A good product is not always a good investment. Their ROEs are in line of 10%, their loan book growth is 22% approximately so they keep diluting. Now their profits are have grown 18.4% last year and their EPS grew only 11%. The time they will start getting control on costs, it will be a good investment, till then enjoy the banking service.

7 Likes

A quick feedback on services for people who are using IDFC First Bank as their primary bank account.

I have been using IDFC First Bank as my primary bank acccount for over 4 years now (started around the time CoVid struck us as that’s when I first learnt about IDFC First Bank and its philosophy)

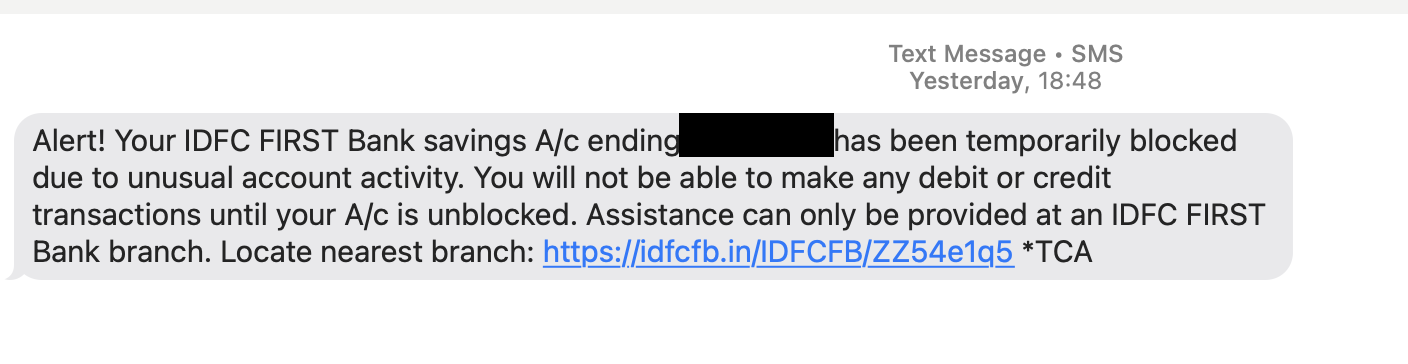

In Sep 2024, my father’s account was flagged “Debit Restricted” suddenly out of the blue in the evening hour, right at the time when he needed access to the account. When I called up customer service, they simply said they cannot help. Its automated, nothing in their hands. Please wait for 48-72 hours and it will be automatically sorted, meanwhile, since IDFC First Bank is the primary bank services provider for my family, the main source of funds stood restricted.

Being a shareholder, I sent out emails to MD’s desk, Investor relations, Customer Care head, Head retail banking and in about a couple of hours I got a call back that they are in the process of getting this fixed.

Next, I got a response from MD’s desk, saying that thank you for flagging gap in our resolution process, we will have this addressed.

Fast forward 4 months - Jan 2025

This happened again, this time with my bank account. I am sitting at a hospital, making IMPS transfers to my wife’s HDFC Account because hospital has HDFC account and they say they get instant payments if made through HDFC Net Banking, and bang out of no where, same “Debit Restricted” flag appears again.

Called up customer care > They said “Too many IMPS transfers” - I made 9 transfers perhaps as I was getting invoices from the billing department at the time of discharge.

Called up customer care - same response - no change. MD’s desk said they will address the issue, sadly they don’t seem to have yet.

Again emailed same set of people on the same email thread. Been about an hour, account still remains restricted and funds are still stuck.

Bank didn’t come to help, thankfully the hospital did. I was on speaker when I was talking to customer care and the accounts person from billing department was there, so she overheard the conversation. She knew I was a genuine person with funds in my account and willingness to pay - just that the bank is causing troubles. She said - sir, please take a screenshot of your bank dashboard indicating that you have sufficient balance, I will mention this as proof of balance, write a letter and attach your ID proof / address proof copy. I will sign the discharge letter and you are free to go. Please make the payment once your account restricted flag is removed.

Having done the process, as we were prepping to leave, the accounts person visited and said - Sir, we have been using HDFC bank for about 20 years, never had such issues. You should consider moving to HDFC Bank. We previously had some issues with customer support of SBI Bank, so our payment gateway is now primarily linked to HDFC Bank and everything works flawlessly.

