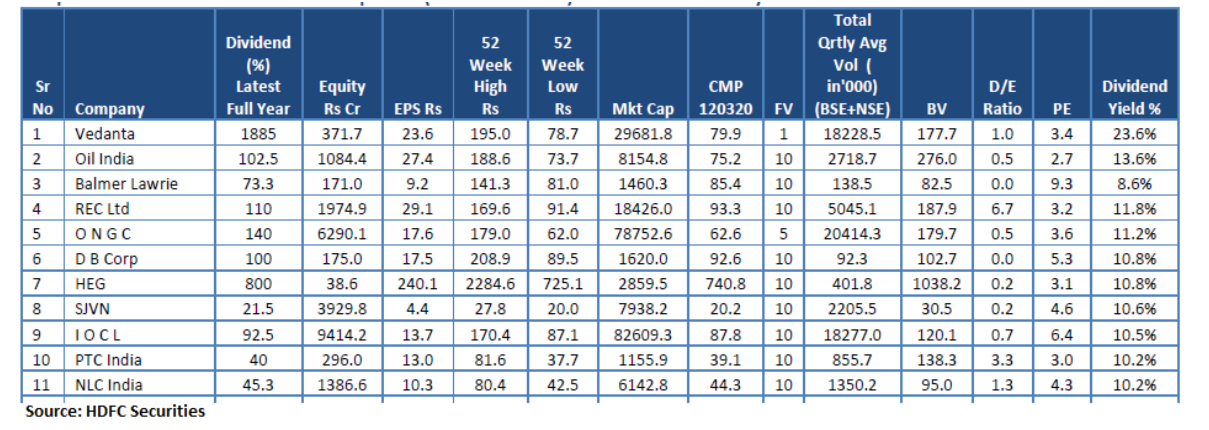

We have been having a rough volatile ride in the markets since past few trading sessions. All during the fall as I have articulated earlier in my posts as well, I have been trimming/selling off my portfolio positions and now sitting at comfortable cash levels.

With the strong downswing a lot of companies we have tracked have come down to very mouth watering levels if one goes by the easy way of looking at the conventional valuations parameters like PE or P/B etc.

However for companies where there is a clear run way and there are no issues with corporate governance, valuations in most cases are still not no brainer types. Just to give an example, I got some examples from a Whatsapp forward (not checked exact valuations but my guess is the value shown in the post will match the real valuation close enough. This is for purpose of approximation and doesnt need to be exact)

Godrej consumer products peak PE 62x, current PE 22x

Marico from 60x to 26x PE

Havells from the peak PE derated from 70x to 38x.

KRBL down 80% from peak of 35x PE to 5x PE

Page ind from 102x to 48x

Eicher from 81x to 17x

HDFC AMC: 68x ti 33x

HDFC Life 131x to 61x

La Opala 70x to 17x

Bharat Forge 71x to 15x

Astral poly 135x to 51x

ICICI lombard 60x to 41x

Titan from 85x to 55x

Kajaria 50x to 20x

Nerolac 65x to 36x

Berger 95x to 70x

TVS motors 89x to 20x

VIP Ind 60x to 20x

Bata 82x to 40x

ITC 45x to 13x

KEI Ind 26 to 8x

Zee 60x to 7x

Maruti 48x to 20x

Britannia 78x to 44x

As can be seen from above, companies like krbl, kei etc are cheap on the parameters described above. But these have issues of their own, as we know in krbl, zee atleast.

Now what we dont know is how the next few quarters, say q1, q2, q3 of FY 21 are going to pan out and whether there is likely to be de growth or not. If there is de growth then above valuations will become even more expensive. However if the bet is that there will be strong growth due to pent up demand (also a possibility) then one can definitely consider investing.

For myself I am not too clear how the situation going ahead is likely to pan out and hence am sitting on sidelines and would be likely to do some trading in highly liquid names if I see a good enough opportunity or opportunities.

@axiskumar I did not get your question. But my guess is it is to do with sector leadership. I think sector leadership will be evident only once a strong bull run starts and for that to happen we need the current bear market to run its course. In bull run most stocks will run to varying degrees but the sector leading the run will create the maximum and most durable wealth. As of now, it seems the darlings of previous bull market like consumer finance, micro finance, private banks etc are all taking it on the chin. Once they stop correcting, there will be sharp upmoves but they will be tradable upmoves and not secular upmoves. (atleast thats the view I hold as of now. ) From among these sectors also big winners can emerge but from a sector that has lost market fancy its difficult to exactly pinpoint which company/companies are going to be the winners.

I think this pandemic will change a lot of business landscapes and we need to be patient enough to see how things pan out. In the meanwhile if we get no brainer bargains, it might make sense to buy but one has to be absolutely sure.