As per Management guidance, Advances are expected to grow at 20-25% in the foreseeable future and it will be fueled by growth in CASA and not by further equity infusion.

With a few basic assumptions:

Net Interest Margin (NIM) will stay in the range of 5.5% to 6% in the near term

Cost to income will eventually reduce (management guiding at 55% for FY25, in bear case let’s assume it reached 65% by FY25)

GNPA and NPA levels to remain around 2% and 1% respectively. (as per mgmt guidance and their long-term track record at Capital First.)

Positive support to NPA levels in the coming years as the Infra book is being closed rapidly

Positive support to NIMs as legacy high-cost borrowings are being replaced with new low-cost funds. (Legacy borrowings are with different maturity dates, most of it is maturing by FY26.)

Qualitatively,

IDFC First Bank is building itself as a strong retail franchise with a customer-first approach and superior marketing and branding. According to my own experience and some scuttlebutt, IDFC First Bank has got one of the best tech capabilities (Net Banking, Fastag, Payments, and other ancillary services.) , also it has strong goodwill among its customers, employees, and the public in general.

With these facts and assumptions in mind, I feel confident that the Bank will:

Be able to generate enough CASA Deposits to fuel its growth

Meet the guidance of growth in Advances at 20-25%

Key Risks here can be:

Cost to Income stays very elevated, thus decreasing the ROE.

Provisions increasing from current levels either due to weak underwriting or economic cyclicality

Key man risk: V Vaidyanathan, CEO of IDFC First Bank has been the showrunner and thus the stakes on him are high.

To conclude, if the risks are kept well in control, IDFC First Bank has the potential to be a multi-bagger 2-3x in the next 5 years with even brighter future prospects.

Do let me know what you guys think or If I am missing something here?

Key man Risk:

In my view it is irrelevant at least for this bank. Already they have impressive leaders in key positions, who are equally capable.

These days I see more of Madhivanan Balakrishnan than V Vaidyanathan in most events.

Not missing anything but your return expectations are low…which is a good thing probably…

With newer segments like credit cards becoming profitable and legacy borrowing getting replaced with low cost funds, I am expecting the bank to make profits of roughly 3000,4000 and 5000 crores in F.Y. 24, F.Y 25 and F.Y. 26 respectively…and stock price to be 4X in 3 years, specially considering it has done nothing in last almost 5 years…

Hi Sir,

I think we need to see at what rate can they grow their Book value instead of PAT.

If we see right now in terms of PE they look to be undervalued but in terms of PB they look to be fairly valued.

If their cost to income ratio is high then the incremental money which they make for every rupee they deploy is going to be low. Eg if CI is 70% you need to spend 70 to earn 100 and if CI is 50 you need to spend 50 to earn 100.

Their PAT can grow at much faster rates but their Book value would not grow at that rate hence we should project their FY24 or FY25 Book value and then give them a multiple to see the possible price appreciation instead of PE.

Even in PB market only gives you a 3times or a 4times PB only if they see you can have a sustained earnings and growth over a long period and the requirement to dilute your shares is low and generally for small SCB this not the case hence 2times to 2.5times is the upper limit for IDFC as of today.

Considering all of the share price growth of 3x or 4x in next 3yrs is low as earnings can grow fast but book value will not.

In short instead of PAT growth we should see EPS growth or book value growth.

ROUGH calculation

- If they are trading at 2.5x PB and price is 200 that means book value of 80.

- For a book value of 80 they need to add 25000cr to 30000 to their share capital without diluting shares.

- There are two way to get this money 1. PAT and 2. Raising money above book value( this process delays the increase because incrementally after dilution you add very less money)

- So now we can calculate how much time will they take to get that money and see when can we expect 200rs share price.

Please let me know if I am missing anything

I am still learning and might be wrong

thankyou

Hi Manhar,

Your Point of view is correct, but I would like to know your inputs on:

- How much can bank grow (Advances, CASA, Fee income, etc.)

- NIMs going forward

- NPAs going forward

- Equity dilution going forward

Because these are the drivers of Book value as well as PAT.

If our conviction with these key drivers is high, then we might not need to cut corners in forecasting each financial metric in detail.

Tough to predict exact numbers in future…

But if we try to imagine situation after 3 years, if market conditions are stable and nothing happens to disrupt current business model of banks, IDFC First can have significantly larger and granular loan book with healthy profits…it will be one of the 5-6 large banks in private sector, so a valuation of P/B of more than 3 is not unimaginable…

Also book value per share will increase with some shares getting extinguished at the time of reverse merger, equity raise at better valuations hopefully and ofcourse 3 years of profits adding to it…

Best estimate scenario after 5 years:

- Loan book is increasing at 25% per year. So loan book will be=(1+0.25)^5= 3 times the current book after 5 years. So as to maintain the statutory capital adequacy ratio, book value will be also 3 times (On the un-diluted basis).

