Ujjivan fin services trades at a discount to Ujjivan SFB because as of now its a holding company and most holding cos attract holding company discount, till the time some form of value unlocking triggers are visible. Here, in case of Ujjivan twins, the merger of holding company with the bank can be an important trigger, more so as we have an example of something similar nearing its conclusion in case of the HDFC twins.

5 Likes

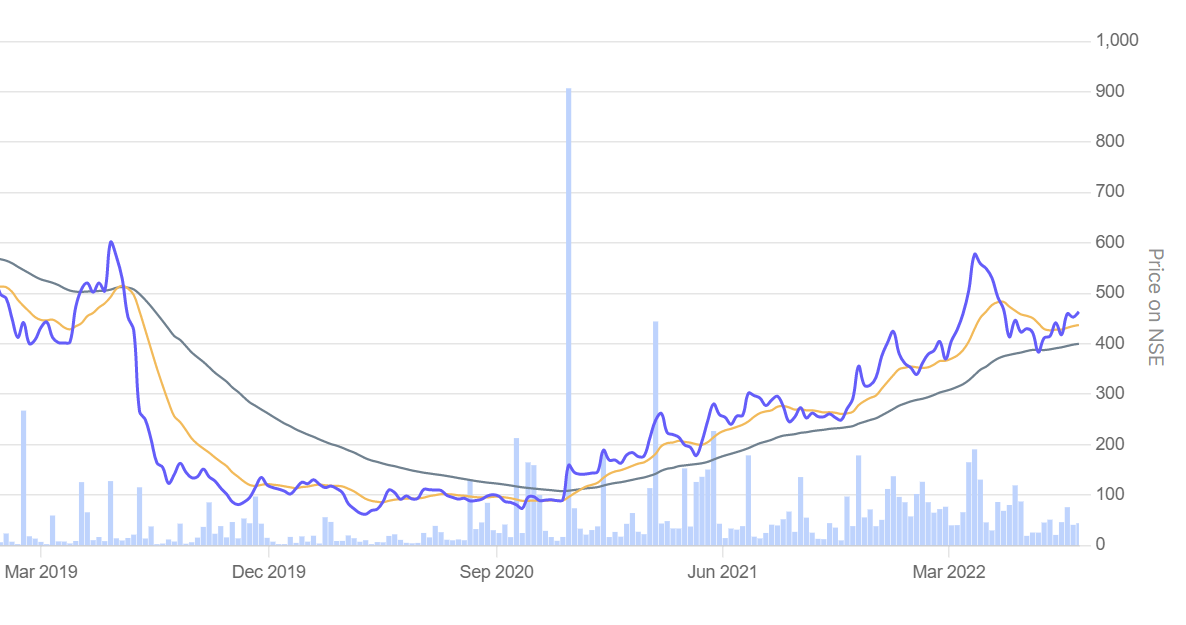

@hitesh2710 ji, would like to pick your brain on charts of Rushil Decors ![]()

does this qualify to be a cup and handle pattern (3-years graph). I’m a novice at this. still learning the basics… So am I just seeing things?

the fundamentals seem to be on the uptick… revenue doubling after 5 years of stagnation… highest ever Operating Profit with scope for increase in OPM…

and the entire manufactured wood industry seems to be on rising due to pressure from imports, increasing proportion of MDF as against Plywood and real estate revival. (Courtesy: FVP post on Rushil Decors)

every visit to this thread is a delight !!! and you seem to never get tired of answering the basic to the most intricate questions… can’t thank you enough ![]()

1 Like

For a cup and handle pattern, we need confirmation of a breakout. So you need to join the tops and stock price needs to breakout above that.

@Vikky9995 I don’t track IDFC first.

@novice2014 I dont track OCCL.

Lets not make this a generic thread on asking anything and everything without making any efffort at understanding ourselves. This is a forum to learn and if possible earn based on that, rather than spoonfeeding. So let’s keep it that way.

30 Likes

We have had a strong rally from the lows of June 22 at around 15200. Currently we are at near 17400 and the nifty has rallied close to 2200 points in a matter of 2 months. All throughout this rally there has been absolute disbelief about the sustenance of this rally and various people have called levels of 16800, 17100 etc as potential resistances, but markets seem to have a mind of their own. We seem to be in an expanding triangular structure in nifty and the overhead resistance could be possible at around 17700-800, a level I would watch out for any signs of exhaustion of this rally. The aforesaid expanding triangle is marked on the attached nifty chart.