Reminded me of the legacy these banks have. Imagine, a customer, whose wife is stuck from being discharged, has access to money, but cannot use it - because stupid bank’s processes. They would immediately take the advice and move to HDFC Bank or whichever bank the hospital would have recommended as its a very old hospital, very trusted, been there for ages for all classes of people - from super rich to low middle class, everyone visits.

I am an investor in IDFC First and an investor in HDFC Bank. But I really believe in philosophy of IDFC First Bank - being genuinely there for your customers - but such experiences really hit deep.

For now, I will be moving my primary account to HDFC until foreseeable future.

PS: IDFC restricted for IMPS, but the destination of those IMPS was HDFC, HDFC didn’t even raise any issue, but they are otherwise very active on transaction monitoring when I make transfers or credit card payments to a new beneficiary. Shows maturity.

14 Likes

I too get restricted transfer messages for 24 hours on the days I do lots of money transfers. I consider it a minor inconvenience because it works for my benefit in the normal scenarios. This is for HDFC bank account transacted via BHIM app

I was paying money to 10 different people for a function and got flagged for large amounts. From a banking perspective, it’s good that these kind of systems are in place

Was it inconvenient? Yes it was.

4 Likes

Yeah, for me, its not the process, its the resolution when raised as a concern specially when its a time sensitive situation. I appreciate the process, but I find the resolution approach flawed.

I remember making a few forex transactions during a trip in 2019 using HDFC Regalia - I had their global something program active which allowed for low forex fee, as I made several small transactions, instead of blocking or anything, I received a call from transaction monitoring team to confirm it was indeed me.

The same happened when I made several small transfers towards a large purchase from Net Banking. In fact this time, as I was making payment to the hospital, that was precisely the behaviour - call from transaction monitoring team, that it was indeed me making several transfers one after the other. They made some other confirmations of details on account just to ensure they were indeed talking to actual account holder.

Anyways, to each their own.

5 Likes

Probably you should utilise UPI, which is instantaneous. RBI has recently increased the hospital payment limit to 5 lakhs per day.

3 Likes

I don’t think that’s the right way to look at it. That way we are avoiding the concern - that’s the bank’s processes which hinder customer experience.

Further development on the issue:

- The “Debit Restricted” flag was removed a few hours later

- However, in the evening, “Total Freeze” flag was added to the account out of the blue.

