The main purpose of the Pat Dorsey book you mentioned is to learn to analyse different companies. Especially what to look for while analysing a particular sectoral company. If you have learnt that it teaches us to use morningstar data, then you have missed the main learning and grasped at peripheral issues. And with screener providing most things needed for fundamental analysis, and most of them even free, I don’t know why we want to go to any other sites like morningstar.

@fundoo I have mentioned about bullishness in paper sector stocks. That view still remains. No change.

@nikhil090 I had already written about my views on small private sector banks. Results of these banks are playing out as expected. I think the stock price movements are also reflective of market bullishness in general on these names. Many of these small banks are undervalued and that is something that can be exploited. But I am not too sure about holding them for the very long term as yet.

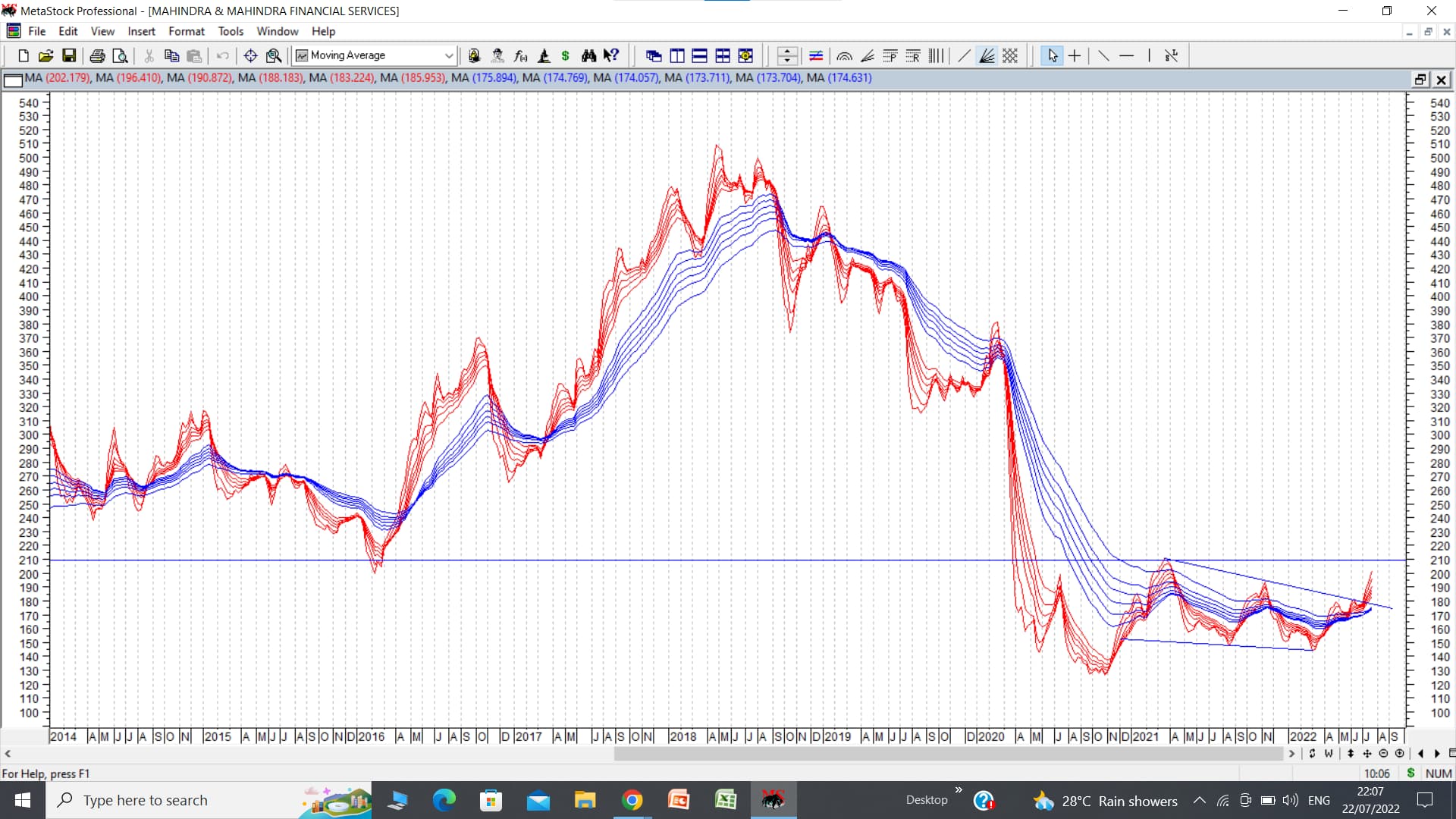

Hello sir, are you still tracking M&M Finance? You had mentioned that this is a turnaround company post getting badly affected by COVID. How do you see it now?

Most of these financials including banks and NBFCs seem to be coming out of the woods. Basic premise currently has been a lot of write backs of provisions made earlier. Next thing to watch out for would be profitable growth in loan book. I think quarterly results of MM Fin should provide idea on how things are progressing on fundamental front. You can listen in to q4 fy 22 concall to get a better idea.

On charts there seems to be a move outside an atypical consolidation pattern. Only problem I see here is a lot of resistances on the way up at various levels.

The view remains same for most financials and NBFCs. So anyone interested in these companies can do their digging and take a call.

You have on most of the occasions said that once the sector fancy is over, its better to look at stocks in a different sector which does show interest, than look at same sector.

If we take recent past, specialty chemicals had a great run. stocks which were 1-2 times sales went upto 10 times. Then the pharma sector. Now if we see again, some picks of chemicals sector viz., Gujarat Fluorochem, SRF, Navin Flourine seem to be coming back to fancy on back of good to solid results. How cautious you are in betting these kind of outliers which belong to sector which had its good time.

