@barathmukhi

I think by sectoral excesses, there are different factors that need to be considered while arriving at a conclusion. A single instance or a single parameter would not provide a complete picture.

For the sector in fancy, valautions for a lot of companies within the sector go out of whack. Recent example was financial sector esp the nbfc sector.

One can understand crazy valuations for companies like bajaj finance which had demonstrated superb track record of sales and profit growth for many years in a row. Even there, people had started posting on VP about them being bombarded with too many calls and messages for getting loans. It had gotten to almost a point of constant irritation. Now when does this happen? When there is a lot of pressure on sales force to get customers. That shows desperation on the part of the company to chase growth.

Other companies like au bank, mas fin etc also were showing good growth but all said and done, they were smaller companies which had reached very high valuations on Price to Book. Companies like bandhan were bandied about as the next big thing irrespective of the inherent risk in the business model.

Whenever there is a consensus in the investor community about the invincibility of a sector, usually a top is not far away.

I can recall similar thing in case of pharma back in 2015. People were thinking that the consistent 25-35% cagr growth shown by a lot of pharma companies in the run up to 2015-16 was going to go on for ever. And accordingly high valuations were accorded. The sector leader made stupid acquisition in terms of acquiring ranbaxy which was a fairly big sized troubled acquisition. Lupin acquired Gavis. Many other companies went about with big expansions. Effectively supply side dynamics were getting challenging due to huge over supply. Back in 2015, most investors agreed that pharma sector was invincible and everyone loaded on to it. And then we knew what happened.

So one has to be on the lookout for excesses from the market participants as well as the owners/managements of the companies in market fancy.

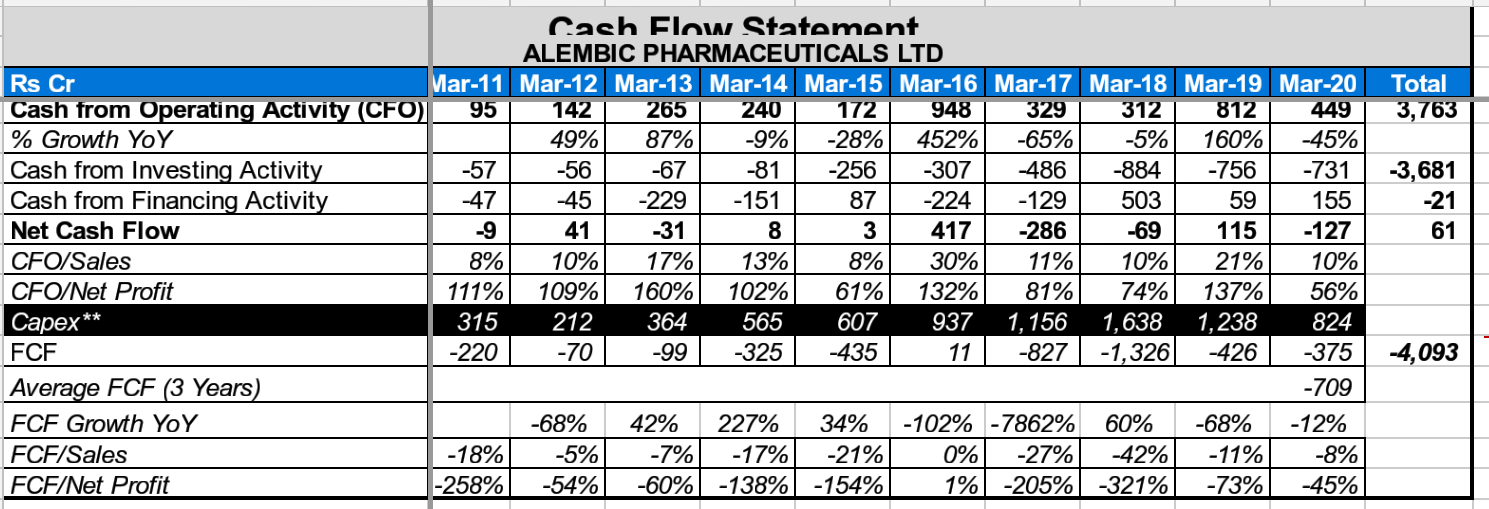

Coming to how to play the sector having market fancy/tailwinds. Usually whenever a sector reclaims market fancy after being out of favour for long time, the fancy does not go away quickly. If we look at the pharma pack, companies like dr reddys, cipla, alembic, laurus, aarti drugs etc crossed all time highs in last 4-6 months only. A lot of these companies started delivering good results only since a couple of quarters. So both business wise and stock price wise, the trend seems only a couple of quarters old. Once a trend starts, ideally it should run for alteast run for a few quarters, usually atleast 1-2 years if not more. And this sector will throw up a lot of multibaggers. That seems to be the case with stocks like aarti drugs, laurus etc going up 3-4 X or even more. There can be more to come. At present only a small segment of pharma sector has provided outsized returns, namely bulk drugs players. The large cap pharma companies seem to be in early phase of their bull runs. So we need to see how far they go. In the beginning of a strong uptrend usually there is a lot of disbelief and hence after every upmove a lot of sideways consolidation. Once the take off phase is over, the real strong uptrend begins and that is the trend to ride. My belief is that large cap pharma and the other big companies in the sector is on the cusp of a major trend. Need to see how it plays out. Currently market seems to keep undergoing sector rotations with most sectors having given decent bounces while the pharma pack has largely consolidated.

Stocks like drl, alkem, cipla etc have recently crossed their respective all time highs and are consolidating post that. Once a stock takes out its all time high it tends to go up by 30-50% from that level atleast, if not more. So it seems these kind of companies have more fuel in the tank still left.

So I feel if we are talking about the pharma sector, thinking about profit booking in general seems to be too early. In specific instances as in case of aarti drugs, at around 3500 plus, where there seemed to be buying frenzy, maybe profit booking would have been advisable. Usually that is indicated by parabolic rise in stock price. The chart always gives a good idea to identify buying manias.

I think even if one is not a guy inclined to track technical analysis, or does not agree with the concept of technical analysis, it is advisable to read THE NEXT APPLE book. I feel it is more to do with the psychology surrounding the big winners rather than specific technical analysis. It also provides a framework on finding big winners and how to ride them.