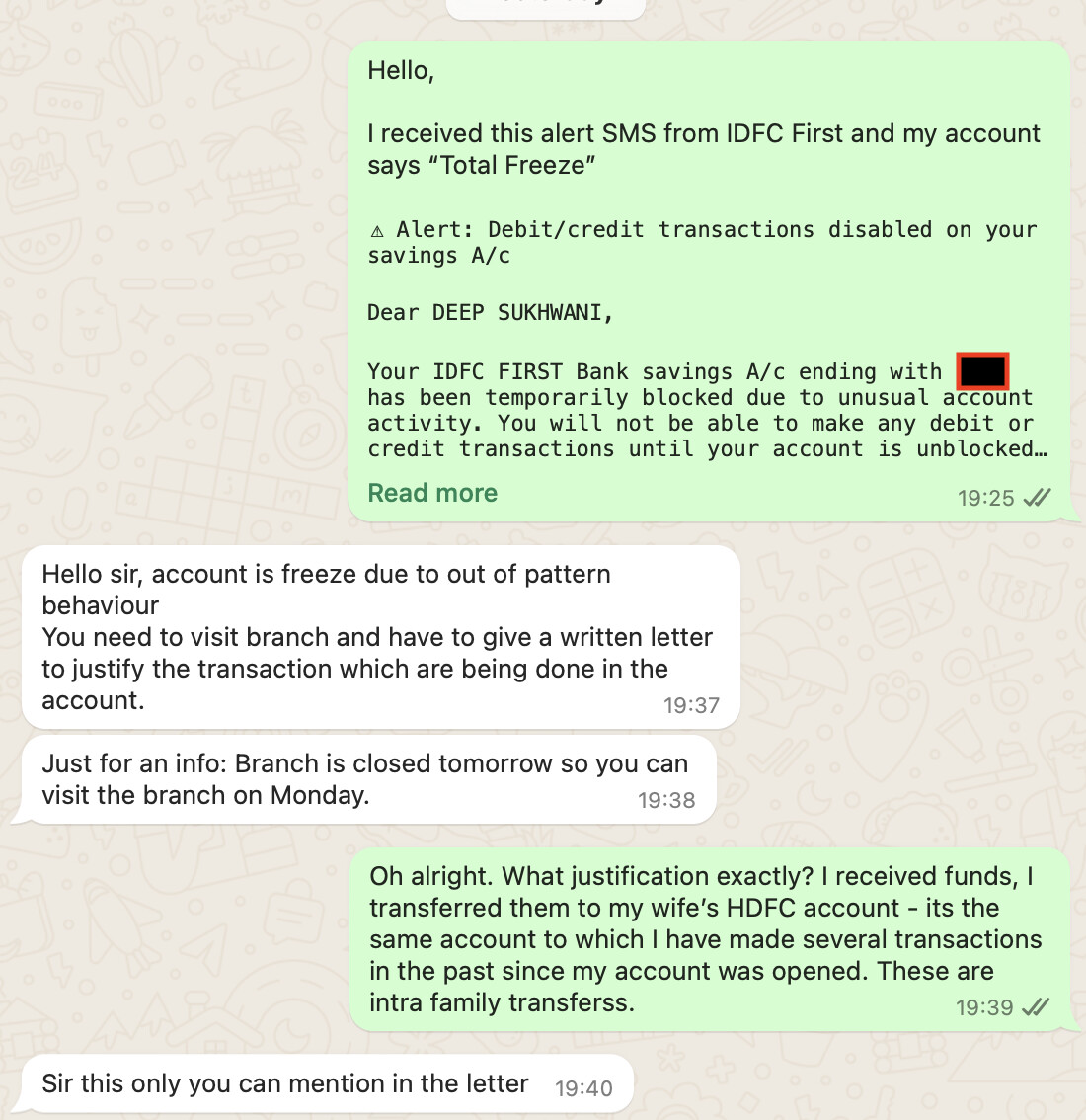

I again sent emails on the same thread, also reached out to the branch executive in nearby branch. The branch executive said, you’ll have to visit the branch - write a letter justifying your transactions

Anyways, since this thread is investment focused and not customer grievances one, leaving it here for now.

I have started the process of moving my family’s accounts out of IDFC First for now because I feel uncertain of such customer-unfriendly behavior - specially freeze out of the blue. Imagine being stuck right when you need the funds and bank’s processes / bureaucracy shuts you out forcefully - as in this situation.

To each their own, I am still a very tiny investor, might increase / reduce stake depending on bank’s economic prospects but not planning to become a full-on customer anytime in near future.

5 Likes

Further update (this one’s investor oriented hence posting it here)

Received call from senior management, they took in the profile level details to determine whether things are genuine in nature, shared their observations within the team that takes care of account freeze.

A few hours later, received another call and they shared that they are working on getting the freeze taken off and additionally posting in some reward points as a way to compensate for the inconvenience.

The responsiveness was quite appealing, usually banks have their set timelines, and its almost naive to expect such involving concerns to be addressed on a banking holiday.

Hopefully, the team works on designing process such that going forward this does not happen again and if it does, I hope others share their feedback publicly so we are informed as investors.

As an investor (and ofcourse as a customer too), I am happy that the management seems genuinely concerned with customer experience so much so that during the fast moving / heavy-workload time of quarterly results (expected to be announced later this evening) they took time to address a concern which might as well have pushed to the following Monday (given today is not a working day - 4th Saturday).

PS: The person whom I spoke with follows ValuePickr forum.

10 Likes

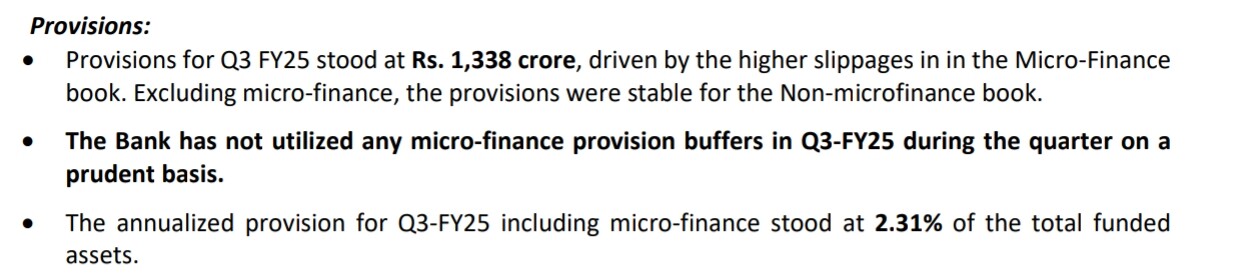

Results out. Net profit 339Cr with decent NPA numbers. Provisions are less compared to last quarter, but still high considering the fact that last quarter’s provision was supposed to take care of almost whole MFI book.

