I have commented on alembic a number of times and there is nothing new to add. Results expected tomorrow so one can get a better idea post that.

Dr Reddys seems to be on a strong wicket in terms of both domestic and exports growth. Stock price is sideways after having run up from 4000 odd levels to 5500 odd levels. Results due to 28th which will give a better idea.

The first off the blocks in terms of sector doing the outperformance was pharma and speciality chemicals. Post that it seems a lot of other sectors have started participating in the rally which has now become more broad based. So it seems pharma stocks seem to be in a sideways mode after the prior run up. My guess is that once good results continue and markets get more faith that the good results are likely to continue for next few quarters/years too, pharma stocks will resume their rallies.

Valuationwise, one has to take an individual call because sometimes a stock I find cheap might seem expensive to someone else and vice versa. If the business prosects remain solid for consistent long term growth, valuations will sustain even if they have gone up to elevated levels (not exhorbitant levels) .

Hi Hitesh sir

Wanted to know usually how long You hold the stock

What’s your average holding period

I see you merge fundamentals with technicals

So do u hold few stocks for very long term

And few stocks you play momentum

How u divide your portfolio weightage

Just curious to know the rough figures

And have you changed your style and weightage since u began investing

I am also curious to know that is momentum investing is essential to create alpha

I understand everyone has different style of investing and should give more weightage to the style which suits them and is giving them good returns

Thanks in advance

Always appreciate your sincere and honest reply

I haven’t calculated the average holding period of my portfolio stocks. But it ranges from a few months in opportunistic bets to max 2-3 years in long term bets.

A few years back under the influence of some of my long term investor friends, I tried the buy and forget or buy and hold for long term approach but it didn’t work out for me. So I figured out that this was not my style. After reading books on technicals and especially William o neil and The next apple, I immediately identified myself with that style. And its been working for me.

Originally I used to hold many stocks and tended to jump in and out of positions, but the big change in recent years has been concentrated investing. Whenever I feel chips are loaded in my favor, I bet hard. It is for these kind of big bets that I find the techno funda approach useful. If both fundamentals and technical picture align, it becomes easy to have high conviction and bet hard.

There are different phases of market where different styles will work. In a sideways or range bound market, momentum less likely to work. In such markets, there will be a lot of false breakouts and breakdowns.

Momentum investing works best coming out of a bear market. Its pretty easy to spot winners. In bull markets too, sectoral fancy is easy to catch.

Any style that suits the investor’s temperament and practiced diligently will generate alpha. One needs to work hard and develop one’s own conviction, rather than work on borrowed conviction.

Portfolio weightage depends again on market phases. In current markets where sectoral moves are easy to figure out, I tend to make decent sized sectoral bets. Most recent were cement, fertilisers, and steel.

@mpbajaj53, I don’t follow granules too closely, so not much idea why too many DII are not invested in it.

Hiteshbhai, some of the old economy stocks are coming out with good (or better than expected) results (viz. cement, tyres etc) and stock prices have started moving up. Do you think the rally is becoming broad based? And can this continue more a few more quarters - like pharm/Chemicals/IT could move sideways and the cyclicals would start outperforming? Pls share your views.

Have you identified any stocks from the above sectors (except Bayer and/or Chambal, that you have already mentioned )?

@hitesh2710 sir , while choosing any stock in my opinion the opportunity to rise is directly proportional to small equity base and small market capitalisation though there are various others reason and features as well for a good stock, but if a company has undergone capex 5x to 6x in last ten years but it’s sale is not grown to same multiple and also the capex is done mostly by internal accruals has better chances than any big blue chip companies as the ant need less energy to move than an elephant and is more efficient in managing the resources . How far is this postulate works in Indian stock market ? My question is when one should make a switch from concentrated bet to diversified bets as the sh** may happens in case of small caps ?

Regards

Hello Hitesh sir, since this is really my first post here, so firstly I’d like to express my regards and thankyou for educating so many of us here. I feel that just reading your posts is enlightening as it helps clarify a ton of things, so many thanks for expressing your views here.

