Looks like an ad for equity deal a la Bennet Coleman’s Brand Capital

An interesting article on HT medias consolidation of the radio business.

Article Link - Consolidation in FM Radio Business – HT Media and Next Mediaworks Group

The merger seems to be the move to consolidate the network of one with funds of other. The transaction is designed in such a way that HTML will become the largest shareholder and the control will be with the HT Media group in the merged entity.

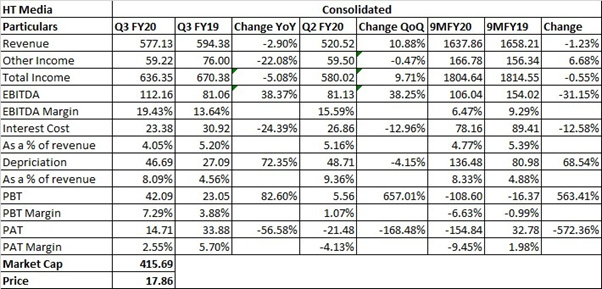

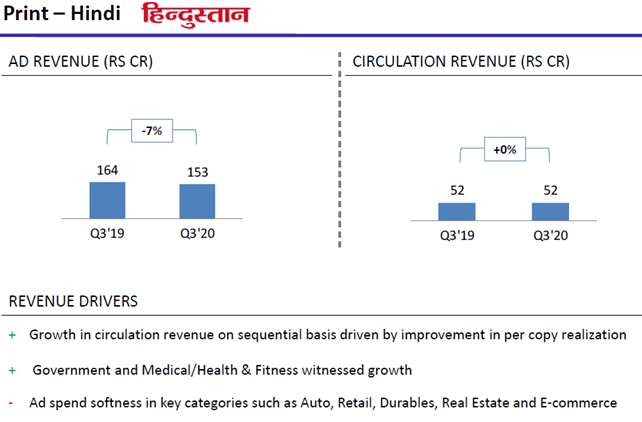

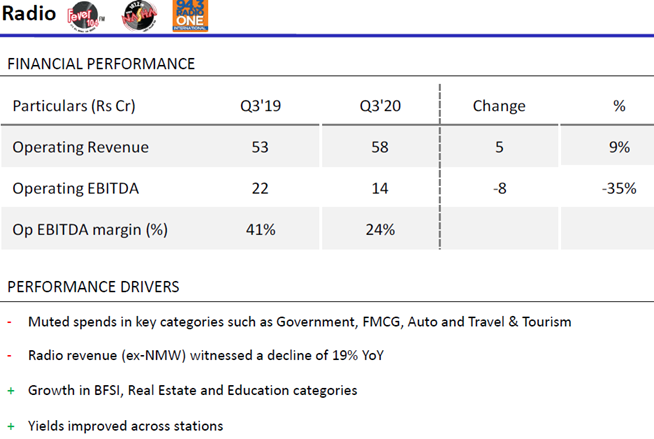

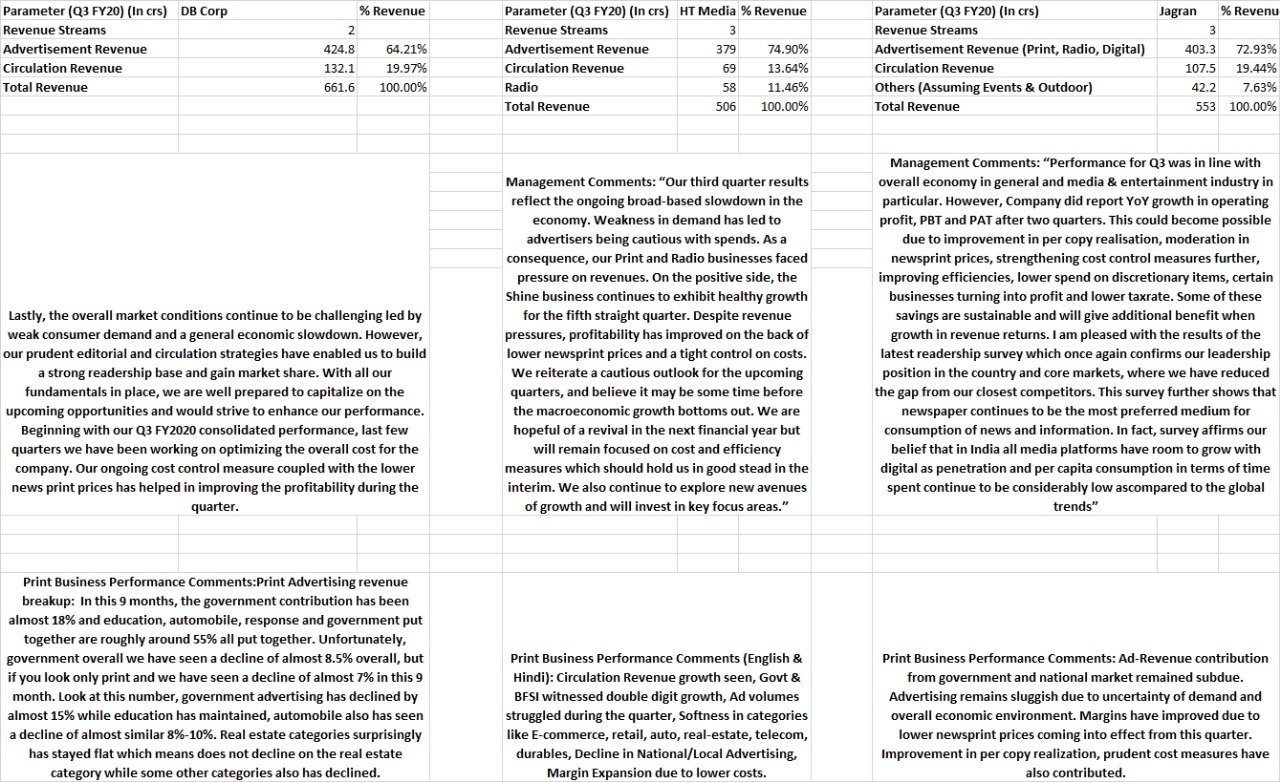

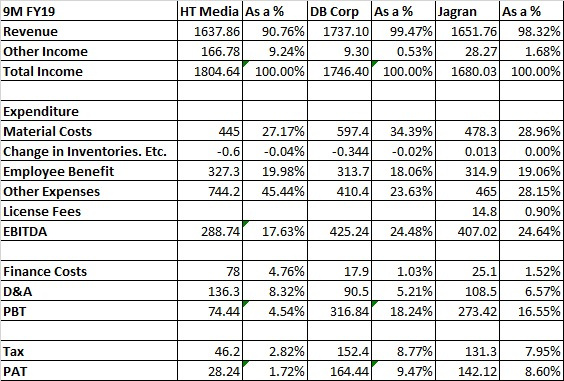

HT Media Q3 FY20 Results!

Q3 FY20 IP:

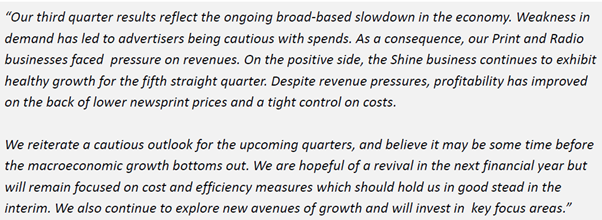

Chairman’s message:

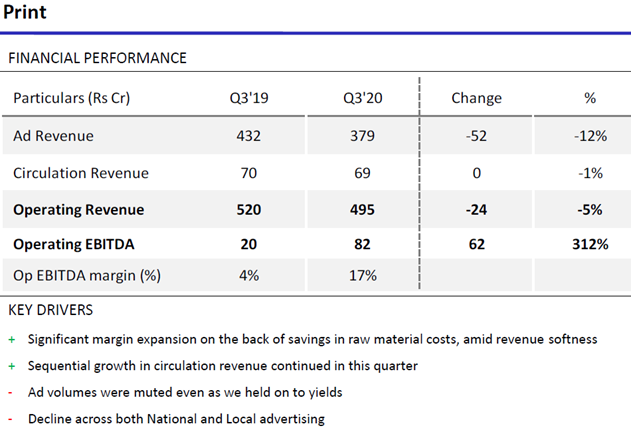

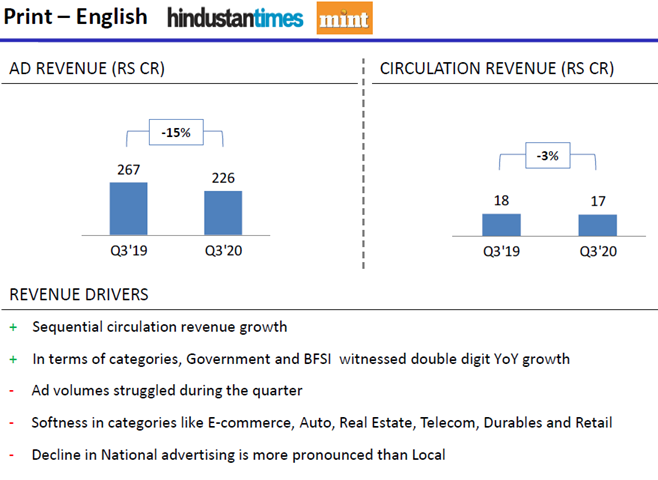

Q3 FY20 CC:

On the plus side, softer commodity rates and our continuous focus on cost control have given us good growth on operating profit and margins. We continue to be hopeful of recovery in ad spends as and when the broader economy revives.

No substantial decline in the newsprint cost expected in the future as it has already been decreasing since the last 3 quarters. The decline in newsprint cost is due to both reduction in prices and reduction in copies in circulation.

I think on the Radio business, we ourselves have been surprised for the last two quarters. If you see our results, or indeed the entire Radio sector results, there is quite a sharp slowdown which from the second quarter onwards is visible across. We are trying to take a lot of actions in kick-starting new stream of revenue, going much more hyperlocal and shoring up the revenues. But it’s very tough to say as we analyze, because we have, and indeed the entire industry has been caught a bit unaware on this thing. And we will see how it goes, but there are a lot of actions that we are trying to do in-house on that.

Profitability in comparison to FY18: Yes, look, I mean FY’18, you know, we used to have a growth coming on the top line, which was a big margin driver, so to say. Now with this six to eight quarters of perpetual revenue decline, there is a bit of a loss of operating leverage in the P&L, which is coming on to the margin. And if you also remember, that year, you know, we had just come out of a big cost project whereby we had improved the margins or the price margin realization had improved substantially. Newsprint prices at that point in time were benign. If my memory serves me right, we were in the zone of about 500 to 525 dollar a metric ton, where dollar was also not as sharply appreciated, which had happened last year. So, those things were contributing to the margin. Now, I really can’t comment on revenue. We have been hoping that the revenue will show some green shoots, though we see that in a few categories, but you know those are not sustainable enough for us to call victory on those respective categories. We are doing a lot of work, but I think for some time, we will be in this margin range of 19%, give or take.