https://www.bseindia.com/xml-data/corpfiling/AttachLive/33f438f6-b7e7-4143-b4aa-d55b4ce08616.pdf

2 Likes

Same here, think they are pretty decent results. Amazed at their growth of Deposits, seriously. And frankly, how is their ex MFI credit cost so low for such yield?

But it is not clear if they have used up the provisions they created in SMA 1 and 2 they made in Q2 25 for MFI, some 320 odd crores. If they have used about 50% of that and kept some buffer for the future, I would be happier. If they have used up everything, then well, nothing to be excited in this results.

If they have not used it at all, and still posted thsi result, Ill be happy. Seeing how conservative VV has been all these years in providing for corporate loans, Ill be disappointed if he used it all up.

Have been searching for investor presentation to get this information, new PPT is not yet available.

Most importantly, we need to see what is their guidance when they expect credit cost from MFI to peak.

On a separate note, after seeing Deeps message, am concerned what if they block my account for transactions! am entirely using them day in and day out, love their app and their services. But after seeing Deep’s message, may need a backup bank. Though not sure who can be as good from a service point… maybe hdfc… they have a large branch network

6 Likes

.

they have not used the provisions it seems,

.

What could be the reason for such big increase in other operating expenses though…PPOP has decreased for first time after many quarters due to that…profit would have been higher otherwise…

Also I expected higher profits this time as 250 crores of provisions during last quarter was one time item.

5 Likes

I’ve had a similar experience with them during a credit card issue. An escalation solved it. It was more of an SOP problem than the customer service people being unwilling/difficult to get a hold of. Their customer service is unparalleled in the industry. This is one of the reasons I believe they will do will. Banking is essentially commoditized. The difference is quality of service and responsiveness.

- Their account opening process is amazing with doorstep services as well.

- The app is convenient and I’ve never had any troubles accessing funds.

- The quality of credit cards is good and priced to make business sense.

- Grievance redressal is good (have faith in the process and escalate sequentially).

The only area of concern would be credit quality. During their growth phase, they did a lot of C2C card acquisition. I hope that doesn’t come back to bite them later. With the way disclosures are structured, you’ll never know what the actual credit quality is. Looking at delinquency isn’t good enough. It essentially comes down to having faith in the management - much like with Kotak.

Disclosure: really hoping it goes back to sub 50 levels to make a large one time purchase. Hope it comes up in the coming few months. There is no way they don’t do well in the long run if credit costs aren’t managed.

4 Likes

For me the results are very disappointing.

Quarter after quarter they keep saying but the Cost to income is not in control.

PPOP should not get hit in such a big way with just MFI loan issues. If microfinance book is just 5% odd with say 10% gping into NPA thats additional credit cost of 0.5%. Said that PPOP should not have gone down.

All in all the results are very disappointing with no NPa controls in NPA side especially MFI.

Unsecured loan can now get affected next like consumer loans, Personal and Credit cards.

Very disappointing to say the least.

8 Likes

We should wait for them to explain the sharp increase in “Other Operating Expenses” approx 380 Crs.

Maybe it’s invested in growth, which is what we want. Growth won’t happen without it.

provisionings are there, other banks too are facing mfi crisis so I guess it’s part of high risk mfi business. the management has a handle on it since it curtailed exposure couple of quarters back.

RBL Bank np has fallen 80% YoY.

Kotak Bank np has been falling for two quarters. YoY is also very low.

Axis Bank YoY growth is only 3%

so this spells out to me that the banking sector is going through a bad patch. To judge this Bank based on the current performance would be doing injustice.

Money is made on betting on the future.

6 Likes

Kotak and Axis Bank’s profit were normal …so no growth on normalised profit …

in IDFC First’s case people are waiting for many years for profitability to get fixed…

RBL is trading at P/B of 0.6,

we should exit IDFC First if we feel there is a need to compare IDFC First with RBL or Bandhan.

