how can an october occurrence be part of sept results? which accounting provisions allow for statement in this way?

Because technically, it is an adjusting event based on subsequent events which confirm the state of affairs as of the reporting date. You can google subsequent events provision in google and understand it, pretty simple and important concept.

IMO accounting wise also and otherwise also it’s better they clear this out in Q2 itself so there is higher chances of good numbers in Q3 and Q4.

The way I have ben learning investing as a newbie, I believe in looking at the core banking performance and all the small things that eventually compound. Having said that, IDFC has been delivering on each of those compounding steps well (except for the CTI which slightly concerns me too). Further, only and only good processes yield great outcomes and VV has been communicating fervently the underwriting processes they follow etc.

Having said that, IMO the core business has been delivering good numbers. And as a Finance professional myself, I truly believe in over communicating and over provisioning (say SMA1 provisioning) than not do it (BTW over provisioning is conservative and not aggressive as someone mentioned above). Banking business is inherently always going to have credit risk and always some or the other sectors are always going to be hit, what matters is the credit cost expectations of the investors before they buy a bank stock, for me anything below 2% and 1% is great and at all times, in all scenarios as long as this number is being maintained, that’s good especially for small retail / MFI loans which are unsecured.

The only change in my expectations (again as someone else mentioned above) is that earlier everyone wanted a quick 3-5x in 3 years time frame and the reality is now that it may take 5 years or more to get there, so this is more about a long term game. As such, what needs to be tracked is long term processes, long term business matrices etc than worry about quarterly numbers. IMO great time to add if people have liquid cash and they are managing risk.

And yes, IDFC’s biggest risk (from a retail investor POV) would always be VV’s KMP risk as we are all betting on him (as any VC bets on the Founder more on the business).

PS: I am holding and biased!

10 Likes

Sorry to keep coming with negative impressions and negative things. the management has not given rosy guidance for Q3 or Q4 either. All they are saying is it will be better than q2 25. Yhats obvious.

But consider that the credit environment is not benign and technology investments continue.

So profit will increase from Q2 25 Does not mean by any stretch of imagination that it will be more than Q3 24. in fact if you see the print of interviews it kinds of kind of hedge they are taking in their interviews, i have a bearish feeling about q3

it it only says it will be better than Q2 which is obvious.

We should not raise our expectations and scream later.

On a parallel note, I am frankly quite intrigued as to why so many of us are sitting and discussing this stock so much?

There are over 3000 posts here, no other bank is debated even remotely this much

Are we getting a vicarious pleasure going through the rough and tumble of this stock? And even more vicarious pleasure watching VV struggle with a bad purchase of a bank?

on one hand they are doing brilliant things on brand technology customer service smell image, deposits, improving ppop by 30 pc cagr, etc on the other hand ppop is not even 2.5%

admitted it has come from zero to 2.5 but still 2.5 is still low compared to indusind which is say 5% (but they dont command the good smell and stature of idfcfb)

we know very well it may ttake atleast 5 more years to even get to industry benchmarks

meanwhile big banks have already been through the rough and tumble during the last 2 decades and are sitting pretty with good roe

then why are we still stuck here debating everyday.

Why are we not simply switching away to a ICICI Bank get assured increase in book value and stay at price to book of 3.5?

Why stay with the bank which will make low Roe and bet that price to book will go up? should investors not just go and purchase peace?

Somewhere I feel we are getting a kind of thrill participating with this management’s rough and tumble. Or because of personality of vv is causing this odd kind of illogical attraction in this bank?

Or are we learning from a mysterious case where there are many positives and many negatives.

We are also probably getting a pleasure watching a successful entrepreneur buying a bank and watching him going through the rough and tumble of fixing his purchase.

If we sell out we wont have any interest in the debate. We are probably enjoying the struggle of a leader who is trying to turn around his debatable purchase?

At idfc we have to depend on a low 10 pc Roe bank increase its P/B from 1.3 to 2, if so,

53×1.1×1.12×1.13×1.145×1.16 =98…

am assuming modest numbers here, and not factoring bvps increase by raising capital at a premium if any.

for 20 pc growth 16 Roe good tech peace of mind governance bank)

At p/b of 2.5

98×2.5 =245 ( 245/ 67 = 3.6 x of todays money)

At 2x p to b, it would be 98×2 =196

196/ current price of 67 = 3x

Vs

in an icici we can be assured of high Roe

Their equation would be

136×1.17×1.17×1.17×1.17×1.17 = 855 … if they retain their 3.5 crown then their stock could be 855×3.5 = 2992 so stock would be 2.2 X of today