- In the near future earnings will increase faster than loan book because of operating leverage and other mentioned factors in the forum. My estimate for the earnings growth is 40%, 35%, 30%, 25%, 25%. So profit will be approximately 4 times the current profit.

- Currently ROE is ~ 12%. Trajectory for ROE by accounting above figures: 12%, 13.44%,14.52%, 15.1%, 15.1%

- Subsequent dilution will be at price of N times the book value. N for subsequent years will (assumed) be 2, 2.25, 2.5, 2.75 and 3.

- Dilution required per year to maintain the statutory requirement of capital ratio is: 7.5%, 5.13%, 4.19%, 3.6%, 3.3%. So total dilution in next 5 years will be 21.62 %.

- In conclusion, at the end of next 5 years, book value be 3 times the current book value. Dilution will be 21.62%. Valuation will be 3 times book value. So price appreciation expected is =3/1.7 * 3 * (1-0.2162)= 4.1X . (Note that current price to book is 1.7)

Note: Invested and Biased

I am just starting out on analyzing banking stocks. Couple of queries:

- Skin in the game: Understand that VV holds less stake directly (0.4%). Does he hold stake indirectly in the firm?

- NIM: NIM is 6%+, which appears more in the range of a small finance bank (vs. 4% levels seen in normal good banks). Is this because of the advances yield given at historical high levels when it was a NBFC? If so, then there could be a reversion to mean of NIM as these loans mature and new loans are obtained at bank lending rates. Is this understanding correct?

My thoughts…

VV held more earlier that was financed by debt. This stock got sold at lows due to margin calls. I dont think he has any indirect holding

NIM is higher due to the nature of this bank’s business. It has nothing to do with any historical high level lending. Its essentially an NBFC in a bank’s clothing, so it generally lends at the higher rates

Its indeed an aggressive projection, best case scenario, when you give it 3X book. I dont think it will happen. Between 2 and 2.5X is the maximum it can get, in my opinion, rather the book value multiple may stagnate with the improvement in earnings. In a space of 5 years, it will also face one pain cycle when its aggressive lending starts to create issues.

- How much can bank grow (Advances, CASA, Fee income, etc.) - 20% CAGR

- NIMs going forward - Between 5 - 6%

- NPAs going forward - May have 1 cycle of pain after 2 years

- Equity dilution going forward - consistent dilutions will be required.

Many factors come into play when deciding whether PB would be 2.5x or 3x. One of the most important factors is the projected growth rate at that point in time. If the NIMs are high with low NPAs, accompanied by strong loan growth and low cost of funding, then the valuations are likely to be high and vice versa. Market always pays for delta in future earnings and the sustainability of such earnings.

Just a naive question…

Why AU Small Finance Bank and Bajaj Finance trade at P/B of 5.5 and 7.5 respectively…

And why IDFC First can’t trade at P/B of 3 or 4 if it keeps improving it’s business for 3 more years after doing that for almost 5 years already… ??

They’ve found a core strategy, gone all in, and won big.

And they’ve had stable management and consistency. The story is clearer, they aren’t turnaround plays.

My understanding is that the valuation of a bank depends on its ROE. If IDFC First is able to improve ROE and maintain asset quality, it is likely to get rerated. The quantum of rerating depends on the extent of improvement in ROE. For a long term price to book over 3, it has to consistently maintain its ROE over 18%. Whether or not it able to do that, only time will tell. Currently, with ROE at around 10%, it is probably trading at fair value.

Disclosure- Invested.

The latest figure declared on 21 Apr by RBI on banking deposits and loans, showed an increase of 0.6% and 0.7% respectively compared to previous month figures. This is encouraging.

The Indian economy and bank balance sheets have never been better than present moment and by all indications economy is going to do very well in fy 23-24. Consequently banks will also do well especially some of the private banks like HDFC, ICICI, Axis and IDFC first. Due to its small size IDFC should be able to grow its assets comparatively faster for next few years.

Of course we have to keep our fingers crossed against the possibility of unexpected provisions and adverse events like covid.

The turnaround has got delayed by about 2 years due to unexpected loan defaults and covid. Let us hope that future is less eventful.

My understanding is that bank valuations are mostly dependent on ROA and ROE.

