ? . Is that allowed ?

I had invested in Capital First. It is now turning out to be an acceptable decision, however I felt that CF shareholders were let down when a string of large NPAs suddenly cropped up subsequently. These have been explained away as legacy issues. Since the combined entity is being claimed as an ethical unit, I feel the merger provides an opportunity to IDFC Ltd to set things right.

The merger ratio can make an attempt to compensate the CF shareholders for the capital loss they have suffered during the last four years by providing a reasonable discount.

Swap ratio can not be decided on the basis of ethics or emotions…

Also we don’t know how many shareholders jumped from IDFC First to IDFC Limited and vice-versa during all these years in hope of a better deal or safer investment…

.

The fact is IDFC has a certain number of shares of the bank as promoter and there should be some logical rational explaination for the number of shares both entities agree to extinguish out of those during the process of merger…

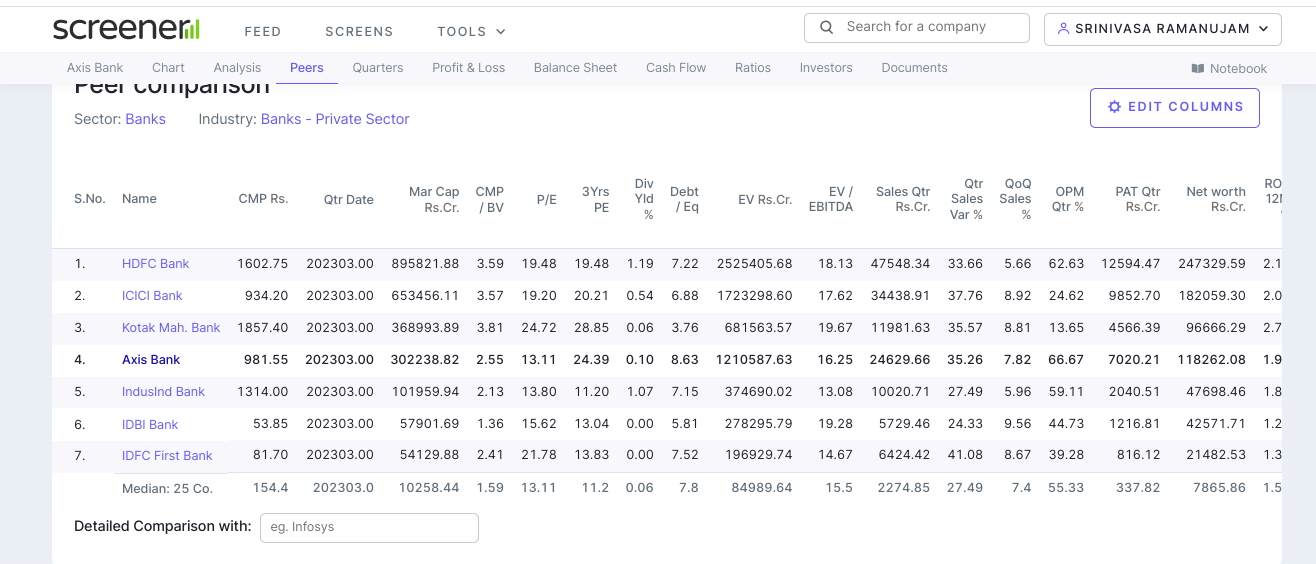

IDFC First Bank’s PB is inching closer to Axis Bank which I think is not sustainable.

I hold both IDFC and the Bank and been shifting some quanties in favour of Axis Bank which I think, will outperform compared to either IDFC or the Bank.

Disc: IDFC/IDFC First Bank is my second largest holding and I also hold Axis Bank

I think the book value per share for both the banks is not updated on screener. This is as per FY22 book value. Book value per share for IDFC First at the end of FY23 is 39. Hence trailing price to book value is just over 2. I agree though that the valuation is based on the assumption of further improvement in ROA and ROE in FY24.

@Vivek_Shetty

Thanks. I stand corrected. IDFC bank’s PB is 2 Vs 2.4 of Axis Bank. Still I think, Axis Bank is relatively undervalued compared to IDFC bank. So, I will keep switching in favour of Axis Bank. This way, I will keep reducing my allocation to IDFC bank and increase it in Axis Bank, assuming that the gap remains about 0.5 times the PB. It is my belief that Axis bank will quickly catch up with the likes of HDFC/ICCI bank.

Why is it not sustainable…??

.

There is high probability that IDFC First Bank’s book value will rise at faster rate than Axis Bank for next 2-3 years as Axis’s profits are normal for its size but IDFC First is a turnaround story and has a low base to grow from…also if AU small finance and Bajaj Finance can trade at a higher book value than large private banks then IDFC First can also sustain at P/B of 3 or even more going forward…

In my view, Idfcfb should be rather compared with AUSmall finance bank than Axis bank in terms of P/B ratio.

Ausfb is commanding a P/B of over 6 and Idfcfb is at now at 2. Moreover, the market perhaps knows the books and future profitability looks way more better for idfcfb, and that is how they decide the price.

Good time for the investors to just wait, appreciate the conviction they had shown in past and witness it paying off slowly but steadily.

eventhough more interested in fundamentals technicals of idfc first bank also looks interesting. Interest rate looks peaking out should help idfc first bank a bit for cost of funds and also due to scaling up of books operational leverage due to reduced cost should also benefit idfc first bank

"Shares of the bank have gained momentum since the past one month as reports state that the bank could be included in the MSCI Standard Index.

Industry experts believe that in the next MSCI review set in August 2023, IDFC First Bank may as well enter the index after the stellar performance."

CLSA downgraded the bank’s rating to “underperform” due to concerns over its valuations, despite it being the best performer on the Nifty Bank index in 2023. The downgrade suggests that CLSA expects the bank’s financial performance to deteriorate or underperform compared to its peers.

For IDFC FB book value (per share) to grow faster than Axis, you need one of 2 things:

Sharing my personal experience…

I wanted to withdraw 1lakh Rupees cash in ahmedabad, I had icici bank cheque book. However, icici bank told me that non home branch withdrawal of 1 lakh ( as my home branch is in other district ) will have 500+ gst extra charges…

There was idfc first bank besides icici branch. Went there. There is no home branch concept in idfc bank. So, One lakh Cash withdrawl charges are zero. ( till 4 withdrawals, no limit )

Saved 500+ tax rupees, clean and easy…

They also dont have cash deposit charges to any of the branch…

No wonder idfc first CASA is moving higher. When there are no hidden charges, customer put their money to save those hidden charges. - one of the reason…

Disc: Holding