Regarding kaveri, you can go through the thread on kaveri seeds and form your own conclusions regarding the company. There has been enough discussion on the thread regarding the issues you want answers to.

I try to focus on numbers rather than narratives. There can be as many stories as there are tongues.

@hitesh2710 bhai, even I strongly believe in following numbers.

Chine me ye hoga,

People will go for movies within a month from now,

ITC will get rerated some day,

Chemical sector will revive next quarter,

People will start flying next week,

People will take vacations a month from now, etc.

All these are fictional ideas & sampling errors that we create in our heads. Without numbers to back such stories, these stories remain just that - Stories, that don’t materialise most of the time because there are too many moving parts.

While writing this I remembered a famous experiment Prof. Bakshi talked about in his Flame university workshop.

In this very insightful article, Michael Mauboussin says, is it is difficult to predict winners in something as simple as movies / music albums which have far lesser moving parts than the investment business where the parts are too many and too volatile. Hence, unless numbers don’t support the story, it could be a logical error to even guess what will happen next week, next month, or next year.

On the other hand, don’t narratives matter too? Without a strong narrative, stocks don’t get assigned “forward P/Es”

What are your thoughts on the importance of a story backing up the numbers?

I think the narrative vs numbers is summed up in the quote

In the short term, market is a voting machine (narrative/opinions), and in the longer term it is a weighing machine (numbers).

If a company continues to churn out numbers on a consistent basis, it is bound to take up stock prices and improve market fancy and assign a higher PE ratio.

Sometimes in shorter term, there are factors like concentrated selling from big players, e.g Pabrai funds in Kaveri and Uday education and Bhailal Amin trust in alembic pharma . In the backdrop of sharp upmove in stock price followed by a QIP, creating supply side pressure, stock price will find it slightly tough to move up and show strength. This situation can continue till buy-sell equilibrium is restored and and that often takes time.

We should be worried if we want to sell out of the company in question. If we want to invest for the longer horizon, stock quote is just a number and should not mean much.

Having said that, I am not a buy and hold forever kind of investor. Neither am I buy and sell on a small rally kind of investor. So for me these kind of situations are par for the course until the time I feel like selling out and switching out to a seemingly more lucrative opportunity.

One should learn to have a portfolio approach. Basically in a portfolio of say 8 to 12 stocks, if 2-3 do not move much or even if go down slightly, it should be okay. The key should be 2-3 which go up and sometimes go up 2x or 3x and these are the kind of companies which make a huge difference to portfolio returns. And if allocation to these names is decent enough, its the icing on the cake.

Thanks for sharing wonderful practical insights as always. I have one follow up question.

How to decide on allocation to a stock where both numbers and narratives are strong and where stock is trading near all-time high?

For example, I wanted to invest 25% of portfolio in Laurus labs after studying it in depth and convinced about long term story. I am a “Growth At a Reasonable Price” type of investor with investing horizon of 3-7 years.

Initially I invested 10% of portfolio in Laurus labs at 850. After results concall, it quickly moved to 1050 – 1100 range. Then I was thinking of buying on dips below 1000 but it never gave that dip and quickly moved above 1200.

So what is better allocation strategy in general.

Should we wait to buy on dips because in short term, even stocks with strong momentum and sector tailwinds can correct significantly due to different factors (e.g. - accident in plant like Transpek, market fall, overvaluation etc.) which may or may not occur.

OR

Should we average up without thinking about these probabilities as anyways we are investing for long term?

PS: Not asking stock specific and gave Laurus labs as a recent example. But I observed many times in the past that stocks with strong business & sector tailwinds move up very fast with each successive quarter as trend develops and it becomes diffficult to allocate more later on.

One advise that a lot of experienced investors seem to be giving is that in small caps it is not easy to exit. So when valuation get rich you should take some profits. Contrarily these are the stocks that are likely to give multiple returns.

So with some of the stocks having run up considerably I am seriously thinking whether to cut down some small cap positions. Valuations are still reasonable in some cases and little high in others.

Should we have portfolio approach and balance the small cap component to a range.

My current instinct is to let things run but in past I have seen small caps being very volatile. Even if I stay invested in these names but trade in out of based on levels.