So which is more likely

A. idfc becoming Roe of 16 and reaching 2X or 2.5X p/b where we make 3x or 3.6 x our money? Or

B. icici Compounding bvps at 17 (roe) and retaining p/b at 3.5?

If we believe B is true we should switch out of our current position

If we believe B is true we should stop shouting and calling names getting frustrated with every bad result. We should trust the capability and intent of management and live with the rough and tumble that will come with this journey

If I am unfair or made logic error or mathematical error pls point out to me I am human

After all as of today, vehicle idfc is weaker franchise has low ppop has low roa low Roe

no matter how good or worlds best management it is, even if it is VV, he can only fix roa roe slowly over time. Because he has to constantly invest into every business and go through the J curve

Meanwhile the startup bank will have thinner skin, every small change in ecosystem, change in regulation will affect thr P and L and more will give heart attacks…

why are we self flagellating and going thru all this stress? Why are we not switching over to sy an icici and be more peaceful? Please educate our psychology so that we learn about ourselves.

Icici core vehicle is stronger, has been through its rough and tumble since 2000, and has reached roe of 17. More assured to deliver good growth in bvps. Retaining p/b at 3.5? Pls guide on the probabilities

Which is more likely? What is going on?

18 Likes

Vv could argue ofcourse that merging with idfc was not a mistake, saying capital first needed funding lines which could not have grown to 1.7 lac cr (todays 2024 Retail Agri Msme book) from 32000 cr (RAM book of 2018).

Cant tell, since i have been ranting against the purchase of or merger with idfc bank

Views pls

3 Likes

I’m a relatively new investor into this bank, invested to play the IDFC merger premium.

I went through the investor presentation and was trying to understand if anyone has more details on the breakdown of provisions other than the prudent provisions on Toll and microfinance book.

2 Likes

This is regular banking event. If one needs to stay in touch with banking good to hear.

Not specific to IDFC First Bank though Vaidyanathan is one of the speaker participant.

3 Likes

Have you seen too many companies going through the pain of explaining visually (through material similar to what they share in investor presentation) why the shareholders should vote to reappoint the managing director. See pages

1 Like

IDFC First bank is one of the top 5 lenders to Fusion Finance (Ref Q2 FY25 Fusion Finance earnings call: https://youtu.be/PJ5n9S-iqbU?si=frffcM0EDrHwaMyR 22:55 min mark)

As per above article “some lenders have given waiver for Q1 and Q2 only”. If some lenders have given waiver to fusion finance then Vaidyanathan as (as per his nature) will provide in coming quarter and eat out full quarter pnl. But this loan seems to be given under his tenure and not legacy loan.

2 Likes

Warburg pincus is their promoter with 52 percent stake. They will subscribe to the rights issue. If they dont the company will go under and RBI will never let another PE firm buy into any NBFC ever again.

So in a quarter CET1 will go up, provisioning will be made and balance sheet will degrow, till npa s are flushed out. Maybe even business model will change.

Probably the ceo will get fired as well once the rights issue is done.

If the covenants were breached in q1 and q2 most banks gave the waiver thenthey probably already knew about it . This will be a good test to see if VV actually had the chops to look ahead and provision conservatively ahead of time. He has already said that microfinance will lead to extra 150 crores of provision each quarter for the next atleast 2-3 quarters

Short term : there will be lots of noise drama media chest beating etc etc but with the PE promoter this should be a low risk event

Disc : invested in idfc and not in fusion finance

5 Likes

“Low risk event” What do you mean by that?

Do you mean the loan is actually on the P&L of Fusion so after 2-3 months anyway from the rights issue atleast fusion will return it back to lenders so lenders carry the risk only incase fusion micro is not able to avoid bankruptcy?

Low risk event = bankruptcy of fusion.

Since the media has already highlighted the news that one of the audit firms has raised questions on the viability of the fusion as a going concern

The article mentioned above says idfc first is among top 5 lenders to fusion with exposure more than 500 crores. We dont know the exact quantum Of exposure

1 Like

Exposure to Fusion Finance seems to be 263 cr, as per the below link

2 Likes

The latest numbers are much higher, as per C.R report dated Oct, 2024.

3 Likes

Now that we have the quantum of exposure i will revisit the conversation

Is my assumption correct that if Fusion microfinance survives due to its rights issue than it has to payback the loans to SBI and idfc first.

Post successful rights issue the risk should move away from P&L of the lenders atleast and what happens with fusion stays with fusion.

Than we can say it is low risk.

Otherwise what are the other cases.

Can they ask banks to take a haircut.

If so

how much more NPA can idfc can have, maybe like 100 crores max for 343 crore loan.

100/150 crore provisioning i guess should be ok ( I am taking the liberty to consider that last quarter provisioning got nullified by the 600 cash added in books).

1 Like

Here we go…

1 Like

I haven’t had the chance to verify most recent Adani exposure of IDFC First, but I hope it is still limited considering the conservative nature of the IDFC First’s management.