Most chemical sector stocks which were running on narratives (of being speciality players ) are now down and out. A lot of these largely commodity kind or quasi commodity kind of companies were touted to be weather proof and immune to vagaries of demand and impact of raw material prices. Problem is not with the business or promoters per se, but the kind of valuations given to these companies. Commodity companies which attain speciality companies’ valuations would often find it difficult to live up to market expectations and hence there will be meltdown. This happens with most sectors at some point of time during their market fancies. But there will be exceptions to these sectoral meltdowns in most instances. And there will be reasons for this phenomenon.

The kind of companies that have remained aloof from the meltdown in the chemical sector are the ones which I think are the real speciality companies with a sort of moat (at this point of time, mind you. Things can change over time here too) In such companies, the narratives are matching the numbers reported by the companies. And that’s what seperates boys from men. (again at this point of time) How long this party lasts is anybody’s guess, but as long as numbers keep chugging along, valuations will sustain and even probably grow in terms of PE being accorded.

Navin reported decent numbers if compared to a lot of other companies from similar space. Personally I feel at cmp, valuations are stretched inspite of good numbers. But who am I to question market wisdom? Maybe there is a clear road map drawn for near 20-25% growth for next 5-10 years. (I don’t track it so not much idea, but price action does indicate market confidence in the company) Against that, today I saw numbers from a smallish (in terms of sales not valuations or market cap) company named Tatva Chintan. Revenue drop, profit drop, margin being affected, everything going in the wrong directioin. Stock price has corrected from highs of near 3000 to current levels of 2370. On charts there was a clear double bottom breakdown below 2320 with a potential downside of nearly 700 rupees. But till now price has managed to hang on above and around 2300 levels. One of the reasons could be high promoter holding of 79%. Or could be some other reason. These are the kind of situations I keep in my study list to see how price action plays out to what I feel are poor results. You keep observing these things and try to keep learning how markets work.

I do not track Navin closely so not much idea about whether valuations are justified or not. However I do own and track Guj Fluoro and looking at global situation in fluoro polymers, there still seems to be strong tailwinds for this particular sector and the company itself. But the proof of the pudding will lie in the eating, and hence I would keenly watch the quarterly results due to be out and management commentary. As of now, the stock price seems to be showing strength and resilience.

