What is the need to raise furthur capital, once the bank is comfortably into high profitability?

That is the most important question to ask. Situation with idfc is there are many good things happening at balance sheet level but nothing good is happening at per share level. It is the basic thing but very hard to implement practically because somehow we have developed the habit of looking at net profit not eps.

1 Like

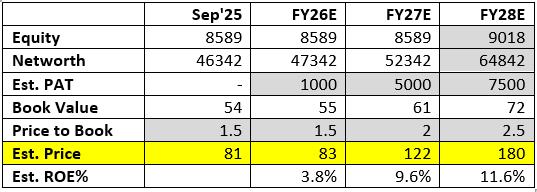

With the expected 20-25% growth in advances and the profits projected, the capital adequacy ratio may fall below the desired levels (above 13%) by Mar’27. The bank will not be able to maintain 20% growth levels without raising the capital for the next few years, until it achieves a stable and healthy ROE of 15% or higher.

updated with ROE projections:

5 Likes

This is a good projection Vijayanji.. and you also put some things into a clear perspective with the column. VV has said that he will come to the market again after 2.5 years to raise capital. His Loan book growth was going forward 20% mostly from now on. Considering that you have increased the equity in FY28 is a good projection. Considering the share price will be a good 5-10x for covid investors by FY30, i think it will be a good run by FY30.

1 Like

If IDFC First Bank is able to achieve a 15% ROE by FY30 by continuing on this same projection, then after FY30 equity dilution will also not be required very frequently.

Till how long can we expect VV to continue? He’s 58 right now

Soon he will move to an advisory role and step away from CEO role

This is an interesting proposition.

I dont understand one thing however.

You say ROE prediction at 9.6% at FY27 and 11% at FY28.

Assuming that happens, will the bank not have to raise capital in the period since it is still below 15% ROE? So if that happens again equity will get diluted and then the Est Share price will not be anywhere near the 122 and 180.

Am I missing something?

Please correct me if I am wrong or missing something.

Market price is related to book value which will go up due to the price at which fresh equity is raised.

1 Like

Couple of things to note for all the boarders

If you are projecting for over 6000cr of profitability, which is atleast 3x from current profitability… It cannot come without major growth in loan book, along with couple of assumptions of interest reduction on savings, and no major npa, and cost to income stabilizing at 65%…

Even if they achieve 6-7000 of PAT, the ROE will be less than 15% , and in process of reaching 6-7k PAT, their tier 1 capital will get depleted due to aggresive loan growth…so they will have to raise funds within next 6 quarters…

Also, even if they achieve by god’s grace 6-7k PAT in 2 years with all the above things - The RoE below 15% will not let the P/B reach 2x…it might top out at 1.6x BV…

But market nature is such, that it swings in extremes…personally for me, if I am an IDFC shareholder, 2x BV will be A sweet exit point for me.

1 Like

Bro the bank itself is running on VV.. how can you expect him to exit and place somebody else? he will remain the CEO for the forseable future unless the banks performance is getting really pathetic.

Yes Vineetji.. i really agree with your last line. For few people including me, this was a safe stock and one that gave hopes. And it remained a hopeful stock that’s all. Hope everything changes soon in the next few quarters we get a good exit

The bank recently raised funds of 7500crs, with the next fundraise expected around FY28. Projections (including share price estimates) already factor this in. assume your query is not about capital needs beyond FY28.

Okay thanks for clarification.

The bank reported profits of 2500crs (FY23) and 2900crs (FY24). FY25 and FY26 profits took a major hit due to Micro Finance issues. With the MF portfolio stress now normalizing (with book size < 3%) and overall business continue to grow at 20%, even if they repeat FY23/FY24 performance levels, profits should increase by 50% in FY27 - in proportion to the expanded book size (2lakh crs in FY24 to est. 3lakh crs by FY26).

Other positives:

- COFs to reduce with the reduction in interest rates on SA deposits

- Unit economics of the bank to improve going forward – as branches age, new products reach break-even (for ex, credit cards), etc.

- Reducing high-cost borrowings (legacy bonds, etc) and replacing with low-cost deposits

The critical assumption (or variable) in the projections is profitability. The projections hold good ONLY IF there is non-linear profit growth in the next few quarters. key metrics to watch closely:

- sustaining 20% growth and ~6% NIMs

- stable asset quality and credit cost < 2% (credit cost for FY25 was 2.5%; a 0.5 % point reduction in credit cost will increase PAT by ~1500crs and improve ROE by ~3 % points)

- ~5% equity dilution expected by early FY28

- progressive y-o-y improvement in the C:I ratio (a 5 % pts improvement in C:I ratio will increase PAT by ~1500crs)

(Note: FY25/26 PPoP impacted by MF loan book reduction – high-yield portfolio downsizing - resulting in higher C:I ratio despite lower opex/book growth)

wanted to reiterate that the large equity base is a structural issue and the bank to continue raising capital until it achieves a stable, healthy ROE of 15% or higher. Higher ROE drives faster BV growth and higher valuations (P/B multiples).

