HT Media Q3 FY20 Results!

Q3 FY20 IP:

Chairman’s message:

Q3 FY20 CC:

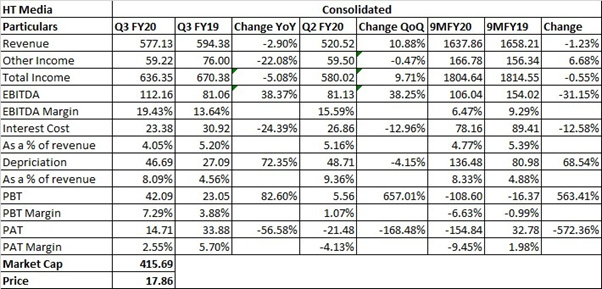

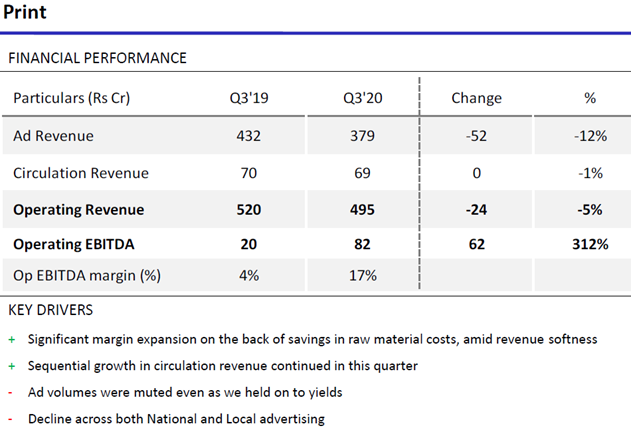

On the plus side, softer commodity rates and our continuous focus on cost control have given us good growth on operating profit and margins. We continue to be hopeful of recovery in ad spends as and when the broader economy revives.

No substantial decline in the newsprint cost expected in the future as it has already been decreasing since the last 3 quarters. The decline in newsprint cost is due to both reduction in prices and reduction in copies in circulation.

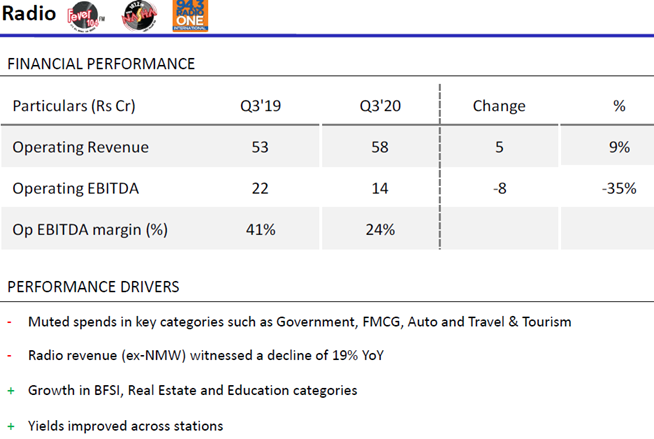

I think on the Radio business, we ourselves have been surprised for the last two quarters. If you see our results, or indeed the entire Radio sector results, there is quite a sharp slowdown which from the second quarter onwards is visible across. We are trying to take a lot of actions in kick-starting new stream of revenue, going much more hyperlocal and shoring up the revenues. But it’s very tough to say as we analyze, because we have, and indeed the entire industry has been caught a bit unaware on this thing. And we will see how it goes, but there are a lot of actions that we are trying to do in-house on that.

Profitability in comparison to FY18: Yes, look, I mean FY’18, you know, we used to have a growth coming on the top line, which was a big margin driver, so to say. Now with this six to eight quarters of perpetual revenue decline, there is a bit of a loss of operating leverage in the P&L, which is coming on to the margin. And if you also remember, that year, you know, we had just come out of a big cost project whereby we had improved the margins or the price margin realization had improved substantially. Newsprint prices at that point in time were benign. If my memory serves me right, we were in the zone of about 500 to 525 dollar a metric ton, where dollar was also not as sharply appreciated, which had happened last year. So, those things were contributing to the margin. Now, I really can’t comment on revenue. We have been hoping that the revenue will show some green shoots, though we see that in a few categories, but you know those are not sustainable enough for us to call victory on those respective categories. We are doing a lot of work, but I think for some time, we will be in this margin range of 19%, give or take.

Long term Strategy: So, let me give you a long-term strategy because this question has been debated, you know, on the quarterly calls even in the past. Two things that you are seeing right now is a lot of real estate which is sitting on the balance sheet. Most of this is our AFE business which is a separate line of business that we have been in for quite some time whereby all the real estate players who are looking for advertising but because of a certain liquidity condition cannot afford to do that. We basically take a risk and reward on the asset after doing a due diligence, and for part cash and part real estate, we kind of give them access to advertising. We believe and it has proved in the past that, of course, there might be some volatility here and there, but this is a good business because it gives us access to incremental advertisers who because of the liquidity situation might not be able to advertise and market their new projects, and we also get a strategic real estate play at what we would like to call a very favorable price, from a long-term perspective. The idea for most of this real estate is liquidation, and if you analyze our annual reports which will come out in three- three and a half months’ time, we are looking to monetize these assets and drive a decent IRR. The second point that you brought was about debt which is a classical treasury operation. Treasury is a very big profit centre. And though we don’t give the numbers because we are not publishing treasury as a separate category here, but treasury is driving a lot of positive EVA (economic value-add) on to a PAT level. So, whatever borrowing you are seeing either is for working capital or for CAPEX purposes where we try to access the cheapest source of borrowings, onshore or offshore, and not liquidating our liquid assets which are yielding us good returns in a risk-free debt capital market environment where we invest through various mutual funds, only on the debt products and never on the equity products.

From a group company perspective, nothing has changed. Monetization of the digital content because we see a lot of more advertising dollar going into the digital side, more growths are coming in there, so we wanted to have a larger play and up the game there. That’s the reason the Digicontent Limited (DCL) as a company was incorporated and subsequently got listed last year. Nothing has changed in this company. You know, if you look at the various sub-businesses on the digital platform that the company does, there is a growth of at least 20% in a segment and going up to as high as 30- 40%. But of course, the revenues are not substantial enough to cover off the print shortfall.

Now, what we did last year when we sold off the HMVL stake was because it was just getting too complicated having two parent companies, HMVL and HTML, and that is the reason it was done, and HMVL shareholders were compensated by cash at that point in time. But the digital company, the DCL, is definitely growing healthier, and it’s a double-digit growth which we also forecast going forward in the future year as far as the digital content businesses are concerned. Of course, there are some other areas whereby their revenues on the content that they produce for the print companies is concerned, which is the transfer pricing thing, and because the print revenues themselves are not growing, it is not helping, but all the pure play digital content businesses are growing in double digits and likely to grow even faster. If print does indeed pick up, that company will grow even more faster, but their pure play digital businesses are going very handsomely and very attractively at this point in time.

Well, from our perspective, at least, the margins have improved this quarter. So, that’s some as they call, the green shoots, we hope that the revenues now come back, which have been the big disappointment over the last many quarters now. While that starts happening, we will already see the impact of that coming through the margins.

On the cash side, of course, your company carries a reasonably healthy balance sheet and is perpetually looking out for more avenues to deploy the cash to generate sustainable returns for the shareholders. We hope the next quarter will be better than this quarter and there is an improvement which kicks back into the Radio business in which we have done some investment as well.

Disclaimer: Invested