@rahgrov Textile sector companies usually move in tandem during an upmove. So ideal thing to do is to wait till we see most of the stocks bottoming out and moving up. Indocount has in past made some serious mistakes and recovered to be a multibagger. Now it seems it is again in market’s bad books. Not too much idea about finer details about indocount. But trident seems to be reporting good numbers. The concern in this sector could be trade wars and tariffs between India and US.

Thank you for this great and precise advice. I was doing the same mistake that you pointed out and was thinking that company is very cheap at around 4-5 p/e. But then this happens to be a case of low pe and high earnings, which Peter Lynch has told to be end of cycle. Thanks once again.

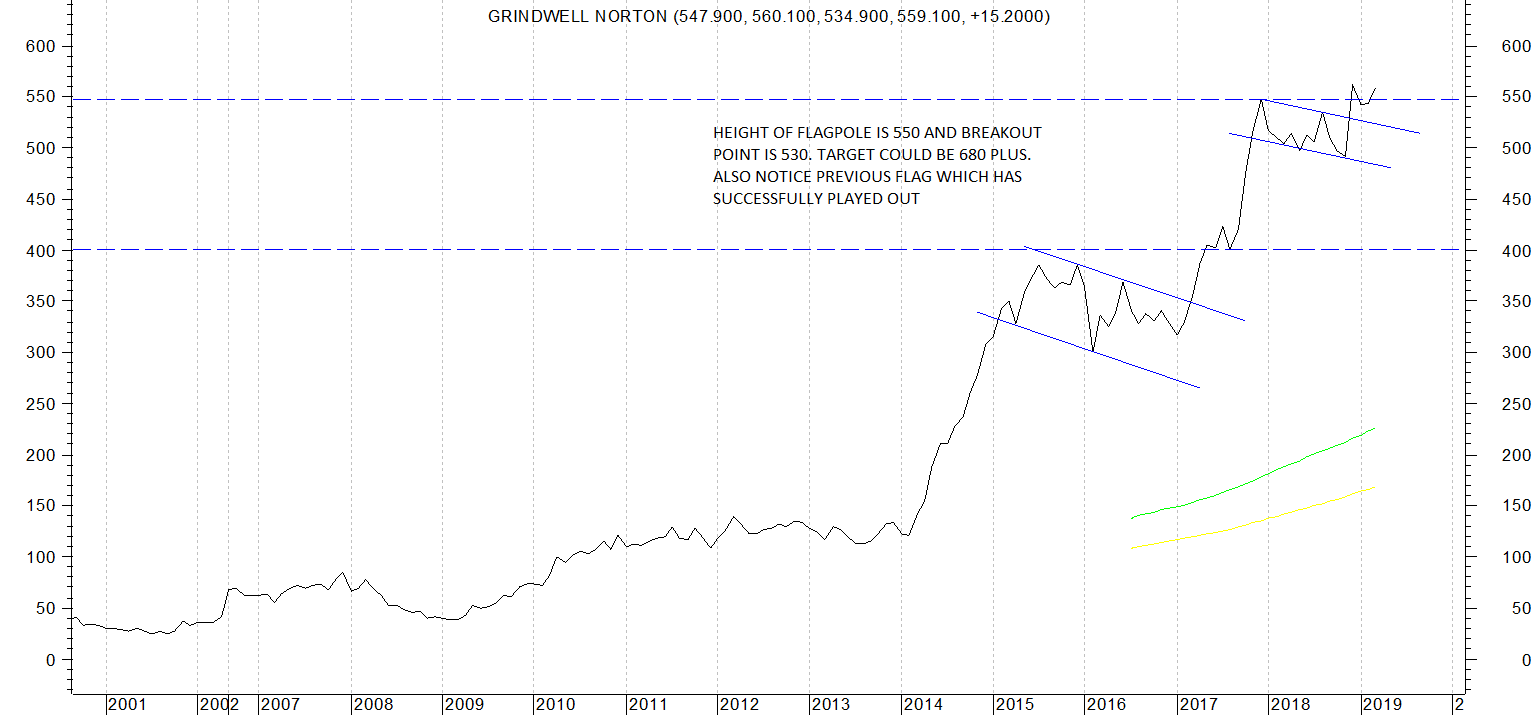

Curious now what made you consider Grindwell, Their sales, profitability growth numbers are in single digits, Plus point is that its a zero debt company. Would be great to understand your views.

Grindwell was one stock which did not buckle under the small midcap onslaught all during the past few months. I noticed it because of its relative strength compared to markets. And on the monthly charts it was forming a flag pattern with a possiblility of 25-30% upside atleast. In markets where you are scared to buy anything because of fear of stocks getting battered, here was a solid company with MNC promoters with very little volatility that offered good risk reward potential. It seemed like a good techno funda combination on longer term monthly or weekly charts.

The drawback with this kind of situation is that in absence of growth triggers, one cannot allocate a high enough part of portfolio to this company. Plus valuation wise its not exactly cheap but sometimes looking only at PE is not the right way to look at things. If somehow the company can show decent growth for next few quarters (and its quite possible with capex revival and infra boom ) there can be decent returns.