I have always tried to refrain from predicting the market movements in advance because the one thing I have observed is that its difficult to get these predictions right all the time. I might draw a few simple trendlines and try to see how markets behave at crucial points which I see on these simple charts. But its better and more rewarding to focus on companies which enjoy strong tailwinds and strong charts , or where markets give a thumbs up to even weak results, indicating good times to come ahead.

Some of the sectors which seem to be showing strong charts till now have been defence, autos, capital goods, power and energy, capex themes, etc. One sector where I see market giving thumbs up to what are comparatively weak quarterly numbers is the FMCG sector. But here, with prices of input materials like palm oils, dasda, other edible oils, materials used for soaps, shampoos etc cooling off, there is promise of better times to come. I would not like to take specific names, but as a sector one can do some more detailed work and try to find anything interesting. Or try to find ancillary play to these names.

Individual companies in the portfolio like Fluorochem, Usha Martin, HBL power, and some trading bets in auto anc space, auto space, hotel space etc have been showing strength/resilience. There are many other stocks and sectors which seem to be on the verge of completing their long corrections. I will post any sectoral stocks once I see clear actionable patterns.

63 Likes

Hi …Dr Hitesh…

Ur views on this wrt Domestic branded generic players. To me it sounds like catastrophic.

2 Likes

This is something I have been reading since a long time… If possible do check the date of publication. And read the details. I do not think it means much overall to the domestic pharma space.

Even govt cannot afford to kill the domestic pharma sector, which is a big tax and job generating sector…

9 Likes

They can only issue guidelines but can never enforce it. There is virtually no mechanism to stop it and more over we know how corrupt the system is. These guidelines are issued only for good optics.

1 Like

Hitesh Bhai. I have 2 questions -

- As a investor interested in growth, how much importance do you place for a stock which do well both in terms of top line and profits yoy, but de-grow qoq on both sales and profit.

For ex. If we see the results of Gujarat Flourochem or Schaeffler, it has done well both yoy as well as last sequential quarter, whereas company like HBL power did well over last year quarter but de-grew compared to previous quarter. I know it’s too much to expect greater performance and compare it with last 3 months. So how much of this does matter for you?

- Since you are fairly concentrated investor betting big on few stocks, how do you deal with adverse situations, which can’t be foreseen. For example, recent income tax raids in the case of Krsnaa diagnostic and insider trading by director in one of innerwear company (can’t recollect name). If we see, in the long run all these doesn’t matter much, like in the case of Divis where there were some IT search/raids and then some insider trading etc., but the stock went up several x.

However, in the short term, the news is enough for the stock to fall by 20%. So with limited capital, being concentrated, how should one manage these kind of risks which is unforeseen.

Once again thank you so much

5 Likes

While looking at companies quarterly performance, we have to know that there are certain companies involved in certain sectors where particular quarters are heavy and some are not so heavy. In companies like HBL where an element of defence orders is there and govt projects like railways are there, quarterly results can be often lumpy, so its better to look at them on a yearly basis. There are some sectors like construction, defence, etc where last quarter is often best quarter. Another example is of Kaveri seeds where q1 is the most important quarter.

- In a concentrated portfolio, there is not much space for errors and if an error is detected, it has to be dealt with as early as possible and in a decisive manner. Krishna and Divis are different business models. I usually am not too aggressive with companies with high percentage of revenues from govt side. The so called B2G businesses. Because according to me, these depend a lot on currying favours from those in office and hence orders may not be sticky. Plus payment may remain pending for long periods of time when it has to be collected from govt.

Even after all precautions, stocks often fall because of unexpected reasons and in these situations, the rough has to be taken with the smooth and it often makes sense to exit at earliest sign of trouble.

26 Likes

Good evening Hitesh sir,

My question is regarding your techno-funda approach to investing.

- I wanted to know if all your picks in your pf have both momentum on charts and fundas always going for them?

- Do you keep a trailing SL, if not how do you deal with exits?

For example in Gfluoro, I pulled out my position at 2800 or so. How do you sense that it would pick up strength again?

