The growth in assets QOQ is decent even if it’s lower than last quarter, however the big issue this quarter is the hit the bank will take on their Treasury book due to the increase in bond yields. The 10Y Gsec has moved up by around 60bps in this quarter alone which is an 8.5% move. This is more than close to double of what it moved last quarter and IDFCB had reported a loss of Rs 9 crores in Q4 on account of this. IDFCB has an investment book of Rs 40,000cr and a further investment of close to Rs 20,000cr in NCD’S etc. That’s a total of Rs 60,000cr that will be impacted. Now all bonds don’t need to be MTM but even if we assume that half the holdings need to be then even a 2-3% hit on that book of Rs 30,000cr will mean a loss of Rs 600-900cr. That’s massive for IDFCB as its PBT is just around 450cr before accounting for any trading losses. So my question is are we looking at another loss generating quarter for IDFCB? If bond yields move up to 8% this quarter as predicted by many economists then will we have another loss in Q2? The losses are notional yes but it impacts the reported profitability and if the first half of the year is a total washout earnings wise then we are looking at a low single digit ROE for FY23 as well. I am a long term bull on IDFCB but every year seems to throw up a new surprise, and frankly I find it hard to justify even a 1x P/B multiple for a low single digit ROE Bank in the current market.

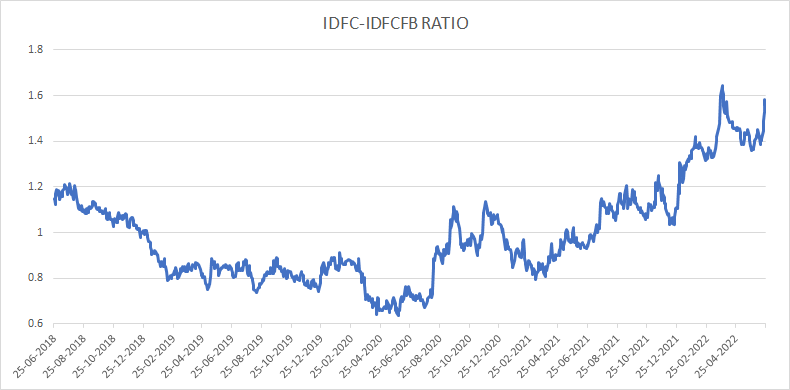

I have all my exposure to IDFCB via IDFC and I am going to use the current 20% appreciation in the IDFC stock to reduce my exposure by 50% and move into cash until more clarity emerges on the earnings. As mentioned by @Puch above the IDFC-IDFCB ratio has moved to 1.6x, which is at top end of the range and considerably reduces our margin of safety. At best the merger ratio will be at 1.8x but even that is a good 18 months away and I am worried that the AMC deal might collapse as market conditions have changed significantly. At a 1.6x multiple I don’t feel the margin of saftety is sufficient and I am happy to wait on the sidelines for a better entry price. Lastly if you see the current delivery data on IDFC then you will see that it’s the lowest its ever been at just 14% on Friday. This means that the increase in the price currently is being driven not by long term buying but by day traders. The stock is up by 22% in just 10 days and close to my average price, so will utilize this opportunity to reduce my exposure.

Edit: Added delivery data below-

Edit 2: IDFC-IDFCB ratio-