I’ve made a similar projection too. This one accounts for provisions.

The sources of my assumption about guidance are as follows:

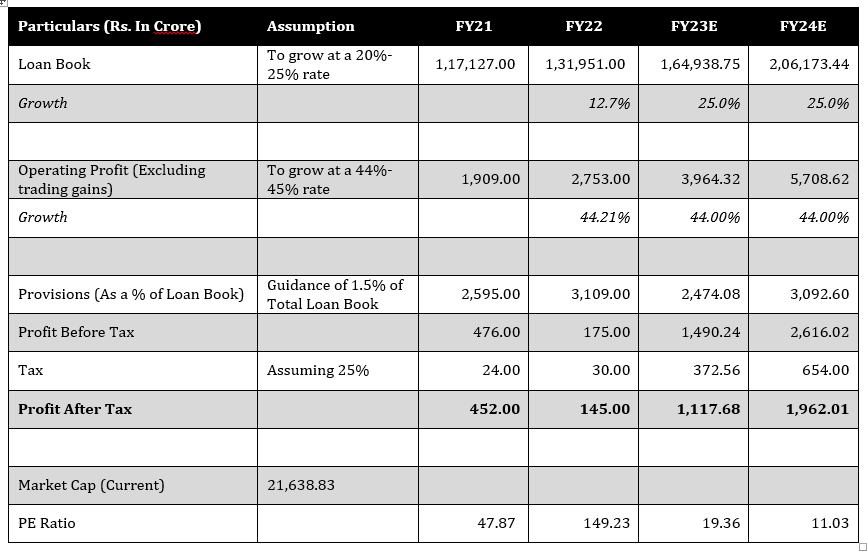

LOAN BOOK GROWTH

-

Q4FY22 Investor Presentation

“Loan book to grow from here on: We have made significant progress during the last three years (FY 19-22). We expect the loan book to grow at ~20-25% on a sustainable basis from here on for the foreseeable future.” -

Q4FY22 Earnings Call

“You see that if you were to get a sense of where the loan book will grow from here on for the next few years, we think that to grow the loan book from overall loan-book, retail, wholesale all put together to grow that and between 20% to 25% it should be very possible.” -

Interview with Financial Express

“We are starting from a small base in the context of India’s size, and in India, growing 22% from a small base is not a big deal. We have strong capabilities for credit appraisal in all our businesses. We are also growing our wealth management, cash management, trade solutions and deposits. All of these can grow at 25% comfortably from our base.” -

Interview with Business Standard

“Now we feel that each of these businesses, whether its consumer loans or wheels or SME or home loans or loan against property, everything will grow in this country. So, so really for us to grow 20-25% on home loans or other businesses it’s really no problem at all.” -

Interview with ET Now

“This year we are expecting credit growth – retail, wholesale all put together – to maybe 20-22%.”

OPERATING PROFIT

-

Q4FY22 Investor Presentation

“Strong Growth in Operating Profits: While the loan book grew by only 13% YoY, the Core Operating Profit has risen by 44% from Rs. 1,909 crores in FY 21 to Rs. 2,753 crores in FY 22. This clearly demonstrates that our incremental business is highly profitable and we are beginning to see strong improvement in operating leverage. We expect this phenomenon to continue to play out over the next few years, which will result in increase in overall profitability and ROE” -

Interview with Financial Express

“What is your key focus for FY23?”

“Profitability. We have addressed assets, asset quality, deposits — everything. Now it’s only profitability to be addressed. It will happen from this year. You will see a sharp increase in profits in FY23. Our operating profits grew from Rs 1,900-odd crore in FY21 to about Rs 2,700 crore in FY22, a growth of 44%. We expect another similar jump in profits in FY23 and … in FY24 also. That’s the pace at which the profits are rising at our bank. One day, you will suddenly wake up to the potential of our bank.” -

Interview with Business Standard

“Last year our operating profit book grew by 44%. We expect that next year as well, and the year after that we believe that sort of track can be maintained. You can watch the results to get more confidence.” -

Interview with ET Now

“Last year, our loan book grew by only 13% but the operating profit grew by 44%. It reached Rs 2,700 crore this quarter. Now that tells us something about how the operating leverage is kicking in. Our own sense is that operating profit can again compound by another 44-45% next year and by another 44-45% the year after that. That is how we think the numbers will play out.”

PROVISIONS

-

Q4FY22 Earnings Call

“At that time if you recall I had publicly said to all of you that our Q2 provisions will be less than Q1, Q3 will be less than Q2 and Q4 will be less than Q3. I’m happy to share the following numbers with you as it turned out. So, our gross Q2 provisions were 475 crores, Q3 provisions were 392 crores and Q4 provisions are only 369 crores. The sum total of all these four numbers are Rs. 3109 crores. Now our average loan book for the year was ~Rs. 1,18,700 crores. If you divide, you’ll get a number of 2.5% to 2.6%. Now you can think and calculate for yourself that in a COVID ravaged year, where Q1 was so hard hit and by the way, in Q1 there were lockdowns across the country. I can’t say across the country but across the large number of states, is practically a national lockdown but there was no moratorium. So, slippages were there. This despite such a quarter and a year our credit loss for the whole year was only 2.55% to 2.6%. You can do the math, somewhere there between the two. I think it’s 2.6%. So therefore, if a COVID ravage year it was 2.6%, really, it’s not hard for you to also believe us that next year when the guiding just for 1.5%, we have done our math for that. If we take annualized credit loss then for Q4 our annualize credit loss was only 1.2% now. So that’s 1.2%. We are guiding for 1.5%. We kept ourselves sufficient cushion when we say that next year, we’ll do 1.5%. Therefore, there is enough data by our side that when we were running this, so earlier it was 2.5%, now even in a COVID year its 2.5%. Now we’re guiding for 1.5%. So, you get the drift. Therefore, we believe that we are building pretty much a phenomenal model at our end where we are able to lend to multiple segments of the market” -

Interview with Financial Express

“Also, provisions are down every quarter. In the latest quarter, annualised provisions are only 1.2%.” -

Interview with ETNow

“For the upcoming year on the credit provision guidance, we are guiding for only 1.5% of the loan book and that tells us how conscious we are about asset quality. We are approving between 40% and 60% of the application that come to us.”