Had made a similar mistake in FCL which corrected after I sold but regained and then some, leading me to miss out on heavy gains. Is there a systematic approach to this?

Thank you so much sir.

5 Likes

Hitesh sir, you have multiple trading bets in the hotel sector. I have couple of queries related to it:

1/ How long is your time horizon for these bets (2-3-6-12 months)?

2/ Most of these stocks are already up 50%+ so far in 2022, so how do you see the valuations of these stocks (are these still undervalued or now fairly valued)? how much more upside are you expecting in hotel stocks from here on as per technicals?

Thanks much in advance

Yesterday attended a twitter seminar having Sajal sir. He said this is not practical because

- Unbranded generics are cheap for a reason. u wont step into the factories of them bcz they are in bad shape. There is nothing like USFDA in India to control quality.

- Medical professionals also dont like them because if it takes 2 pills and 2 days hospital bed for a patient to recover with branded ones then with unbranded generics of low price it takes 20 pills and 7 days.

- Absolute profit earned by selling one pill of unbranded generic is much lower than branded one. So to make same profit the pharmacist has to sell more pills.

Hence it’s not viable and sajal sir told this type of things makes no sense for neither the doctors, nor the patients nor the pharmacist. Only government gets some credit for bringing down medicine price but at what cost? india is already the cheapest producer of drugs. How do u make some thing more cheaper when it’s already cheapest in the world.

14 Likes

IMHO, When it comes to winning elections, politicians are hardly bothered about logic or long term benefits.

Government has introduced fee reduction in 50% seats in private medical colleges without any thought about how to compensate them.

Many private medical colleges will struggle for survival.

Regards

1 Like

Hi hitesh bhai, you recommended shaeffler India for a technofunda bet about a year ago. The stock did fantastically performed and reached a peak of 2000 then it sold of to 1800. some time ago in March 2022 I asked for your opinion on the stock as it already had significant run up from your recommended levels. Then you replied that you exited counter at 1800 and don’t expect any major move. But to our surprise the stock went up another 50%.

My question is how can we avoid missing such moves even when we have identified the counters for technofunda bets.it happened with me alot in recent times as I was looking for opportunities to go in using technofunda method. I waited for laurus labs to correct till 450 levels to buy but when it did happened i was unable to pull the trigger. Happened in sbi when it was 440 and happened with icici bank at 680 and in many more counters. I wanted to buy stocks for 10 to 20 percent up move within 1 to 2 months. Most of the times the stock making the move but I’m unable to hold the position for the entire move. I’m able to capture only 2 to 3 percent or exiting the loss. Could you suggest any psychological or anyother changes in my approach? Or in general the desire to stop booking the small profits and hold for larger gains.

Thanks in advance

2 Likes

@Vikky9995 There’s wisdom in the market cliche “Only two people can buy at the bottom and sell at the top – one is God and the other is a liar.” This means even the smartest guys in the room can’t sell at the top or buy at the bottom, every single time. They may get it right a lot of times but not always. For example, Hitesh bhai was able to exit Laurus around 650 levels last year, when practically everybody was Gung-ho about the stock all over social media.

That being said, the practical way of dealing with this problem is to build conviction in companies by working hard on them. This is to be followed by buying the stock at opportune times when the whole market is in a pessimistic mood, like what happened a few weeks back when almost everybody and their dog thought the sky was falling due to problems caused by the Russia/Ukraine war, inflation, Fed rising interest rates, etc. At such times, provided you have pre-built enough conviction in a company + you don’t foresee structural problems in the company’s business model in the near term + the stock has fallen to reasonable levels from where it can be expected to deliver decent returns, then one can buy in a staggered manner on the way down, without worrying too much about interim paper losses.

Technically, one can try to buy near support levels but even those levels don’t hold too well during free falls and one just has to bear the temporary pain that comes with drawdowns.

So if I had strong conviction in a given company’s business and it had good near to medium term earnings visibility and it’s price had fallen say from 1000 to 800 and I had pre-decided to buy at 700, I wouldn’t wait for the stock to reach 700. I would instead start buying in installments at 800, then at 750, 700 and so on. That way if the stock turns around from 710 and starts goes up towards 1000 and beyond, I would have no regret because I was able to catch at least some part of the move.