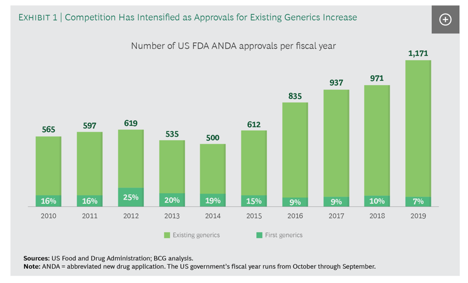

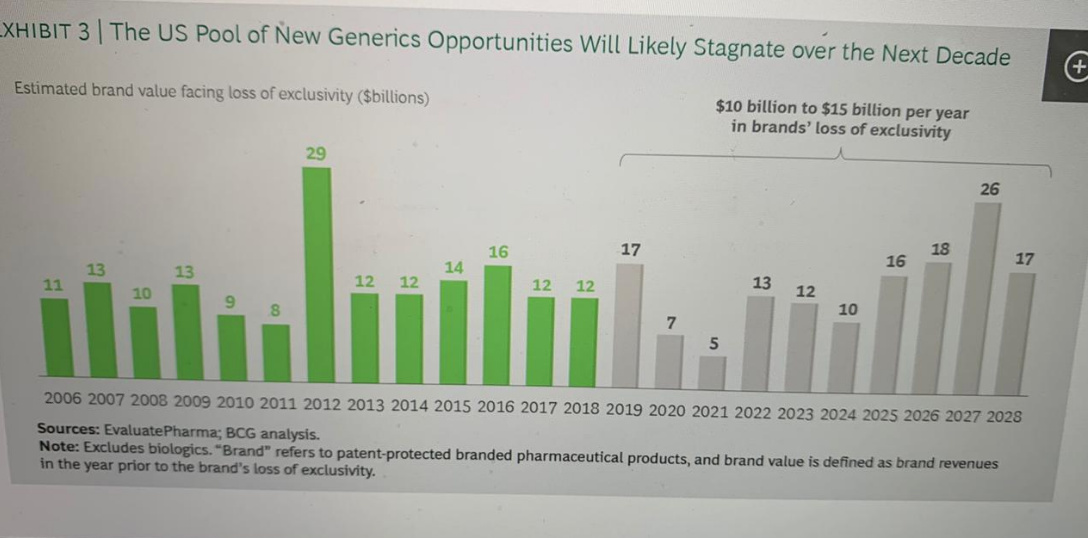

On the one hand we are seeing number of approvals given by the FDA growing rapidly (and competition increasing). On the other, the potential pool of drugs going off patent seems to have peaked out and especially over the next 2 years seems to be falling significantly. Few questions related to this:

Does this not indicate that the generic pharma industry as a whole is going to go through a tough time over the next 2 years?

In this scenario, if Indian pharma were to outperform, we would have to gain significant amount of market share. Are there any triggers for the same?

This scenario has persisted for the last few years, yet FY19 and FY20 numbers for most pharma players seem to be really good. What could be the driver behind this outperformance?

Allocating a big part of the portfolio to a stock after a sharp run up is a tough decision to make. Laurus has gone up nearly 4 times from its lows and although it does not show any signs of weakness, the fact remains that run up has been pheonmenal.

Fundamentally the company is on a purple patch with all engines of growth firing simultaneously and management commentary also very strong. Add to that the sectoral fancy and stock prices can take off really strongly.

I think what one can do is to wait for small dips and keep adding gradually if one is convinced about the story fundamentally. Personally the last tranche I bought was at around 520 kind of levels during the second lot of sale by Warburg Pincus. Post that I have not bought it and in fact reduced some holding because the portfolio weight was going out of proportioins. But even post that the stock price continues to rise and seems to be showing good strenth.

Averaging up works till the time the chips are loaded in our favour clearly. That is, when stock appears cheap on traditional valuation parameters. So maybe adding dips can be a good idea in case of Laurus after such phenomenal run up. Having said that, no one knows where stocks at all time

high can go, so one has to take one’s own call.

Alternatively one can look at companies like dr reddys, alkem etc which have solid well rounded business models and great managements and which still have not run up too sharply and see if there is any investment merit there.