Long term Strategy: So, let me give you a long-term strategy because this question has been debated, you know, on the quarterly calls even in the past. Two things that you are seeing right now is a lot of real estate which is sitting on the balance sheet. Most of this is our AFE business which is a separate line of business that we have been in for quite some time whereby all the real estate players who are looking for advertising but because of a certain liquidity condition cannot afford to do that. We basically take a risk and reward on the asset after doing a due diligence, and for part cash and part real estate, we kind of give them access to advertising. We believe and it has proved in the past that, of course, there might be some volatility here and there, but this is a good business because it gives us access to incremental advertisers who because of the liquidity situation might not be able to advertise and market their new projects, and we also get a strategic real estate play at what we would like to call a very favorable price, from a long-term perspective. The idea for most of this real estate is liquidation, and if you analyze our annual reports which will come out in three- three and a half months’ time, we are looking to monetize these assets and drive a decent IRR. The second point that you brought was about debt which is a classical treasury operation. Treasury is a very big profit centre. And though we don’t give the numbers because we are not publishing treasury as a separate category here, but treasury is driving a lot of positive EVA (economic value-add) on to a PAT level. So, whatever borrowing you are seeing either is for working capital or for CAPEX purposes where we try to access the cheapest source of borrowings, onshore or offshore, and not liquidating our liquid assets which are yielding us good returns in a risk-free debt capital market environment where we invest through various mutual funds, only on the debt products and never on the equity products.

From a group company perspective, nothing has changed. Monetization of the digital content because we see a lot of more advertising dollar going into the digital side, more growths are coming in there, so we wanted to have a larger play and up the game there. That’s the reason the Digicontent Limited (DCL) as a company was incorporated and subsequently got listed last year. Nothing has changed in this company. You know, if you look at the various sub-businesses on the digital platform that the company does, there is a growth of at least 20% in a segment and going up to as high as 30- 40%. But of course, the revenues are not substantial enough to cover off the print shortfall.

Now, what we did last year when we sold off the HMVL stake was because it was just getting too complicated having two parent companies, HMVL and HTML, and that is the reason it was done, and HMVL shareholders were compensated by cash at that point in time. But the digital company, the DCL, is definitely growing healthier, and it’s a double-digit growth which we also forecast going forward in the future year as far as the digital content businesses are concerned. Of course, there are some other areas whereby their revenues on the content that they produce for the print companies is concerned, which is the transfer pricing thing, and because the print revenues themselves are not growing, it is not helping, but all the pure play digital content businesses are growing in double digits and likely to grow even faster. If print does indeed pick up, that company will grow even more faster, but their pure play digital businesses are going very handsomely and very attractively at this point in time.

Well, from our perspective, at least, the margins have improved this quarter. So, that’s some as they call, the green shoots, we hope that the revenues now come back, which have been the big disappointment over the last many quarters now. While that starts happening, we will already see the impact of that coming through the margins.

On the cash side, of course, your company carries a reasonably healthy balance sheet and is perpetually looking out for more avenues to deploy the cash to generate sustainable returns for the shareholders. We hope the next quarter will be better than this quarter and there is an improvement which kicks back into the Radio business in which we have done some investment as well.

Disclaimer: Invested

1 Like

Thank you there is a lot of value. however the promoter chooses not to act. look at the low dividend payout. this is the most irritating aspect to institutional investors. they continue to keep this as ignore

1 Like

anyone still tracking this stock , looks absurdly cheap unless cash in the books is overstated.

1 Like

Hi, the shareholder returns on this stock have been abysmal. Having said the same, it will be interesting to watch the progress of Digicontent( listed company). This is the arm which earns revenue through Livemint. com and Hindustantimes.com. They have other digital ventures under this company too.

The media is obviously not a dying a field, unlike what many people believe. The strength of a media house lies in the strength of it’s reporting. Many of the print mediums have adopted a print + digital medium. Wall Street Journal, Barron’s continue despite the flood of information over the net. I am still observing and learning and hence my thought process is still WIP.

Disc: Not invested

2 Likes

So what it seems like , one should try to understand the other listed company as both are under same promoters so not much of difference for the promoters . I could see HTML giving unsecured loans to DG . One should question the management on the same, i hope they are doing quarterly concalls .

Hello I want to contribute towards background of promoter of this company.

Problem in HT media is even if the business is good the bad intentions of promoters destruct the wealth of investors.

The K.K birla had 3 daughters namely Shobhana Bhartia, Nandini Nopany and Jyoti poddar,

The company HT media belongs to Sobhana Bharatia the daughter of K.K Birla.