Another thing to note is that stocks that are in strong momentum + good near term earnings visibility usually don’t correct more than 20-25% from the top. Again like everything else in the market, nothing is infallible. The one rule of the market is that it never follows rules. ![]()

36 Likes

-

All my picks do have momentum on charts and I try to make sure that there is fundamental momentum or a promise of fundamental momentum. The latter because many a times charts guide you to entry points in stocks when not much is visible on the fundamental front. Its only after some time that the actual fundamental triggers start to play out. So if I have any position where at the point of entry I cannot figure out any fundamental triggers, I keep myself clued in to the developments happening at company/sector level.

-

As a general rule I try to follow broad ranges as my stop loss rather than absolute numbers. But after having read Stan Weinstein, and then looking at the charts after having plotted 30 week moving avg, I think a simple way to follow stop loss could be to watch out for a decisive breach of 30 WMA in stocks which are strongly trending. For me also its a work in progress, but hope this approach provides some kind of systemic framework for you.

22 Likes

Hotels and other unlock themes are usually the flavour of the season types of bets. These type of situations are easy to decipher for markets and hence most of the juice is out within some time, unless there is prolonged disbelief in the theme. The bets in hotel sector for me was one in which it took longer than expected to work out and not to the extent I had expected to work out. Part of the problem was that I was much earlier than what was prudent in these bets and hence had to watch the stocks go down and then now watch them go up.

I had put up the chart of Lemontree hotels where I had explained that 70-72 was a stiff resistance and now that is crossed, I think technically target was close to 84-85 and beyond that all time high around 90 and above.

But I cannot get my head around the valuations of these hotel stocks, so plan is to exit on visibility of froth, or when technical targets are achieved. In these kind of names, I find it futile to try to value them as its beyond my expertise to value them. But broadly if I catch an earnings upcycle, I would try to ride it out till visibility is clear. In case of hotels, I keep tabs on how bookings are faring, by keeping in touch with a friend who is a travel agent. The upcoming holiday season in near term, plus Diwali etc going ahead, should bode well for the hotel sector.

Only thing to watch out for these thematic bets is that many a times stocks tend to top out much before trouble is visible in actual fundamentals of the companies/sector in question.

14 Likes

I think what the pharma expert Sajal sir said is true. It doesn’t make sense for any parties involved in the whole pharma value chain and hence not expected to materialise. As said before I have read these diktats since a long time. And we need to check the date of publication of these stuff and read in details who it is applicable to.

Having said that, I have felt since a long time that as of now pharma space is something that does not excite me too much. A lot of these companeis especially the US facing companies (where the actual big bucks can be made) are facing pricing heat. Domestic pharma market is highly fragmented it has its own set of problems. Plus finding a company with exclusive domestic presence is difficult. Most pharma companies have a business model wherein part of business comes from exports.

As seen in the past, bulk drugs, had a stellar run wherein stocks gave multibagger returns. But as of now that too seems to be a thing of the past, and while there can be a winner here or there within the sector, base rate of finding winners is low. So I prefer to focus elsewhere.

For those interested in knowing more about the pharma space, @gurjeev has put up a write up on Medicamen biotech on Shivalik rasayan thread . There he has tried to put up details of some terms people find difficult to understand while looking at pharma space. I have my doubts about my ability to project numbers mentioned in the report, but just as a report to understand a pharma company, one should read it.

19 Likes

I think @barathmukhi has answered the query in a very good and detailed way.

Coming to specific company schaeffler, 1800 was a technical target and once that was achieved, with the available information at that time it seemed fairly valued. Plus I had a couple of other ideas like Usha Martin etc which were more exciting to me. Hence the decision to exit. And if I see now (although one might consider looking at it in hindsight) I find that the stock price consolidated in and around 1800 for nearly 10 weeks before moving up again.

If you are following the techno funda approach and keep looking at charts, you will be presented with a lot of new opportunities off and on and hence the idea is to evaluate the new opportunities and try to compare them with the stocks you hold. And then its a toss up on where to be present. One approach I think could be useful is to book partial profits and let rest of the position run to maximise the gains. That is only a thought process currently and not put in action. The drawback I see with this approach is that I will land up with a lot more names in my portfolio than what I am comfortable with. But even with this drawback it seems this method has its benefits, but getting a mindset to adopt this strategy will take some time and a lot of fine tuning, and I am not too sure when or if that will happen. If someone can find it useful and implementable, then its worth doing.