5 Likes

Point I was trying to make, which got missed, was that banking sector is going through a bad patch. In that, Idfcfirst has managed to grow in areas which it can control and guided. It has a plan in place.

As for the time it’s taking to become a good bank, like Kotak; It issued Guidelines 1.0 and fullfiled it in a timely manner, we all can agree with that; regardless, the market agrees is why we saw 100+ on market price.

Now, guidlines 2.0 is in place.

3 Likes

I have now come to realise that people were comparing this bank with RBL Bank et cetera … and saying it should trade at 0.6 times book are making a huge mistake. imo, pls give counter arguments it will make me see better.

If you see my old posts I used to say this all the time. I used to say this bank is an overvalued bank. I used to say when the bank has no core operating profit (remember CORE PPOP was less than 0.8%, even with normalised credit cost of 1%, this was 0 ROE Bank, forget the large bad loans), this bank was in the pits. Then they had no Casa, 20,000 crores of infra loans, I used to say why it should quote above price to book.

But here is my experience. I used to keep waiting for stock to come down. But unfortunately for me it never did. The only time this company came down to 0.6 Price to Book was in the ultimate depth of COVID, BVPS was 34 and stock came down to 20.

Prior to this, it was hovering around 40 (above price to book) for all of 2019-20 (prior to COVID). Why? At merger their share price was 36.4 and BVPS was 38.5. Why was such a non existent franchise quoting above price to book? we can safely say COVID horror show was the worst time, that too for a bank with worst financials + COVID it was at 0.6 p/B

This is not COVID scene. so dream baby dream for this to be 0.6 B. I too do.

So now i am realizing if someone is for ever quoting above book, then maybe it is the right price ( whatever the crazy logic of the markets)

Now talk of customer experience. we must be crazy to compare this banks customer experience and brand with RBL. IDFC brand and customer experience is many notches superior. It is s superior to Indusind by a huge margin, culture is many times better, ive spoken to branch staff. You cant even compare. App is better than all other banks including big banks. Delivered on 1.0. Growth is there, they have shown their brand/ customer service prowess by fixing deposit side issues. so probably market is valuing all this we dont know. The only other mid tier bank is Bandhan. the less said the better totally useless tech. So I feel in the mid tier bank banks this is the only real bank which can enter the top 4 club.

am too waiting for stock to correct, waiting and waiting. waited all of last quarter after they posted terrible p and l. somehow market is valuing them where they are.

13 Likes

IDFC First have not delivered on guidance 1.0,

they missed all the metrics like profitability, ROE and ROA, which matter most for an investor by a huge margin.

only few quarters back, and probably after dec,2023 (as bank has said they started seeing stress in MFI segment during dec,2023 itself), vaidyanathan declared on national television that they will do a profit of well over 1000 crore in Q4 of F.Y. 25.

I will be happy if they even do half of that.

honestly I don’t know how much of that valuation which this hank gets is based on facts and substance and how much is because of brilliant marketing skills of Vaidyanathan.

Invested in this since Jan, 2019, and will keep holding until end of F.Y. 2027 probably…if they don’t deliver on their ‘promise’ of ROA of 1.4 by 2027, that will be the last lie for me at least.

9 Likes

How can there be deffering views on Growth 1.0 metrics which management promised and whay they actually delivered?

Can someone settle that with actual facts?

I believe CI ratio has heen a perennial problem for them im ROA/ROE tree

2 Likes

I think real problem in this bank is heavy dilution of stocks…This management is giving lakhs of shares to employees as ESOPS if one has to cross check you can go to link Bank Announcements | IDFC FIRST Bank and just search ESOP. Month on month heavy dilution is going on in this bank under name of ESOP. Vaidyanathan should dedicate one slide also for this in presentation instead of giving details about Capital First.

9 Likes

All said and done they have not delivered what they guided. For an investor, all operational efficiency and input is seen in ROEs and nothing else for a Bank. There are hundreds of moving variables for any business and it cant be excuse for not being able to deliver on guidance. Every time for more than 5 years and you still make excuses means you are not able to navigate potential future issues to give proper guidance. Best to guide less or dont guide if one cant deliver. Some time back they said they will deliver 40% operating profits for next two years but they have missed it with huge margin. They arent the best bank for investors as they were thought to be. All said and done they are indeed a good customer franchise with good interest rates on deposits and good technological adaptiation and zero fee banking.

7 Likes