1 Like

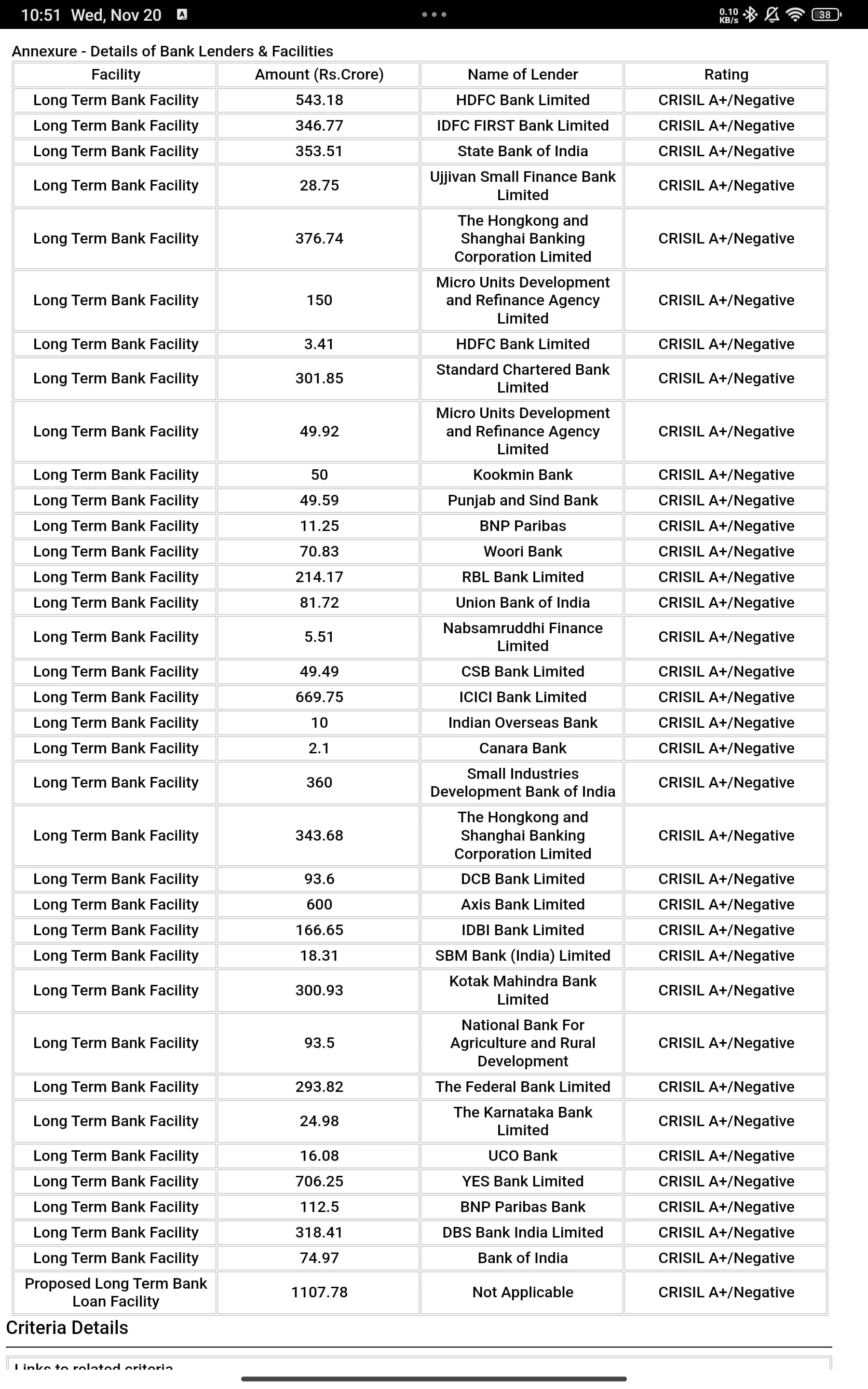

They have at least 750Cr exposure:

400Cr exposure in Adani Ports via IDFC Limited (looks like one more legacy item).

250Cr exposure in Adani Enterprises directly via IDFCFB (not legacy).

Found these on free versions of Crisil and Care ratings websites. There may be more hidden/indirect exposures - I’ve not done extensive searches.

On top of these, there is about 345Cr exposure in Fusion Finance…

There goes at least next 2 quarter profits in provisioning, unless Mr. VV has already provisioned for some of these ![]()

4 Likes

Just because the stock price fell, how does that impact the revenue of Adani group companies ?and If revenue impact is minimal how does it affect the debt servicing ability?

8 Likes

This reflects the way we started to see this bank. every quarter we started to anticipate new reasons for provisions … Thank God its still in black and not in red yet

2 Likes