@hitesh2710 , Texmaco and Titagarh Wagons. They both have garnered orders worth 4-5x their annual revenues. Trading at near book values. Mcap less than annual turnover. Turn of the cycle ? Sounds too good to be true… please guide on wagon manufacturers… and on rail expansion play in general…

hitesh sir ,

I would like to ask you about BPCL (BHARAT PETROLEUM) …As it gives healthy dividend is it safe for long term ? If you tracking BPCL please share your view

thanks

NPA is high in those banks sir

For NPA in these smaller banks, the trend is more important than the actual NPA numbers. And since past 4 quarters, NPA have been consistently trending down. We need to see how these pan out going forward.

@praveens I dont track these railway stocks.

@hitusohi1 I dont track BPCL.

7 Likes

sir , isnt hdfc bank safer with more clarity and good management and now at decent valuation … than such smaller banks with huge npa .

2 Likes

Sir

Are you tracking rail related logistics players like allcargo or gateway distriparks and express logistics like tci express or gati

hitesh bhai, i spoke to an RBL employee today, he is my customer so i enquired about the situation in the bank, he told me that middle level management is leaving the bank, and his boss told him to get out of the bank asap. he refused to divulge any further details, but at the outset all is not so well in that particular bank.

5 Likes

Hello any view on auto sector, do you see signs of reversals based earnings call commentry?

2 Likes

Hi @hitesh2710 Sir !

Is this the right time to enter small / mid cap scrips in this volatile time…

Sir, what’s your view on these small / mid cap scrips for long term :

KPR Mills, Schaeffler India, Meghmani Finechem & Laurus Labs.

I am really confused to enter these stocks at this point of time…

HITESH SIR WHAT ARE YOUR VIEWS ON EASY TRIP PLANNERS AND DIXON? ARE YOU TRACKING THIS COMPANIES? I have read somewhere that technology related companies are easily replaced, said by Mr. Warren Buffet. If this is true then easy my trip is not good for long term right? But if we look into Travel Booking agencies then this is the only company which is profitable and also have 70% GPM. ROCE and ROE is also very high. Good financials. Is this company worth looking?

Hi Hitesh bhai, hope you’re doing well!

Would like your thoughts on a few things:

- What do you think about the API and specialty chemical space from a 3-5 year perspective at CMP given that these stocks are out of market fancy and individual stocks have also seem 40-50% correction from the peak.

E.g., Aarti Drugs is a well-run company, is doing significant capex, and is available at reasonable valuations; I think the same is true for Oriental Aromatics

Would also like your thoughts on individual stocks in case you’re tracking Aarti Drugs/Gufic Bio/Astec Life/Divi’s Labs/Oriental Aromatics/Deepak Nitrite

-

How do you think about the BFSI space and players such as Kotak Bank, ICICI Lombard, HDFC Life, HDFC AMC in an inflationary environment with quantitative tightening?

Do these have the potential to deliver 15-17% returns from a 5 year perspective at CMP? -

Would also like your thoughts on the hospital space and if you find companies such as Narayana Hrudayalaya or Healthcare Global to be interesting?

Thanks in advance for your time ![]()

The auto sector has been out of favour since well before Covid. Most of the stocks were in a downtrend and not showing any significant signs of upcoming rallies, based on chart formations. But with Covid onset, most of these stocks underwent significant cuts and a lot of these stocks have formed significant bottoms. The problem with a lot of these is that there can be significant consolidations in a lot of these charts before real take off happens. M&M chart looks good though in short term it may see some consolidation. It has been one of the few auto companies to go well above its life time highs. Other stocks which seem interesting are TVS Motors and Eicher Motors.

Some auto ancillaries also look good. But as of now I cannot find any screaming buys based on techno funda appoach, neither have I any position in the sector. But on charts the worst seems to be over for many stocks.

I have not listened to individual companies commentary but the sense I get from listening to financial companies concall, the impression is that the CV segment seems to be coming out of the woods.

@aatish I dont track dixon or easy trip planners.

@Shakti_Srivastava Laurus seems to be on a strong wicket based on the latest concall. You may listen in and decide. Schaeffler has been very strong in recent times, so can be a good momentum play on declines. Rest I do not follow.

6 Likes

The API players and the chemical/speciality chem players have in the recent past been huge wealth creators and now most of them seem to have broken down on the charts. But as seen in past many posts, people keep getting obsessed with past market winners. ![]() While in fact the prudent thing to do is to look at other sectors where either the charts are showing strength across the board, or individual companies are showing fundamental momentum and turnarounds , OR preferably a combination of the two.