In the investment world, when we are investing in a company or when we are invested in a company, there will always be something or the other to worry about. How much importance to attach to these worries is something we have to take a judgemental call on.

I dont know where you have got the data points from with all the charts and stuff, but it would make sense to counter check these data points from other sources to see if the picture presented here is the true picture or imagination of some biased analyst.

What is a fact and an iundisputed fact is that most export facing pharma companies have reported fantastic numbers and commentaries from most managements is bullish. I would tend to go with these numbers and management commentaries rather than rely on projections of molecules and revenues going off patent.

If you are very interested in kaveri as an investment candidate, I would suggest that you go through the whole thread of Kaveri seeds from start to finish and go through the annual reports of past 5 years and maybe listen to last 2-3 years concalls (they do concalls regularly and are quite transparent in answering questions. Maybe even ask questions by logging in to concall too so that you get answers from the horse’s mouth. )

This is a slightly long drawn out process but the results of this exercise will provide all the answers needed to questions related to kaveri before investing in it.

PS. You need to check if advanta is still trading independently. As far as i know, it was merged with united phosphorous. You can get the details from UPL annual report.

I don’t think we should rely on either estimate and cross that bridge when we get there and decide based on whatever new info becomes available w.r.t the available future market opportunity.

Another thing to note is that, companies like Alembic & others would take at least a few years to monetize the ANDA approvals they already have (191 ANDAs approved in the case of Alembic) before stagnation becomes a reality.

Both seem to be reputed sources. But will dig more and see if I can find any data that says otherwise.

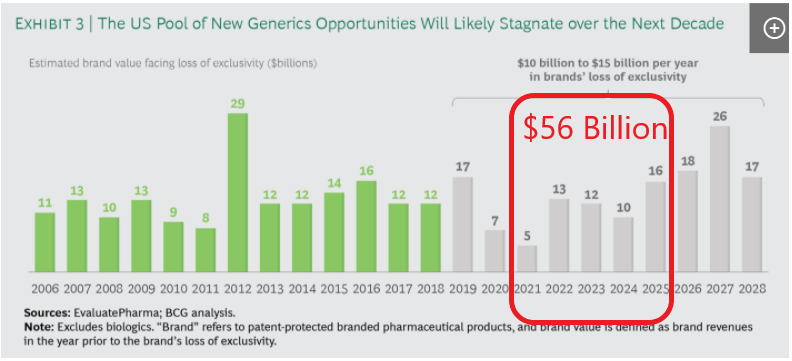

Even if the amount of patents losing exclusivity is $100bn over next 5 years, that is still less than the preceding 5 years based on the IQVIA report. I was a bit concerned by the environment of 1) increasing approvals and increasing competition in the US market + 2) seems like at best the value of patents expiring seems to have peaked.

Despite this, most pharma companies have been delivering phenomenal numbers and have been giving really strong guidance for the future, what is driving this performance and optimism from an industry perspective? Is it the China API issue, have we been gaining market share due to it? If so, is that sustainable? Or are there some other reasons?

P.S: New to this industry so still trying to learn. Starting from a top down picture. But got intrigued since the data overall seems to not be corroborating with the results being declared.