21 Likes

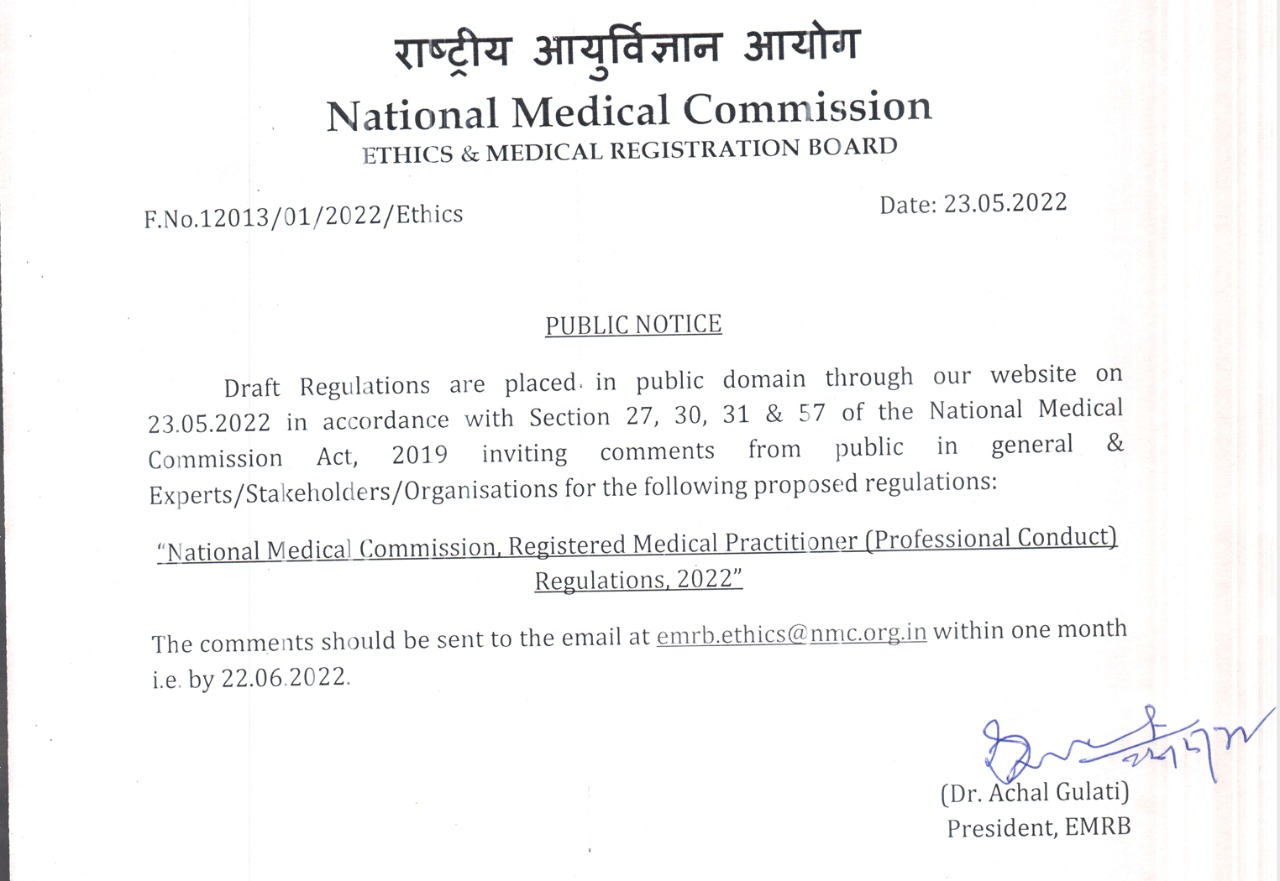

National Medical Commission published this NMC RMP Regulations 2022 on 23-05-2022.

These were draft guideliness and they were inviting comments on the same. These guidelines need to be passed and published on official gazette for coming into effect. Just like you pointed out, I too am not sure if this will ever materialize or when it will happen. I posted the same because that regulations caused some element of uncertainty and needed attention.

6 Likes