While in fact the prudent thing to do is to look at other sectors where either the charts are showing strength across the board, or individual companies are showing fundamental momentum and turnarounds , OR preferably a combination of the two.

The usual story is that a particular sector or sectors start showing decent results, (though not head turners) in early phase of a market fancy. But there are still some concerns on some or the other front. So while the smart money is getting in early, momentum guys keep waiting on the sidelines for price momentum to begin. It takes a couple of quarters or more of good results and good commentary for the company/sector to start attracting generalised market interest. Till that time all positives are ignored. Once the crowd and institutions start getting in gradually, price momentum starts building up. And all this while results continue to surprise positively or beat estimates. Then there is the stage where these names start making it to the headlines on news channels/social media/investment forums and all this while, the stock price continues to rise. The dumb money still has doubts about the sector and stays away. Once the frenzy is built up, there are wild price moves in the final blowout phase, and that’s when the dumb money starts getting in at the fag end of the rally. These guys are the most gullible investors who swallow everything that is being thrown at them in terms of positive news/rumours. And during this time, when there are huge volumes with price moves, the smart money starts exiting and this is the phase that is labelled as distribution. A lot of media stories appear (some planted, some fabricated, some part truths) establishing the invincibility of the sector. And a lot of capex news start making it to the headlines and grab eyeballs. There is a lot of extrapolation of numbers based on capex estimates. And then price cracks start appearing and start giving early stage warnings. But those who missed on the way up are obsessed with the companies on the way down and try to find reasons to buy and all the time charts continue to show price weakness. And then bad news/bad results start appearing and still some folks try to find value in a previous growth sector.

And all this while another sector is already getting ready to shine, while the dumb money is obsessed with the previous winners. And the cycle repeats itself.

Coming to specifics, all these API players listed have been big winners in past couple of years, but they have had their day in the sun. Base case of making big money (key word is big money) from these names is low. There will be the odd one that will make it big, but its like looking for a needle in a haystack.

Most of the companies going in for capex is usually a doomsday call for a sector. When every company wants to increase capacity, its usually the time of peak sales and peak margins and peak profits. Then shit starts hitting the fan and a lot of people end up getting muck on their faces. (there are those rare instances when capex leads to big winners, but there one has to look on a one on one basis rather than a sectoral call. )

Coming to financials, I have made my views clear in previous posts, so no use repeating them. Insurance is a sector I do not know how to value so I tend to avoid, unless I see strong chart patterns.

Hospital sector stocks and the valuations they are being given in the name of long runway for growth is something I cannot understand. NH and HCG are interesting but I find it difficult to value these companies and I cannot find consistency in earnings which I want in my medium to long term bets. NH chart has been a strong one, so one may dig deeper, but I am staying away.

54 Likes

I feel, in Indian market, significant part of the time, Market leaders continue to get market share and related profit pool . That’s why there is a scarcity premium. Sector rotations may happen but sectoral leaders remain more or less same, eg IT, Banking,Paints, NBFC,

3 Likes

Hi Hitesh sir

Please advise on below points

-

Your view on cement sector for next 3 yrs in view on real estate sector will shine

-

Your view on recent ultra tech capacity expansion… how that will pan out for other cement companies

Hiteshji,

Any view on MAS financial and Armaan?

Hi Hitesh Ji,

Any view of IT sector now particulary HCL Tech and Tech Mahindra considering the entire sector is bitten down much and valuation also seems reasonable now.