My idea in riding this company is to enjoy the music till it lasts and keep on lookout for any signs or newsflows contrary to my investment thesis.

To be fair, management has guided back in Q4 itself that Q1 and Q2 is going to be subdued for SDA segment which was approx 40% of their FY22 topline. They did advise this is a temporary pain due to semiconductor shortage as auto emission control is a major application for SDAs. And this segment should be back firing in Q3 and Q4 so much that it should cover for the subdued Q1 and Q2. So, I think we should hear the management out. If the commentary changes, this can be taken as heading in the wrong direction.

But if by Q3 growth is expected to be back, the long term business would still be intact. In fact, backlash in the short term due to these and potentially similar Q2 numbers may provide entry points.

Disc: Not invested but on watchlist to invest at reasonable valuations.

Guj Fluorochem results have been better than I expected. And in the concall management commentary comes across very strong indicating strong levers for growth. It comes across as an example of a company which can deploy huge doses of capital at incrementally higher rates of returns.

Schaeffler results have been very good and it seems to be well on the growth path. But I do not track it too closely now that I have exited. Yet to listen to concall.

(@hitesh2710)

Hitesh Bhai - Few Q’s for which I would like to hear your views:

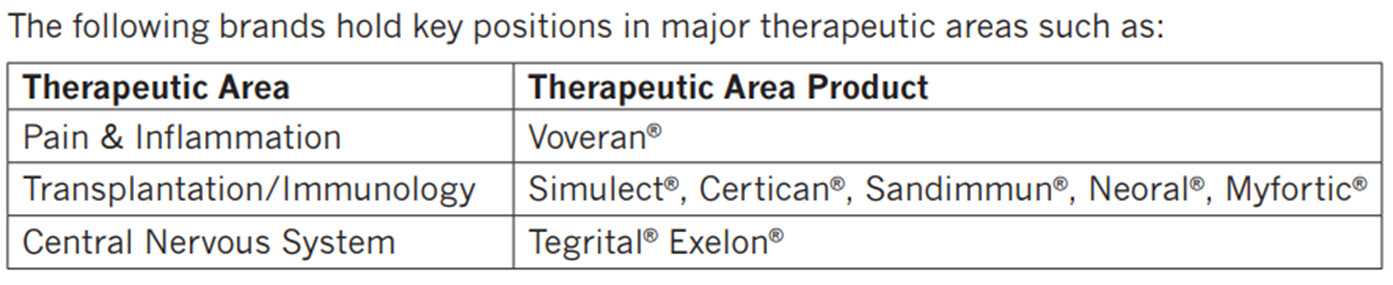

How good is the product portfolio of Novartis India Ltd?

What kind of market opportunity do these drugs cater to? Business focus is on the four key disease areas- Mature Neurology, Transplant, Mature Oncology, and Bone & Pain.

What will be the incentive for a doctor to prescribe these names compared to cheaper and branded alternatives (1mg shows various reputed names as cheaper alternatives)?

Please share your views on how to analyze a generic pharma company product pipeline strength with emerging market exposure?

Everyone posts in their quarterly and yearly reports we have filed these many ANDAs (F2F, DMF etcc ) and all but as a retail investor what is that one parameter ( I think it can’t be one but many ) that can give some insights about the opportunity size?

Your views on this buzz word in Pharma CDMO.

As per Pharma experts (dedicated PMS into pharma) they don’t favor companies with US exposure due to pricing erosion, but high margins are achieved beyond a level only by going to emerging markets. Please share your thoughts

Gland - In the concall Mr. Sadu said impact is due to syringe supply constraints, but in Reddys latest concall, they said there is no such issue experienced by them. (It is evident there is huge demand for syringes all over the world for vaccines ) How to understand these kind of statements (in terms of management honesty / integrity ) ?

Hitesh Bhai wanted to know your views on Deepak Fertilizers if you are tracking and also this sector. Strong set of numbers in Q1 FY23.

The Top line has sequentially grown by 50% and YOY for the quarter by 59%. Margins are stable and the growth in the bottomline has been strong. The stock now trades at a PE of 8.