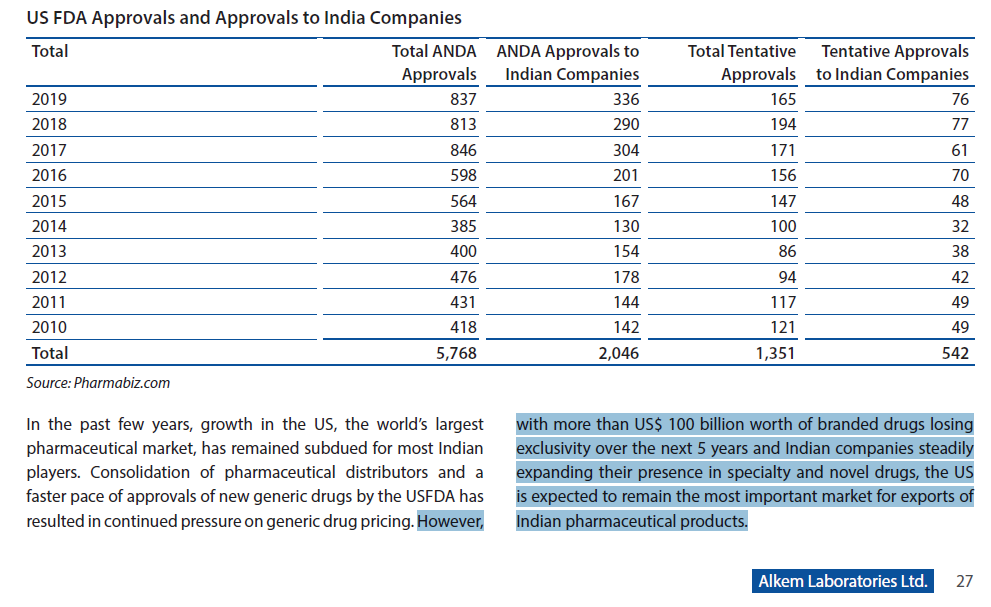

If you want a picture of the US generics industry, you should go through the annual reports of Indian companies that have a significant presence in that market. Companies like sun, lupin, aurobindo, drl, cadila, glenmark, alembic, alkem etc.

A brief look at management discussions and analysis, and chairman and ceo message will provide the true picture rather than all these external data sources.

Sir, do you track Solara Active? while their Vizag plan will start adding to the pnl. there have been similar issues of pledging like Laurus (ofcourse not comparable from business standpoint). Next growth from API and CRAMS verticals

wanted to know your views.

Can you please help me to understand rational behind PE ratio…

Few companies enjoy high PE ratio where as market doesn’t offer better PE ratio for few good companies.

For example.

HDFC bank. India’s no #1 bank. No any scams ( not am aware of anything) , cash rich company and consistent growth for

many many years and there is no doubt about future growth. However, the PE ratio for HDFC bank is always between 23- 29.

TCS: Cash rich company, uninterrupted cash flow, consistent growth and has been multibagger for many investors. Backed by strong management

( Tata group). No doubt about the future growth of the company. Still PE ratio has not crossed 30 at any point in time.

Whereas few companies enjoy high PE ratio

Eg. Titan , Page industries, Asian paints.

What is the key factor that market will consider to offer high PE ratio for these companies compare to HDFC bank / TCS.

PE ratio and the rationale behind it is a whole subject by itself. Its not something that will unravel itself in a single post from me. You will have to put in some hard yards and read up relevant books, and some posts on the subject.

Basant Maheshwari in his book the Thoughtful investor has covered the subject as far as I recall it. There is Five rules for successful stock investing by Pat Dorsey which also I think deals with the subject.

And PE ratio is not something etched in stone. It is a valuation market is willing to give to a company based on a lot of factors and market levels. I can give you an example which taught this thing to me. Ajanta pharma back in 2010-11. The stock had grown its earnings at a cagr of 37% cagr in previous 5 years and was available at PE ratio of 5-7 for a period of around 1 year post that. You can go through the thread on ajanta from the start and see the posts which shows my disbelief about why the stock quoted only at 5-7 PE inspite of consistently good quarterly numbers. And 3-4 years later, it was quoting at around 30-40 PE.

You can also go through a thread on art of valuation on VP.

Observed Cadila Healthcare gaining momentum, its near to 2 years high and already 20W EMA crossed 200W EMA. I don’t have much understanding on Pharma domain but sector tailwind looks favourable. Also, Q1 Y.O.Y. numbers looks good. Will appreciate your views

Cadila is as you say gaining momentum along with most of the pharma companies. Its almost a dart board in the pharma space with the rally starting to be broad based. But the key to better returns remains in picking up the companies with best growth prospects, good management and good balance sheet.

Companies where capex is finished or nearly finished and debt is not too much of an overhang also will provide good returns. Earlier it was only the API and CRAMS/CDMO players which were running hard but now it seems most pharma stocks are showing good strength.

I dont track cadila in too much details, but its charts look bullish. Alembic pharma after nearly 5 weeks of correction seems to have reversed direction by giving a bullish candlestick closing this week. Alkem is a company which I like fundamentally and is undergoing sideways movement recently. The latter two are companies I have been accumulating since past couple of weeks.