Hi @hitesh2710,

This is a very helpful summary of things to look for. Do you have a more comprehensive version available somewhere, on this site or elsewhere, either written by you or someone else?

Hi @hitesh2710,

This is a very helpful summary of things to look for. Do you have a more comprehensive version available somewhere, on this site or elsewhere, either written by you or someone else?

Hello Hitesh bhai,

What are your thoughts on Muthoot Finance (red group) at current scenario?

Prefer Muthoot over Manappuram due to higher customer focus by management + lower exposure to MFI. But Manappuram has higher online gold business (61% of its book as of Q4FY20 while Muthoot is in single digits one year back).

Thanks!

Discl: Added to portfolio in last 90 days

I think you have covered most of the investment arguments concisely for Muthoot finance.

Gold loans carry little risk of bad loans being converted into NPAs. And in the current envirnoment it becomes a big positive where most finance companies have a hard time, trying to recover EMIs amidst dwindling incomes.

And with other institutions curtailing loans under other heads, gold loans will become a ready source for raisinng funds for retail guys.

Management wise also Muthoot group has been less adventurous than Manappuram and hence lesser exposure to MFI which seems to be the cursed sector these days.

Valuationwise also at less than 3 times book and 12-13 PE, though not too cheap its neither too expensive. As far as I recall they have not diluted equity too much. (need to check). Companies that dont dilute equity too frequently and do well fetch, higher P/B because we know that whenever in the future they dilute equity at a premium, book value will go up.

Technically also it seems to be forming a cup and handle pattern which confirms on crossing and consistently closing above 875. If this pattern suceeds, target could be 1200. But since financials are at the receiving end in the markets, I would be very careful in looking out for bullish targets.

Hitesh Bhai

Whats your views on recent results by Ajanta Pharma N DRL ? is drug shortage n rupee depreciation helping all pharma exporters ?

Hello Hitesh Bhai,

Do you track Astec Lifescience? It is a small Godrej group company in agrochemical space and promoters are continuously increasing stakes in past years (now at 71.33%). Company has come out with great numbers for Q4 FY20 (EPS of 16 vs FY19 full year EPS of 18). Management in recent conference call (of parent company Godrej Agrovet) mentioned that they expect Q4 FY20 performance to be repeated in future. Stock price has gone up quite a bit in last one week. I feel this company has legs to go. Need your views on this.

Dr Hitesh,

Good Day,

With great respect, i would like to thank you for your valuable inputs in the forum. This has been interesting journey for me to learn and listen keen then act.

If you have any views on the below 2 stocks, can you share them :

Aditya Birla Fashion & Retail : Indian clothing retail with brands such as Louis Philippe, Van Heusen, Allen Solly and Peter England.

Inox Leisure : Multiplex

Due to covid-19, these stocks have badly hit to their lows and slowly they are resuming to grow…

Both ajanta and drl q4 results views posted on ajanta thread. In addition to them both companies have very good balance sheets with net cash. And hence PE valuation could be higher.

In case of drl,if one accounts for inventory write off in q3 fy 20, pbt has gone up 55% and if eps is calculated accordingly, the valuations might not appear as expensive as they currently do. It remains one of the better placed large cap companies with top notch and ethical management and well diversified business.

Ajanta has finished most of its capex and capacity wise, growing for next few years should not be a problem. Demand side needs to be monitored. Again exports is well diversified and all gegographies seem to be doing well in exports. US business is relatively small to the tune of 500 crores annually and hence a small base to grow on. So though it appears expensive, it could attract investor interest.

Disc: I have recently entered into starter positions in both ajanta and drl.

@Marathondreams I dont track astec life.

Hiteshbhai

Please share ur views on ITC at current valuations…

Thanks

ABFRL even after the correction does not appear too cheap on valuations. Besides this, looking at the nearly 2 months lockdown, q1 fy 21 results are likely to be washout. Even with opening of lockdown, these kind of businesses are not likely to start kicking at previous rates too soon. I think it will take a few months atleast to start showing sales momentum.