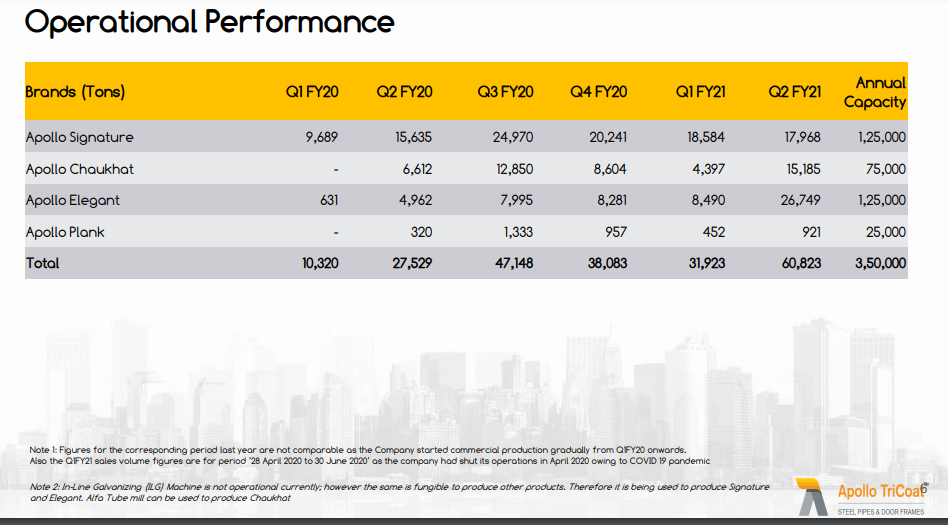

I wanted to ask your updated views on Apollo Tricoat after today’s results. This sector (niche home building products) seems to be largely underpenetrated and it looks like a multi-year (if not decadal) growth opportunity.

My thesis points are:

Promoters are experienced and ethical and have a long term outlook. They’ve done in the past with APL Apollo. Good for minority shareholders.

First company in India and amongst the 4-5 companies globally to produce coated pipes using the galvant and tricoat process. The technology allows the production of galvanized steel pipes, tubes and other products in a continuous single line process based on high quality standards. With access to the advanced technology Co. has competitive edge over its peers as Tricoat products have greater strength, eco-friendly nature, extended life (high corrosion resistance) and enhanced load bearing capacity. (copied from a report)

Products are super innovative and I think they’re taking market share from traditional wooden doors/windows/staircases. Products seem to target mid-to-affordable section of housing as I would imagine higher end home-owners would still prefer wooden doors/windows/staircases coz of that premium feeling. (please do correct me if I am wrong) (see products here: Chaukhat, Elegant, Signature, Plank, Wondoor). Plus they can always leverage APL Apollo’s wide distribution channel.

I did not get the exact gist of your question but I think you were referring to small cap companies with good balance sheets and under utilized capacities as a potential opportunity to invest in.

I think the capacities have to be seen in context of the overall demand picture. If there is existing demand or a promise of poor demand reviving, then it makes for an interesting case.

But one cannot look at investment arguments from a single vantage point. We have to see the company as a whole and analyse it from all aspects and then take a call.

Regarding switching from concentrated bets to diversified bets, its a very hypothetical situation. The whole premise of concentrated investment is built on the foundation that you know a lot about the business and chances of things going wrong are low. One cannot make course corrections in investment style just by fearing that things are going to go wrong.

One has to know what suits ourselves as an investor and try to keep getting better at that style.

Hitesh bhai,

How do u read the alembic pharmas results and more importantly the concall?.

The management has given a guidance of Rs 60 EPS for the current year, which seems to be very conservative and considering their performance in H1, they are likely to do better than that. When seen among results of companies from other sectors, it is clear that pharma has once again done very well and Alembic has clearly outperformed on all counts.

But the surprise for the market seemed to be their guidance for FY 22 with an EPS of Rs 50. That means a reduction of around 190 cr in net profits on new capital. Further a new plant will incur operational expense of 450 crores and will keep increasing at a decent pace going forward. With these two numbers, other things being equal it seems that the top line will grow around 12-13% in FY22. The market didn’t seem to have liked it and fell by more than 3%.

So how would you read this stock going forward. There is no doubt that even next year onwards too their performance will be solid from existing facilities but with additional expenses and capex, FY 22 may be a subdued year. Also with new plants, for production to reach a optimal levels and attain operational leverage will take some years. So can we consider this stock still as a fast grower or growth like 25-35% as of now seemed to be over?. Is it wise here not to bet big?

Secondly, how do you see companies doing more and more capex. Though investing for future growth opportunities is good but if it doesnt pay up well with revenues and profits, the ROCE will be hit.

I dont track apollo tricoat too closely but had a brief look at the recent quarterly results and it seems the company is on a strong growth path. It has reported stellar numbers for the quarter. There has been a sharp run up in anticipation of good results but I think looking at the results, if management commentary is positive, there can be further upsides.

@Suman1 I don’t track any of the companies you mentioned. viz. niacl, tata chem or sundaram fin.

Alembic q2 fy 21 results have been along the expected lines. The big surprise has been the EPS guidance which the management has given for this year and next year. I havent heard them mention exact numbers before. So that for me is a surprise.

The reason for that could be to allay investor fears of severe de growth in earnings over the next few quarters due to higher burden of depreciation. These kind of numbers probably establishes a floor to the earnings for the periods mentioned;. If the company can deliver better than the promised numbers going ahead, there can be upmoves in the stock price.

