One has to think how a start up bank translates into high operating expenses.

Are there any fixed costs associated with the bank that lead to high expense initially followed by lower expense? Is a bank branch associated with a high fixed cost upfront?

I believe most of the bank branches are in rental premises so it is a variable cost. Even furniture, hardware are capitalized expenses and not fixed expenses running through income statements. Bank employees per branch can be easily scaled as business has grown.

Most of the items listed in the expense account of the bank should be linked linearly with the scale and volume of the bank compared to what is being portrayed by management.

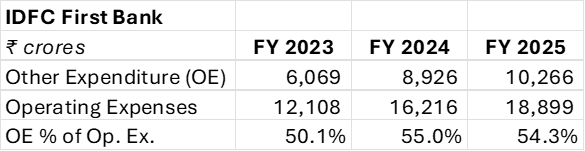

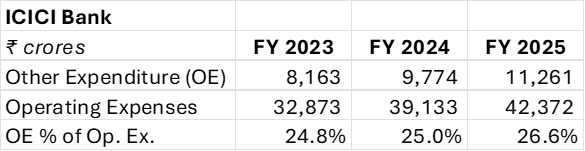

It bothers me that the bank puts out 100+ slide presentations every three months but has scant details about other expenditures compared to other banks such as Kotak Mahindra Bank or ICICI Bank in annual reports from 2021-2024.

Recently the bank has started including a few more details but these are insufficient especially since IDFC First investment thesis hinges on two pillars of bank maintaining NPA ratios and bringing expenses inline with other banks.

As it has been pointed out, operating expenses are increasing with the size of the bank and not coming down.

How much is branch banking relevant for IDFC First or any other bank? Bank MD has talked about technology stack and app built by the bank, how is that supposed to help the bank achieve higher ROA and ROE? Is that working out as expected? Very long presentations, frequent interviews, speeches and annual reports fail to shed light on these questions.

Does the bank need to enter all these new businesses on the deposit side and on the lending side to be in start up mode after merger in 2018? Did Capital one have all lending business that bank wants to be in? If those were existing lending businesses then they should not be in the start up stage. If those were not part of Capital First then why does the bank need to be in these business and why does it need to be those businesses now? Vaidya has highlighted India’s growth potential multiple times so does that need continually investing to expand product portfolio or does need scaling of existing lending products?

There are specialized gold loan companies, credit card companies, and wealth management companies. Does a bank need to compete with all these companies and in all possible product categories when it is a start up bank? It might be the wish of MD to build a universal bank ASAP but I disagree that the bank needs to launch all these products to be a successful bank.

Indian investor will be better off expanding investing pool to consider companies listed outside of India. There are lot of good established banks and other companies delivering great results in US, Canada, Europe and Japan.

Vaidya had also indicated that micro-finance issue would be resolved during H2 of 2026. I never understood why bank chose to dilute heavily around 1.1 P/B ratio. Bank had raised funds at much higher valuation. As per management predictions, fundamental outlook was going to be improving in few months so what was the need to dilute so heavily at such a low valuation.

Vaidya praising P/E investors as marquee and very grateful to have them invested seems like he doesn’t value existing shareholders who have invested in the bank with long term mindset and have been and willing to be shareholders for the long term.