Now I read this article titled ‘samjha karo yaar’

Link here https://www.moneylife.in/article/samjha-karo-yaar-notes-from-an-annual-general-meeting-of-ht-media/51722.html

It reveals the standard of corporate governance of this company, also the attendant had questions regarding the large number of subsidiaries of the company, and his friend told him ‘samjha karo yaar’

Here samjha karo yaar means ‘understand they are like that only’

This is a major Red flag, also if the company holds so much cash then why does it not do buyback from open market to support share price?

Share price is 16.80 as on 14/12/20

Market cap is 384 crores

They posted a loss of 383 crores in FY20

Their cash and bank balance is just 43 crores now according to reinstated financial figures

Link for the annual report: https://www.bseindia.com/xml-data/corpfiling/AttachHis/d9eb5f3c-8058-46b1-9337-d0f360aaf035.pdf (uploaded to BSE on 6th December, 2020)

I remember cox and kings they had huge cash and bank balance I thought it was an undervalued company, but later the fraud was uncovered, similarly in HT media as well the cash is drained by posting losses, 383 crores of loss?

Shobhana Bharati also has a background in politics affiliated with Indian national congress.

Let’s look at her sister Jyoti Poddar, she and her husband Saroj Kumar Poddar now head the adventz

The companies include Texmaco ltd, Texmaco rail and engg, Chambal fertilizer, Zuari agro, Zuari global, mangalore chemical and fertilizer.

Last year Zuari Agro was rated ‘D’ meaning defaulter, also minority shareholders opposed managements plan for some complex merger and transfer of company assets.

So similarly Adventz group also dosent have good reputation in terms of their corporate goverancne.

In conclusion I would say

However great the business be but if the intentions of the promoter are not shareholder friendly then it becomes a big problem.

We must red flag and be cautious of all K.K Birla group companies

I am adding the list

Zuari agro chemicals ltd (company has defaulted on debt payments)

Chambal fertilizers & chemicals ltd.

Texmaco Infrastructure & Holdings Ltd

Texmaco Rail and Engineering Ltd

HT media + hindustan media ventures ltd

Sutlej textiles

Magadh sugar

Mangalore chemical and fertilizers.

Zuari global

Sil investment (this is another holding company from kk birla group, similar to Zuari global, under control of Nandini Nopany)

I have also written article on HT media (https://stockactivist.blogspot.com/2020/04/ht-media-management-issues.html)

And Zuari global (https://stockactivist.blogspot.com/2020/08/ZBL.html)

Highlighting corporate governance issues in the company

Notes: I have highlighted points on Management and corporate governance issues due to which I have red flagged this group as a whole, management and corporate governance problems can ruin even a good and strong businesses, I also don’t own any shares of HT media.

Also if anyone wonders how and why did they post such a massive loss of 383 crores for FY20, my reply to that would be “samjha Karo Yaar”

11 Likes

Though the future of this industry good or bad, Here is my thought

EPS from 2011 - 2018 from 7 to 13

Stock Price 2020 7 to 13

Debt reduce 2018 - 2020- TTM from 1,182 >>1,102>>927>>591

Disclaimer: Invested

Please see the profile of Mr Someshwar, MD of Ht and HMVL. They mean business. Yes franchise is below par vs mkt leaders. The co and peomoters too are finally consolidating the number of entities. Digicontent yo be merged back into ht media. Few loss making units shut. Shine.com has turned around. For sure the promoters dont deserve any praise, rather extremely poor approach towards shareholders. Not one ad-for-equity investment had yielded returns. Let us see how mobikwik goes. Immense immense value.

thy eroded shareholder wealth in texmaco, isnt keaoram also frm the same lot of sisters?

the article was hilarious. ht had an extremely inefficient incompetent subscription dept also.

Merger Has been rejected by shareholders between DG content & other group companies . The Valuation at which they were merging was never meant that merger would happen ,specially with DG content.

1 Like

Their podcasts business HT Smartcast seems to be doing well. I see their podcasts recommended on every podcast app

2 Likes

I think when you invest … you should look the business rather than its political affiliations