Was running the YOY comparison and the growth numbers look great for the retail portfolio, even better than Bajaj Finance.

| Q2FY21 | Q1FY22 | Q2FY22 | QOQ (%) | YOY (%) | |

|---|---|---|---|---|---|

| Retail Funded Assets | 59,860 | 73,673 | 78,830 | 7% | 32% |

| Housing Loan | 10,919 | 12,120 | 11% | ||

| Mortgage Backed Loans | 22,034 | 26,006 | 29,404 | 13% | 33% |

| Mortgage Backed Loans (%) | 36.8% | 35.3% | 37.3% |

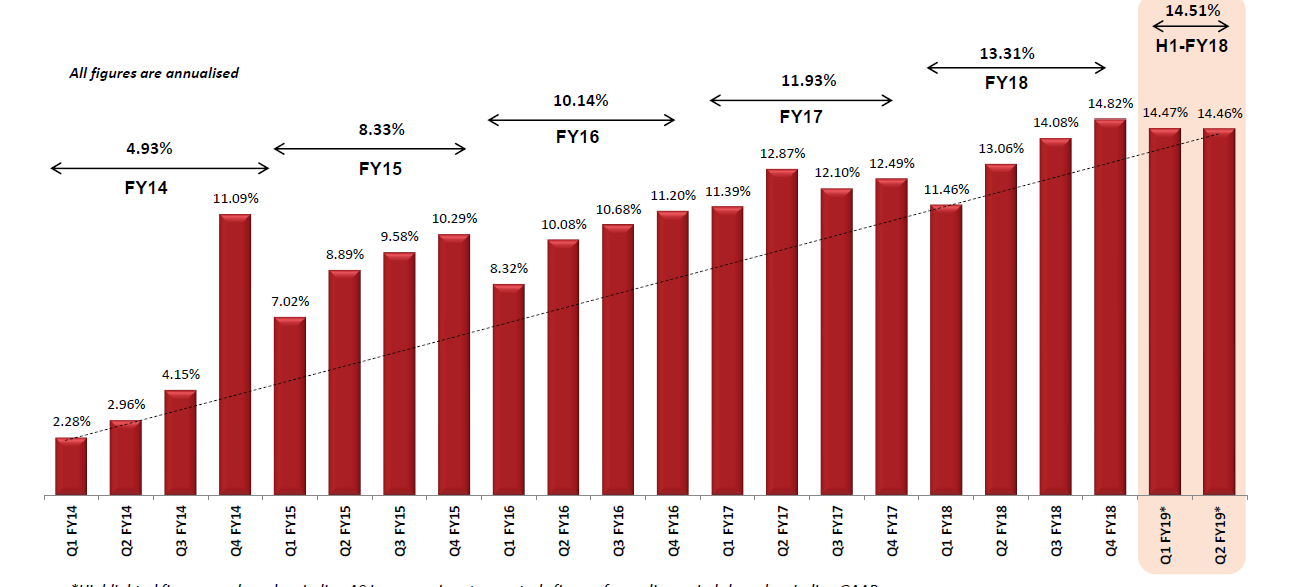

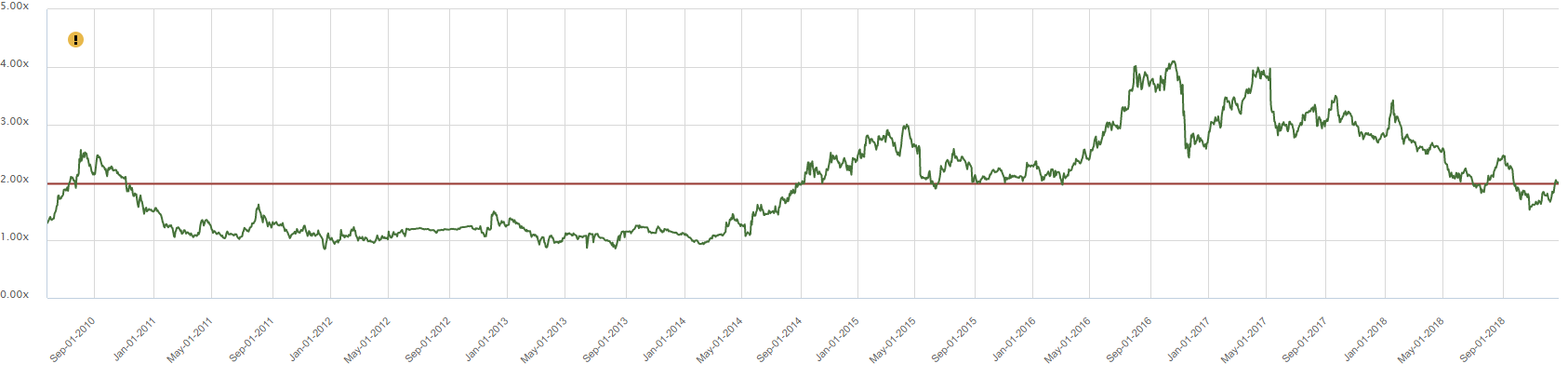

Also went back to check the historical P/B multiple progression vs ROE’s for Capital First (both charts below) and its interesting how closely it mirrors IDFCB. Till FY13 CAPF was loss making and turned profitable FY14 onwards with an ROE of around 5%. P/B multiples between FY11-FY14 were mostly between 1-1.5x. In FY15 CAPF started gaining momentum and had ROE’s of 8% and then 10% in FY16 and 12% in FY17. This was matched by the P/BV which started expanding FY15 onwards and was above 2x and even went upto 4x in FY17-18. Its clear that the P/B re-rating happens much before the ROE starts going up.

One could argue that IDFCB is today at a similar place to where CAPF was in FY15. The bank posted an ROE of 3% in FY21. If PPOP for FY22 turns out to be around 4,500cr (was 1,000cr in Q1) and Credit Cost comes out to 2,700cr (Roughly 2.5% as per mgmt estmates) then PBT will be around 1,800cr and PAT around 1,400cr which implies an ROE of ~7%. Next year as per current guidance/growth projections ROE’s shoud easily be above 10%. IDFCB today is still trading around 1.5x P/BV, so going by historical trends we should see a re-rating of the P/BV multiple soon.