@hitesh2710 bhai since you own/track Usha Martin, did you happen to analyse DP Wire as competitor? They are also in similar products line. Pls share fundamental insight if you have done, Also pls share technical view DP wire. Thanks

Hi Hitesh Sir, what is your view on sona blw .Q1 FY23 results are somewhat weak due to slow down of economy in Europe and US despite all time high revenue growth .currently it has order book of 10X of FY22 sales and management also seems good .

As of now I do not see any bullish chart formations in PEL. The technical set up also is not too encouraging, the stock price being well below 200 dema in the midst of a strong rally in overall markets…

@Surender I do not track Novartis. Its leading products are well known but in pharma business, which is highly fragmented in India, well known brand names does not provide too much of an edge. Another company can come up with a copy cat product at much reduced prices and in India where a large part of patient population is non affording, this fact assumes a lot of significance. You can check prices of tegrital and mazetol both of which contain same molecule. Tegrital is the original molecule but because of very big price difference between it and other clones, doctors would prefer to prescribe cheaper alternatives to provide lower cost drugs to patients.

@Rafi_Syed How to analyse a pharma company is something beyond the scope of this thread. You will have to read up annual reports of companies which give out detailed information. Or else go through relevant pharma threads on VP. I recall @ankitgupta gave a presentation on one of our Goa VP conferences on pharma sector. You can try to locate his presentation and go through it.

@lakshmikanth1 Sona BLW IPO came out during the IPO bull run which was prevalent few quarters back. A look at screener tells me that its PE is near 100 and June quarter results have been affected by margin pressure. Now companies quoting at near 100 PE are not allowed any mistakes. They can get away with some fancy explanations for a quarter or two but if even after that period results don’t match expectations, there can be a carnage in stock price. Often this kind of carnage goes from over optimism to over pessimism. If that happens, there can be an opportunity. As of now I feel I have better options to look at.

We have to realise that companies whose IPOs come out during IPO fancy periods often are over priced and over hyped. This is because there is a whole army of financial mercenaries working to sell the IPO at highly inflated prices. And managements/promoters often are working in collusion with these guys to give a rosy picture. Even the media, including social media, print and digital and TV media chips in intentionally or unintentionally to magnify this rosy picture. We have to remember that there are a lot of incentives at stake which you and me as retail investors are not aware of. So better to rely on wisdom of experienced guys like Lynch, who said that the full form of IPO should be understood as "Its probably overpriced. "

Regarding order book being 10 times FY 22 sales, we have all seen such stuff many times in the past. In the infra/real estate frenzy of 2006-2008, the biggest buzzwords were land bank and order book. ( I remember there was a term called book to bill ratio or something similar) A lot of companies in infra space were peddled based on this logic. And look at where those companies are… I guess a lot of them like Punj Lloyd and GVK and Gammon group etc have become penny stocks or have been delisted.

These kind of cycles keep repeating and keeps trapping gullible investors. That’s not to say Sona BLW is similar kind of company, but we have to be very careful when we invest in companies based only on their order book, or expanded capacities and so on and so forth.

Hi hitesh sir, could you share your views on laurus labs? This quarter growth returned in revenues and company posted good results. If possible can you analyse the chart? It will be a great help to me. Thanks in advance.

I want to know your thoughts on stock selection and portfolio building.

How do you select a stock? e.g. do you select the sector first based on tailwinds and identify basket of companies in that sector? If yes, how do you identify the sector before it start appearing in the news like now auto anc is in the news? Once sector is identified, do you select basket of stocks(2-3)

Portfolio building - do you have core and momentum portfolios or you follow only momentum portfolio? What are your thoughts on % allocation for core and satellite/momentum portfolio? Also in general, how much max one should allocate to a sector and stock considering person is not concentrated investor

How does technical play a role in your stock selection? Do you use them to identify basket of stocks once sector is identified?

What are your thoughts on auto anc and power sector in term of tailwinds? How do we know that we are not late into the party and have to pay the bill.

Thank you for your guidance to the entire investor community.