Inox is in a similar predicament. Although govt might allow it to open with some restrictions, it will again take a long time to regain higher occupancy levels. Even people like you and me will be scared to go into multiplexes because of fear of contracting of the disease.

These kind of businesses should be considered once we have definite signs of number of infected cases going down. As of now, I am not even too sure how many days and weeks it will take to achieve peak numbers after which the numbers will start reducing.

In my view its better to be patient in buying these kind of businesses where there is a lot of uncertainty about business momentum and timelines are not clear.

Stocks which have hit multi year lows can go even more lower and still some more. Reverse is also true. In these uncertain times its better to be in businesses endorsed by markets where stock prices have shown relative strength in response to business strength.

@Kuldeepjadeja ITC thread is well populated with learned opinions. I dont know if I can add anything more useful.

Hitesh bhai - what is your views on Bajaj Finance given that RBI has extended the moratorium period by another 3 months time.

Extended moratorium given by the rbi increases the timeline of uncertainty for lenders. The lender is not certain who is going to pay up and who is going to default till the moratorium lasts. Markets also.know this and it rubs on to the stock price.

This usually what happens to a stock in a strong downtrend. You decide that at a price (e.g 2000-2100 i in case of bfl) all the negatives are priced in and there is limited downside left. And what happens next? Another unexpected negative event/newsflow rears up its ugly head to push the stock price further down the cliff.

And still people keep bottom fishing.![]() Trying to catch the bottom is a difficult task and requires a very special temperament and skill set and very few people have it mastered.

Trying to catch the bottom is a difficult task and requires a very special temperament and skill set and very few people have it mastered.

Buying when there’s blood on the street looks like a simple statement. But doing it practically is very tough because many a times we end up donating our own share of blood to that on the street while trying to catch a bottom. And the long held high conviction goes away often at the wrong time, actually very close to the real bottom

@hitesh2710 bhai, it is usually said that market is forward looking but at the same time goes on both extreme for valuations and thus opportunities.

In your view what could be positive triggers for BF( and rest of top league banks) that could possibly sooth market nerves against financials particularly.

promoter buying, solid disclosure didnt suffice for BF in current juggernaut.

I think people who are starting their investing careers should be made to read these paragraphs repeatedly. If I had read this earlier, would have saved a lot of my own blood!

Even after many many involuntary donations, I still keep getting tempted with catching the bottom. Although I think trying to catch the market bottom would be less dangerous.

@hitesh2710 ji,

Do the larger chemical manufacturers have better B2B brand & capabilities and thus more chances of exclusive contracts? For example: Atul vs. Transpek.

Its great to see Bajaj Finance being discussed so passionately on its way down. ![]() Reminds me of similar passionate discussions on avanti feeds, some pharma names when they were going down, yes bank thread, dhfl thread etc.

Reminds me of similar passionate discussions on avanti feeds, some pharma names when they were going down, yes bank thread, dhfl thread etc.

I am trying to bring investor psychology here. In the immediate weeks and months following price crash in what once was a market darling, there are always those who sing merits of great business models and great managements (often rightly but at wrong time) . From an investor psychology point of view, stocks and sectors don’t bottom out when a lot of market participants keep discussing them and are interested in them.

Case in point being export facing pharma companies. These were market darlings and on the way down say in case of Sun pharma, people found it cheap when it corrected from 1200 to 700 and then on to 500 and so on. And all the interest died down from 2018 to 2020 when it was in the last leg of its correction. Hardly anyone talked about it and if at all there was talk it was about some corp governance or usfda problems or some such other matter. These are the times of total investor apathy when bottoms are made in stocks.

But as investors our aim should not be to try to catch these bottoms. Because even after formation of bottoms, these kind of companies often take months and years to move sideways and cause frustration even among those who have bought close to bottom. Our aim should be to start looking at these names once business momentum starts picking up in the stock and or the sector and that is reflected and endorsed in stock price. Thats when the waiting period of getting returns is low and the invested capital provides quicker and more surer returns.