It would be great if you can share your views…

Thanks

Vinay

1 Like

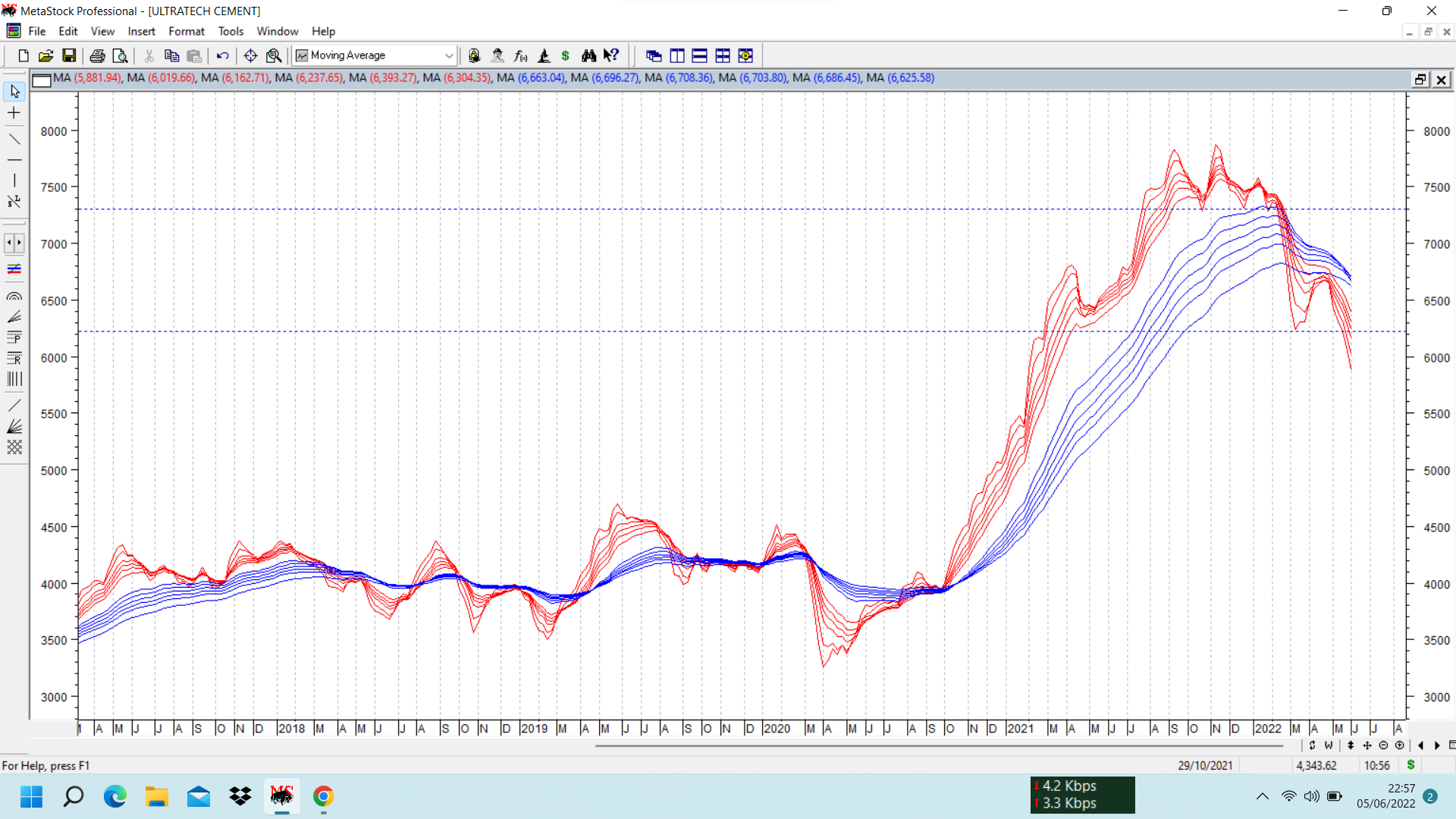

I don’t track cement sector too closely but the charts of most cement companies look weak. Even a cursory look at ultratech chart on screener shows a clear breakdown from a head and shoulders pattern below 6000 and from current 5600 odd levels, downside still seems more.

Even other cement stocks like ramco cement, dalmia cement etc look weak.

So based on these charts I would not look at cement stocks at current levels and instead wait to see how this plays out and where these stocks bottom out.

