Would greatly appreciate it if anyone could let me know the general flowthrough/reconciliation between disbursements and AUM for a typical NBFC.

My understanding is that disbursements are the principal loan amounts disbursed during any particular period; this then gets aggregated into your AUM, which generally tends to get reflected in the BS as financial receivables. Is this right? Does it go anywhere else? Now part of these loans are also generally securitised and taken off balance sheet. The money from this securitisation goes back into the BS as assets or some place else and then I’m assuming the securitised inflow is amortised as income during the said period of the loan?

Difference between AUM of any two years would be disbursement plus re/prepayments of loans. AUM at the end of the year = AUM at the beginning of the year plus disbursements during that year minus repayments or prepayments of loans. Every year you will disburse money and also some amount of loans will be paid back. The net figure will give you the AUM.

Hi, you should look at both, but not rely on either one. P/E is impacted by provisioning policies and leverage, and similarly P/B doesn’t accurately reflect leverage - and it is subject to regulatory shifts so P/B in different regulatory regimes will be different, doesn’t necessarily mean company is a value buy.For ex a bank with 100 of loan book, 100 of market cap and 10 in earnings and 20 in shareholder equity has P/E of 10 and P/B of 5 and leverage (equity to loan book) of 5x. If regulations require the bank to require only 2x of leverage it needs to have shareholder equity of 50, which would show P/B of 2 - this is not necessarily a value buy as there are now large dilution and growth concerns to be factored. Instead of P/B, you can think of Market Cap to Operating Assets (loan book + investment book) - captures leverage and you can apply portfolio quality measures to this ratio easily, by deducting them from operating assets for example or applying a hair cut based on provisioning / recovery trend.

Not sure if there’s any technical reason for ignoring P/B when dividends are paid out.

RoE is distorted in banks and NBFCs because of leverage, instead use RoA. NIM can also be overstated because of low leverage. Healthy level of leverage is desirable so low leverage is a sign of inefficient capital use.

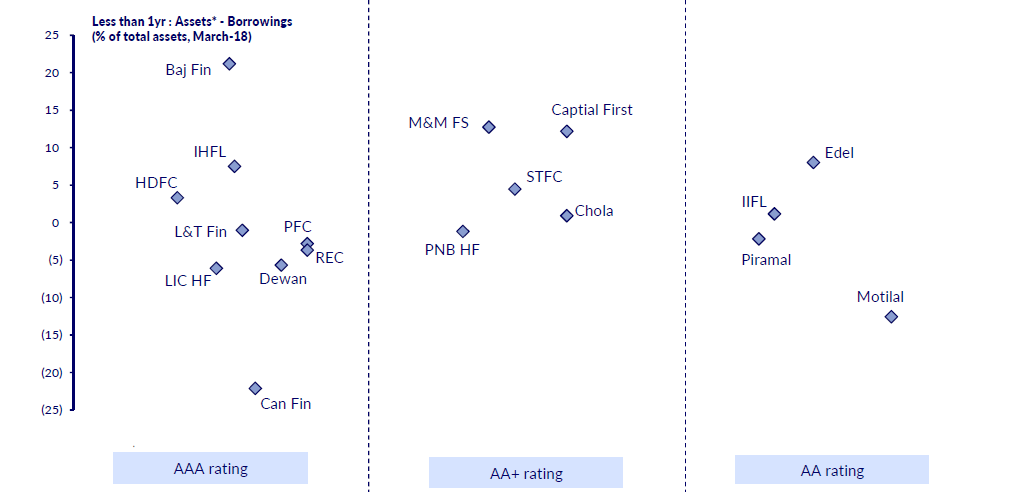

With the recent episode of Asset-Liability mismatch risk coming to the fore in the event of rising interest rate regime, please find below how different NBFC’s are stacked. Without sticking my neck out on any company specific recommendations, in my opinion sticking to 1) Market leaders 2) Higher-rated (albeit bad reputation for credit rating agencies) 3) lower ALM mismatch could be a prudent approach for risk-averse investors.

While various NBFC related threads are active today hope the below crux is beneficial for our forum members.

Hi, yes, you can think of it that way. It is similar to considering asset efficiency and RoCE for asset heavy manufacturing businesses.