Finally, it might not turn out to be an asymmetric bet, but it fits the – “Heads I win, tails I don’t lose much” scenario.

Disc: Invested, biased, not a buy sell reco.

2 Likes

it’s not fair to see Net income, PPOP, Interest Income etc for this bank. for obvious reasons

A 20% growth stock must have atleast 35 PE.

Now, here comes a leap of faith, to estimate EPS from loan book size.

for Kotak bank it is

"net profit to loan book ratio of approximately 0.7% for the quarter (annualized, it is roughly 2.8%). "

Idfcfirst banks loan book size ₹2,66,579 crore

at 2.8%, gives net profit of 7464 crores, divided by outstanding shares 731 crores gives EPS of close to 10.2

At 35 PE, share price should be 350. Market is cautious. It gives it only 85. But, not for long.

5 Likes

It’s to be noted that there’s meaningful change in Interest rates. This can be seen a ms one of the step towards reducing liability cost and should contribute a few bps to ROA.

Need to see how they’ll bring more changes in future.

This is the playbook for Kotak while ut was building it’s liability franchise

2 Likes

If you plant a banana tree, it will yield fruit in 6 months. A papaya tree will yield fruit in 2 years. A coconut tree in 4 years. A mango tree in 5 years. And if you plant an apple tree, it will yield fruit in 7 years.

Bananas sell at rs 50/kg, papayas at 70/kg, coconuts at 90/kg, mangoes at 120/kg and apples at 250/kg. Some farmers plant banana trees because they need quick profits, even though the profits will be small. Some farmers plant papaya trees because they are willing to wait slightly longer to get slightly bigger profits. Some plant mango trees, because they are willing to wait even longer, to get even bigger profits. While some plant apple trees, because they are willing to wait very long for very fat profits.

Vaidyanathan is like the farmer who plants apple trees. He has played the long game, spending 7 years investing in building multiple businesses, and a strong liability and asset base. He could have taken the approach of a papaya tree farmer - invested much lesser, and aimed for quick small profits. But he ain’t no papaya farmer. He is an apple tree farmer. Period.

Now, I read posts above, of folks planning to exit IDFC bank when it reaches 2x book value. How unwise would that be? Because it will be like planting apple trees, waiting 7 years for the trees to bear fruit, and then selling your apples at the price of papayas, thanks to 7 years of frustrating wait!!!

What has Vaidya built in 6-7 years? Its a long list - fastest growing bank, fastest growing deposit franchise, fastest growing loan book, fastest growing CASA, huge reduction in cost of funds, most granular deposit franchise (80% retail deposits), most granular asset book (80% retail loans), fastest growing credit card business, class leading customer experience, class leading digital stack, etc etc. It has lagged on two parameters alone - Asset quality and Cost to income (Operating expenses).

Asset quality issues are more or less a thing of the past - the two problem areas have been resolved. Infra book is run down almost completely. Microfinance book is now only 2.5% of the loan book, and almost completely insured.

Operating expenses are being significantly addressed and operating leverage has started to play out. In the last few quarters, the business of the bank grew by 22%, while operating expenses grew by only 11% to 12%.

I expect IDFC bank to post around 1000 cr profits in Q4. If you annualize it, that would be around 4000 cr profits. That’s nearly 8.5% RoE, which is huge considering that IDFC Bank is generating such RoE while growing 22% in the midst of a war for deposits, with a cost to income ratio of 70%.

Now try to imagine the RoE that this APPLE TREE will generate when it’s cost to income ratio falls to 50%, when its cost of funds normalize to levels of other big established banks, when it starts charging fees for various service like other banks do, when it has established a strong Current Account franchise, when its credit card business becomes profitable, and when there is less intense war for deposits, etc etc. It can easily be upwards of 20% RoE.

So, my suggestion would be to not sell your Apples at the price of Papayas!

9 Likes

By this logic you will make Rs 250 in 7 years selling apples and Rs 700 in the same time by selling Bananas every 6 months - thus making close to 3 times more!

5 Likes

By this logic you will make Rs 250 in 7 years selling apples and Rs 700 in the same time by selling Bananas every 6 months - thus making close to 3 times more!

Exactly - so last 7 years, one would have made far more money being invested in other banana counters. But what happens the next 7 years - hold bananas or apples? ![]()

Hold banana tree when the apple tree is growing up. But once the apple tree starts bearing fruit, then sell off your banana tree (and not your apple tree).

3 Likes