For us, we have to figure out from where the positive surprise is going to come. Revival of domestic growth can be a good avenue of growth. Exports is going steady. Another small but significant factor can be royalty income from TG therapeutics. TG Therapeutics has been given permission to conduct phase 3 trials on U2 molecule in patients of CLL. It has already got approval for marginal zone lymphoma and another less common variant of lymphoma. If company can succeed in phase 3 trials and is able to lauch the drug for CLL (where number of patients are much higher than other variants of the disease) then it can generate better than expected revenues and hence higher royalties for Rhizen and hence higher share for Alembic. Any quicker resolution to the USFDA inspection (which is pending due to Covid) can be a positive.

Till the time any or all of the above triggers materialise, stock price might not move much. There can be range bound movements in stock price.

What is your view on Joe Biden winning the next US elections and democrats taking control of the congress also. They want to have a public option for healthcare and want to allow medicare to directly negotiate with pharma companies to reduce drug prices.

As per my limited understanding, US pharma market is so lucrative primarily due to lack of any price controls / collective bargaining by healthcare providers which happens in other developed countries (where pharma companies have to disclose their cost structures also in many countries)

I think the US election outcome can be more of a market specific risk rather than a sector specific risk. A new president in the White house could mean change in a lot of policy decisions. But having said, that, Trump himself is not too much to talk about in terms of continuity of any policy decision. In fact he always has had the business community in emerging markets on tenterhooks with his frequent tweets. So in the normal course of action, Biden may not be such a bad idea for the markets in terms of more sanity in decision making. (hopefully) But all these things are matters of conjecture and we dont have any control over these things. Thinking too much about the impact of a new president on pharma sector I think is too early. We have to see how he goes ahead with his plans.

What we can decide is the companies we invest in or not invest at all and sit on the sidelines. If we are too worried about the markets, we can always sell partly/completely and sit on the sidelines.

@hitesh2710 and others. Wanted your advice wrt the recent buyback announcement of Rane Brake Lining buy back offer. It was announced few days back https://www.thehindu.com/business/Industry/rane-brake-to-buy-back-22-cr-shares/article32865537.ece

I bought after the announcement. It opened yesterday, but my ICICI direct didn’t show buyback offer in the demat a/c. Today I saw the announcement of the buyback done by the company, https://www.bseindia.com/xml-data/corpfiling/AttachLive/94980b48-4d67-4a0a-8f51-46011168fba6.pdf.

Since I had not previously participated in any buyback offers, I thought this would be a good time participate in one, with very small allocation, mainly to learn about it. But now I am confused. If the buy back offer does not show up in the demat a/c, how does it happen? I can see other buy back offers listed like Cheviot, RITES etc. What should be my next course of action.

Any advice would be greatly appreciated.

Kopran results have been very good . It has continued the improvement in numbers shown in q1 fy 21 and that goes to show that this trend can continue going ahead too. Two continuous quarters of good growth is something that cannot be brushed aside.

Since we do not have any more details about the contribution of api and formulation or domestic vs exports etc, we have to consider the results as a whole and that looks good. Going ahead, with commissioning of the new facilities better growth can be expected. When those facilities get operational needs to be seen.

What seems favourable is the valuation as compared to the broader sector. Half yearly EPS is at 7.1 and if we consider similar numbers for H2, then full year eps can go up to 14. Based on that, even after current run up stock looks cheap.

Glaxo results are difficult to decipher and predict. They come up with frequent nasty surprises in term of write offs and extraordinaries etc. I gave up tracking it long back.

Read through Jack Schwager’s Market wizard series books.

Some of the guys have phenomenal track records in terms of CAGR for periods ranging from 5 to 10 to 15 years. And these rates often go up to 50 to 100% CAGR and more.

I found that the books are not written too well. The interviews and perspectives of the guys featured in the book are often looking like a superficial job.

But I plodded on and tried to finish most of the books by skimming through certain pages that contained details about guys involved in commodities, options etc . Some things that came across about all these investors/traders are:

Most of the guys came from modest backgrounds and began their investment journeys with small capital. Some of them also lost a lot during their early phase of the career.

One streak common to all of them was persistence in their chosen profession inspite of little initial success. These guys kept at it and tried to refine their processes and ultimately made it.

Most of the guys reviewed their mistakes by writing down details about all their trades and then found out where course corrections were needed.

The common learning from all of them was to exit losing positions as early as possible with minimum damage and keep running the winners as well as possible. This applies to investors too. Instead of living in hope, better get out of a losing position and think again.

What reading these kind of books do is it helps to dream big. If these guys have done it, its possible to do.

The narration in the books is not top notch and does not hold reader interest but for me , I used to read it at bedtime and it usually gave me good dreams about making it big.

I think this statement is not suitable for long-term investors. Stocks or businesses may not start to perform just after your entry. Peter Lynch also emphasizes that this is something that gives retail investors an edge over fund-managers. Stock price may crash 50% just after we buy a stake but that does not mean we should exit realizing the losses. If you analyze the multi-baggers of ace investors like Jhunjhunwala, Kedia or Pabrai etc. you can find similar patterns - when they purchased Rain Industry, Aegis Logistics, Atul Auto etc.