You can actually derive the operating cash flow, so to speak, for a financial entity, but it is quite tricky considering the cash in cash out nature of the business - and one typically needs to know the repayment schedules of both their assets and liabilities for that, which are not disclosed in detail. One can study the accounting practices and cash flow statement to see how revenues are amortized to get a sense of this.

Hi,

Can anyone help me to understand how to find how much a bank or nbfc has distribute as a loan to corporate under debt restructuring schemes ? Since 25-30 percent of the restructured assets, in the event of a delayed economic recovery, can turn bad, which is the case as of now. So this is equally dangerous as NPA.

what is a good mix of liability side means? everyone seems to be quoting that the nbfc which are good at liability side will weather this crisis…pls share your thoughts on this

NBFCs raise money from various sources - Commercial Paper, NCDs, Bank borrowings, Company Deposits, Bank Credit lines etc. By the “good mix” of liability, the management might be saying that they are well diversified across different sources and can sustain any impact from a single source.

For instance, the current liquidity crunch in Commercial paper makes it difficult for some companies to roll over(issue new ones to pay off old ones) their papers. The companies relying heavily on Commercial paper will take a hit if the liquidity issue persists for long.

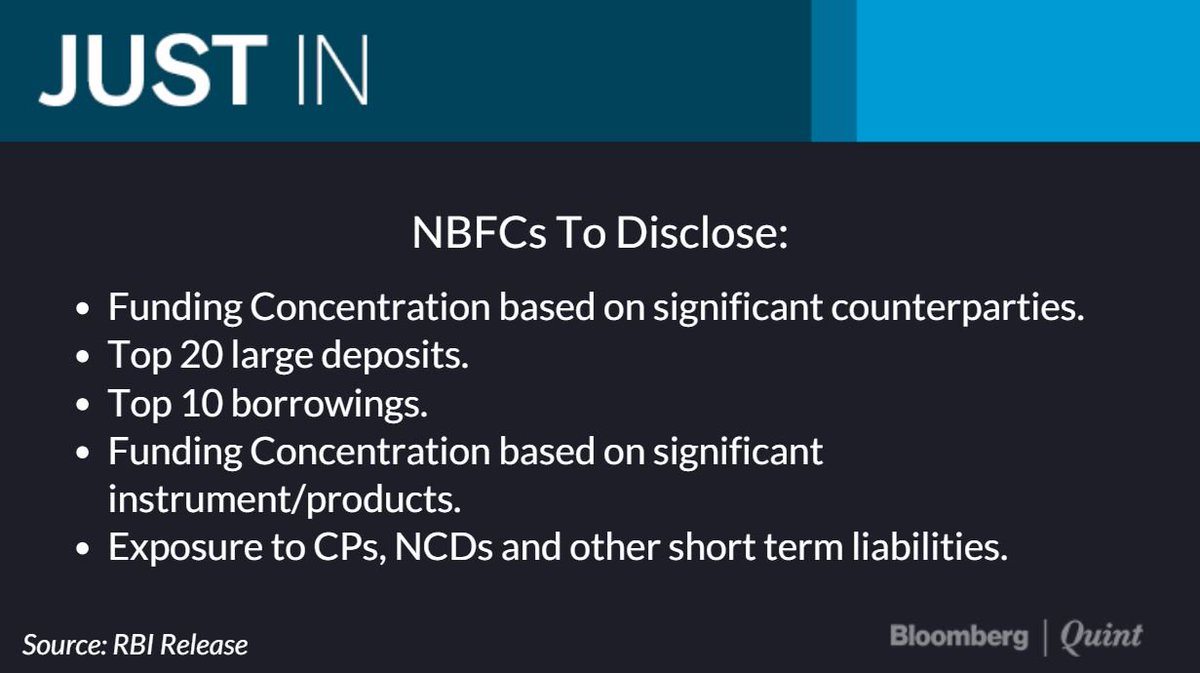

RBI releases draft norms on liquidity risk management for NBFCsThe banking regulator proposed that it will implement LCR through a glide path from April 1,2020 to April 1, 2024

—————————————————-

The LCR is calculated by dividing a bank’s high-quality liquid assets by its total net cash flows, over a 30-day stress period.

————————————————

The central bank has acknowledged the importance of NBFCs particularly in delivering credit to the last mile, including retail and micro, medium and small scale sectors.