As of now, I think Bajaj Finance is on its way down as we see in the results also. June qtr is going to be a washout. So is Sep qtr because of the morat extension. So that takes us up to Oct-Nov in terms of getting clarity of how delinquencies are going to pan out. Forget about growth during this period. And this is the earliest I can think of. If morat is extended further due to one or the other reason, the timeline gets extended. So what is the haste to buy Bajaj Finance? Personally speaking I am not interested in catching the bottom. I would be perfectly happy to buy 15-20% or more above the bottom also provided I see something clearly in the fundamentals or on charts. As of now whatever I can read or think about the company and its business is only an educated guess or a smart sounding theory which may or may not be correct. (of course there is no harm in writing or reading up these theories but bottomline is making money based on these theories is going to be difficult till the market agrees with your view.)

I personally prefer to spend my time and efforts in places where I see chances of making money and financials is not a space which provides such chances as of now. So why bother. ![]()

Hi Hitesh bhai,

What’s your view on MNC pharma sector ? Because of more patented medicines and introduction of newer products from parents basket plus the 5 years tax benefit for patented products , would it be better compared to domestic companies? Many thanks

@hitesh2710 Very nicely put Hitesh bhai… I think it’s lies in our sub conscious nature to catch falling knives

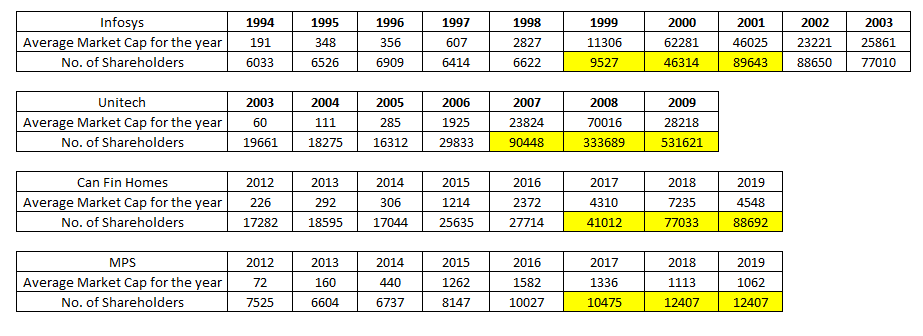

Here’s some data I collated from the annual reports of these companies. As we can see, the number of shareholders almost always goes up when a sector leader falls. Even after these companies’ glorious days were over, the number of new shareholders kept increasing. Like everything else in the stock market, there will be exceptions to this rule. But generally speaking, this pattern plays out. So we should watch out and not fall in the trap called Anchoring bias.

Maybe that’s why averaging up is almost always a better idea than averaging down. I would rather buy Bajaj Finance at 20% higher than whatever bottom the stock price touches than buying it today.

I have burnt my fingers in two MNC companies namely Multibase and Glaxo pharma. So have decided to be away from these unless I have a very very compelling and convincing investment candidate.

@kartiks, I dont track hexaware.

Hitesh sir, Your messages are a Masterclass. Many great investors advise to look at sector that are out of favour and be contrarian. But that still leaves a lot to be answered. This message of your succinctly mentions how those sectors would look like from an Indian context.

So considering that pharma would be a great place to look for contrarian bets, how can we filter down to individual stocks to invest? Can you provide a couple of stocks that looks interesting at this stage?

Hitesh Sir,

Can you please share your views on DB Corp. I read in the DB Corp thread that you held it at one point of time. I feel that the stock has taken an excessive beating currently. Screener is showing div yield of > 15% and there doesn’t seem to be any specific news. At an EV/EBIT of 2.3, it seems like a good value buy.

Thanks

Considering investiment. Currently in watchlist. This and Jagran Prakashan both