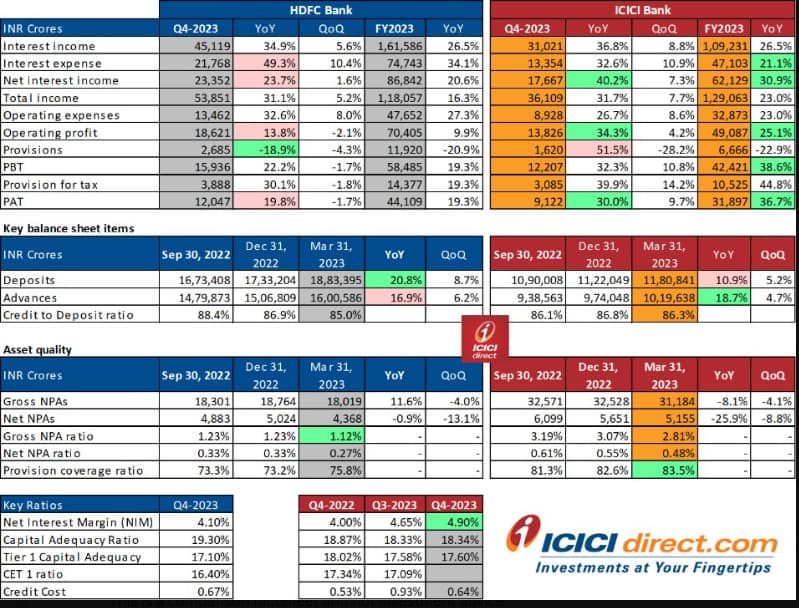

In the last 3 to 4months I have realized how important Cost to income is so let me just share you what I have noticed. Please Ignore if you already know

This is the result of HDFC and ICICI if you notice HDFC NII is 86000cr ( up 20% YoY) and operating expense is 47000cr ( up 27% YoY) despite this in absolute terms they have added incremental revenue when I just compare NII and operating expense. Same can be seen in ICICI case.

In IDFC case NII is 9000cr (up 28% YoY) and operating expense is 8700cr (up 25% YoY) now the incremental revenue IDFC has added is absolutely low.

In simple terms if NII is 100 and operating cost is 50 and both increase by 30% my revenue grows by 15%

But if NII is 100 and operating cost is 90 and both grow by 30% I grow by 3%. Now I cannot increase the gap between my NII and operating cost in 1year it will take 2 to 3yrs atlest.

IDFC NII is 100 and operating cost is 96 so now we can do X growing at 20% Y growing at 15% or whatever and see when can it come to NII 100 and operating cost at 60 for operating leverage for comparison HDFC operating cost is 55 and ICICI 53.

But despite this problem the only way to still grow is other income which can be game changer so in IDFC case we have to analyze 1. What are the operating cost, How much is business volume related, When will leverage kick in. 2. How much can other income grow.

Another important point is we have to see this year how much of my profit came from lower provisioning and how much came from higher operating profit or PPOP and next year will I be able to get more profit from lower provisioning or not.

As rightly said by Nirvana Laha Sir that we have to focus on the % of promoter NET WORTH in a company. So if this 0.4% is lets say 90% of his NET WORTH then there is enough skin in the game

I think these are their sustainable NIM but in the very long term as you get bigger they to to come in line with larger banks. EXAMPLE - Bandhan bank had a NIM of 8% but then they had asset quality issue and now they are moving to corporate lona from EEB loan ( Emerging Entrepreneurs Business) so they are saying that going forward their NIM will fall.

Now it is not going to fall by 100bps in 1 year it is going to be very slow because as a bank becomes bigger they want to give loan to the creamy layer which as on date is captured by HDFC,ICICI,KOTAK that is why they have the best asset quality and you can give loan to this creamy layer only when you have the ability to take CASA and 3.5% or 4%

A good way to see PB said one by Ayush Mittal sir was divide the ROE of a company by the 10yrs bond yield. So if ROE is 30% and bond yeild is 6% PB can be 5times. Now there are many more adjustment to be done and this not a hard and fast rule. A SCB bank can never generate 35% ROE what an NBFC can hence high PB.

SUMMARY.

1. We have to focus on ROE as it captures dilution but PAT does not so instead of PAT growth we should see ROE and EPS

2. We need to see other income and how long can it grow at current rate because for IDFC that is critical as for 2 to 3yrs operating leverage wont be significant.

3 We have to analyze operating expanse and see how much is volume related and try to roughly estimate when will leverage kick in

4. How much profit this year was form lower provisioning and next year what will be the drivers

5. At what rate can book value grow @Pradeep_Jadhav Sir most of your estimates are too high especially dilution at various PB and i think some where we have to consider cyclicality factor I feel especially small SCB cannot have linear growth. So that factor has to be considered

Thanks for this well written and elaborated reply…

expanding on my naive question, dividing ROE by Gsec yield to arrive at P/B does not seem to be working in case of financial sector entities atleast… in case of AU small Bank and Bajaj Finance according to their current P/B which is much below highest and unrealistic levels which they attained once, even at these levels formula which is working for them seems to be more like 2*ROE/Gsec…if we want to apply that…xD

.

also on point raised that they have an established strategy and business model etc.

IDFC First Bank will also have backing of that narrative and will come out of cocoon labeled as ‘turn around story’ once it starts showing consistent profits it seems…business is consistently improving since merger despite unexpected roadblocks like covid but looks like market will recognise it only once profits normalise, F.Y 2022-23 is first year where profits are somewhat normal for a business of this size, 1 or 2 more years of that and it will be re-rated I think…

11 years in operation for IDFC bank, what it has become a bloated equity mamooth, not even at IPO orice.