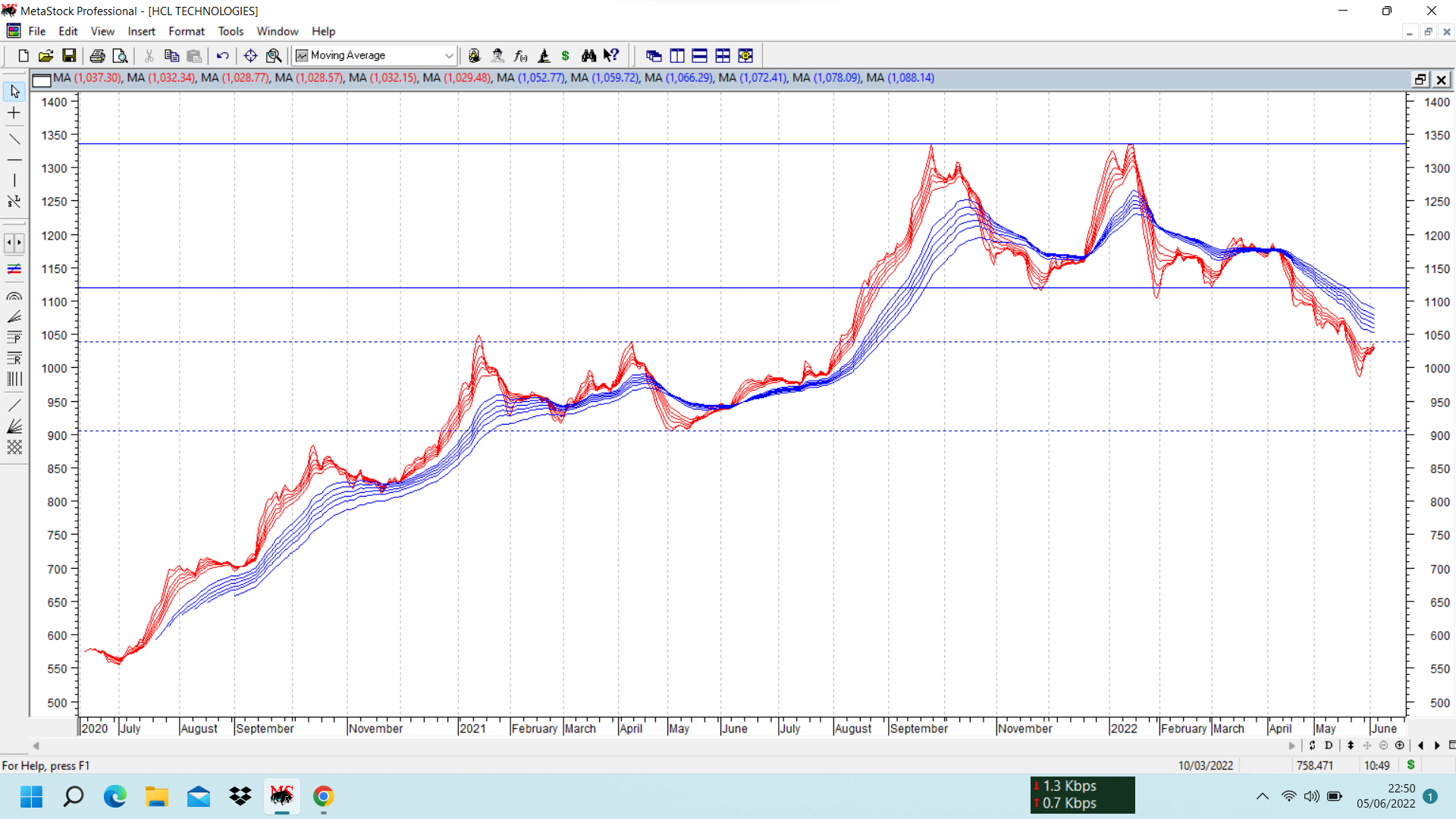

@ktvinay Regarding IT sector, I suggest you read and understand the quote of Minervini I put up a couple of posts back. The relevant few words are " Past leaders that look cheap" . Once you get a hang of those few words, the message is clear. Now Minervini also can get it wrong, and his views might be wrong sometimes with relation to a few stocks and sectors, but I personally am against buying stocks that have broken down and appear cheap because they can keep appearing cheaper on the way down.

Just to give an example of HCL tech, it just recently broke down below 1100-1120 from a double top/stage 4, (call it whatever you like) and once stocks that have been in strong uptrends break down, they will need to consolidate a long time before making an attempt at fresh uptrends.

@Shankar I have already expressed my views on financials many times in the past. No need to keep repeating same on and on. Regarding specific stocks, you can listen in to concall and take a call. Charts wise, these stocks still are in a range of consolidation, so it might need more patience with these names.

Please find attached GMMA chart of HCL tech. Range between two horizontal dotted lines could be a support zone, but we need to be patient to see how this plays out.

And the chart of ultratech which shows two key breakdown levels as shown by dotted horzontal lines.

17 Likes

Hi Hitesh sir,

What’s your view on microfinance companies like Arman Finance. As the Roe crossed 30% and the market has started to take notice.

And secondly what do you think about companies like Iifl finance when it comes to financials. Their Housing Finance Business has been doing better than the likes of canfin homes when it comes to Roe, roa and the aum growth. Moreover, in gold finance they have grabbed market share from the likes of Manapurram. Do you think that broader markets might start taking notice on this one?

Finally, what do you think about Rolex Rings. Which is a proxy to bearing companies like timken, schaeffler and Skf. As all 3 are shifting more capacities to India and reporting solid volume growth. Bearing rings company like Rolex might do well as it’s the sole supplier in outer rings to these companies.

Your views will be appreciated Hitesh Bhai ![]()

Disc: invested in all 3.

19 Likes