I am refferring to following news,

News 1 >Status Change: Hudco may soon become infrastructure finance company - The Economic Times

- Hudco aims to transform into an infrastructure finance company (IFC) to access cheaper funds and reduce borrowing costs. (RBI) approval decision expected within a month or two.This will allow Hudco an access to a larger investor base, enabling diversification of resource base and optimization of borrowing.

- To qualify as an IFC, at least 75% of assets must be dedicated to infrastructure lending, with additional criteria including a net worth of ₹300 crore, a minimum ‘A’ credit rating, and a CRAR of 15%.

- Hudco is interested in financing projects related to energy transition as part of its IFC transformation.

- The company has been pursuing IFC status for nearly two years and submitted its application to the RBI on March 29, 2022.

- The government plans to launch a housing scheme in the interim Union Budget for 2024-25, for people in rented homes, slums, or unauthorized colonies, allowing them to buy or build their own houses.

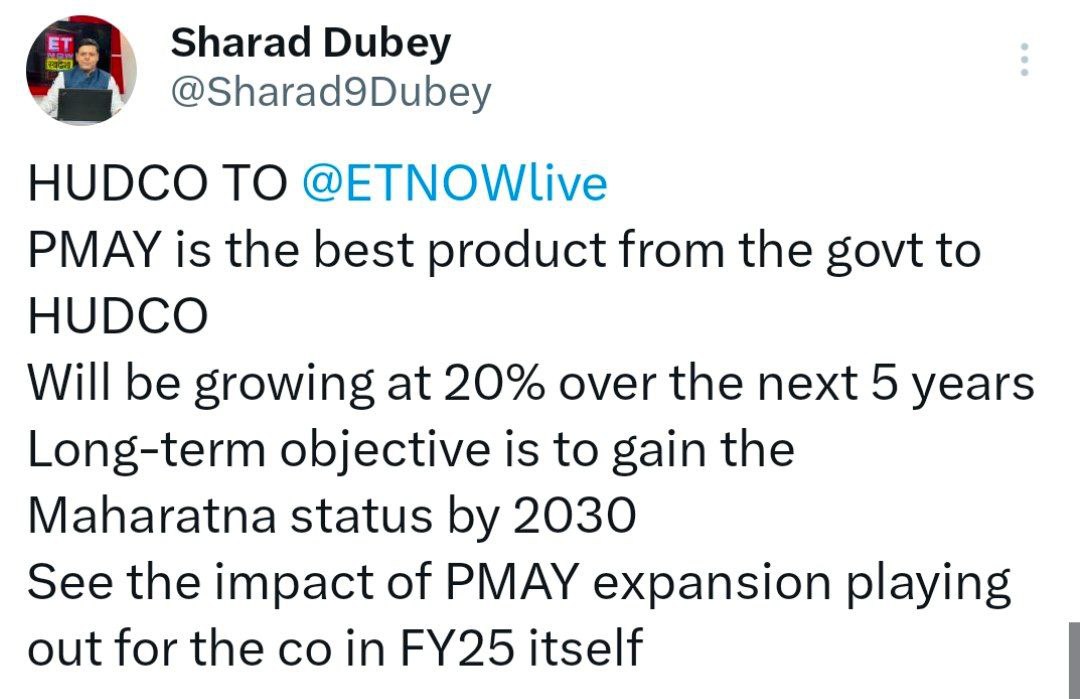

- Aligning with the ‘Housing for All’ mission, encompassing PMAY-Urban and PMAY-Rural schemes.Fin. minister highlighted the construction of 3 crore houses under PMAY-Rural and proposed an additional 2 crore houses over the next 5 Yrs to meet growing demand.

- The Union Budget estimates for FY25 for PMAY stand at Rs 80,671 crore, as compared with FY24 budget estimates of Rs 79,590 crore for the “housing for all”

- ₹25,103 crore is designated for PMAY-Urban to accelerate the ‘Housing for All’ mission, while the remaining funds support the PMAY-Rural scheme.

Query

What could be the chances that HUDCO gets an IFC status ?

If it gets IFC can it be considered in the league of IREDA,REC,PFC ?

What changes for HUDCO future earning with additional allocation in the budget and if it gets IFC status ?

Can hudco be more than just a PSU rally and be a long term bet ?

D-Invested~70s on PSU momentum…added at 200