After a brief correction to the 505-515 levels the stock price has quickly bounced back to 550 plus levels. Volumes also seem to be picking up. Lets see how this one plays out.

As said before apollo hospital remains a sector leader in the healthcare sector. But healthcare sector is plagued by multiple issues

Asset heavy because of infrastructure, instruments etc needed to set it up. Some like HCG have gotten around this by having rental/lease arrangements with property owners.

Working cap intensive because most patients come with mediclaim policies and payment happens after few weeks/months.

Attrition. Its often difficult to retain the best drs as they are often lured away by higher packages.

And finally most important, govt interventions where govt has resorted to cap prices of devices etc and procedures.

Against all these risks the runway for growth is very longand a lot of PE type of guys are ready to invest big money in the sector.

Technically apollo hospital chsrt seems interesting with stock price breaking above a medium term falling channel.

Thanks for the insights…what should minority investors do in such a sector where on one hand runway for growth is huge, sector is not cyclical but structural…when is right time to invest and with what horizon? PE investors play musical chair and usually exit with their target returns in few years irrespective of what stock price remains… Thanks

Are you tracking company hester bioscience company is into animal and poultry vaccine and topline,bottom line from last 7-8 year is growing very well and can we assign pe multiple of 27 to this growing company

Dear Sir,

Your views on Indian toners and developers. The company is having good past track record in terms of ROCE /ROE. Also available at cheap valuation. The product of the company is repeatative and demand will always be there.

Do you track Mayur uniquoters ? Thanks

Hi Hiteshbhai,

1 Stock picking is more an art than a science and your explanation of equity investing definitely makes it look like an art . I have been guilty of overdoing dcf and missing several oppurtunities .

Just focus on quantitative aspects i feel may lead to investing in value traps . To what extent and till what steps, should one do the financial analysis and not overdo it and instead focus on qualitative aspects . Would request your views on the same and how to avoid such over financial analysis and focus more on qualitative over quantitative factors ?What approach/factors to be considered to make investing more like an art ?

In many cases, i have observed from your posts that you know which factors are decisive for investment and which can be ignored ? How to know which factors can be considered and which can be ignored ? As an example in one of your post you mentioned maggi issue in nestle . I wrongly thought that it was a major risk at that time for nestle as it was a major revenue source for nestle . Eventually it turned out to be not a major issue ( and even at that time after correction, my dcf valuation incorrectly showed nestle as overvalued )How to determine that this factor is not significant at the time of the issue ?

I personally have changed my view that dcf is not that important but size of oppurtunity is important and growth . Am i correct in concluding that ?

2 could you please describe any resource on behavioural aspect of investing and how do you manage the drawdown in stock prices in mid and small caps and at what point should one sell in order to not sell too early missing out on the whole stock run ? There is a incorrect view IMHO amongst some novice investors like me that as soon as a stock doubles, 50 percent must be sold to make it free and reduce risk . But the dilemma here is how to decide the maximum price to sell ? What are indicators of end of bull market cycle ?

Many Thanks Hiteshbhai

Sir @hitesh2710

1)Which business newspaper you read and will recommend

2)your recommendations for business magazines and journals

3)your recommendations for websites

4)your recommendations for daily,weekly,monthly reading materials for investment basis

5)How to track rising trends like paper trend,heg graphite trend etc

6) any paid subscription recommendations

thank you @hitesh2710, I hold HCG and it makes up 7% of my PF, I was wondering if it makes sense to continue to hold or switch to Apollo or exit the sector altogether based on your commentary of the sector.

Investment rationale for holding HCG - asset light due to their ability to get the leasing model working and their strategy to partner with leading doctors in region to start new hubs than hire doctors to run the facility.

Thanks in advance.

Hester bio is a unique company operating in the animal healthcare space. It has shown very good growth since past many quarters and according to concall it seems stepping stones for next leg of growth are also lined up with proposed expansion in Tanzania and stake in Texas Lifesciences. Although the Nepal plant has not lived up to expectations, the company still has managed to show decent growth. In the concall the management seems quite confident about growth in future also.

I had a tracking position in the company but because of very poor liquidity could not build up a sufficient enough position and now it seems the stock price is taking off.

Valuationwise it has never been too cheap and currently also it seems fairly priced. It looks like a good company to buy on declines if and when they happen for whatever reason ( barring something structurally wrong with the company.)

The problem about trying to learn and master an art is about getting carried away with it and trying to use it everywhere. We have the famous Mark Twain quote " To a man with a hammer everything looks like a nail. " Similarly with anything we know very well or anything we have learnt new, the urge is to try to apply it wherever possible and sometimes wherever its not advisable.

For a surgeon the most important thing to know is when not to operate. Similarly for us who know or are good at one discipline of investing, its very important to know its limitations. Trying to apply DCF where it is not applicable e.g in lumpy businesses or unpredictable businesses is often fatal. Similarly trying to apply patterns that work during bull markets during bear markets is likely to fail.

We have to be open to the idea of applying different disciplines of investing to the same idea. If in some idea, the charts, fundamentals, scuttlebutt etc all fall together there is higher chance of success.

Regarding drawdown in stock prices after buying I find that if stock prices go down along with general market corrections i am okay with it. Besides if the investment thesis I have in a company continues to play out I am not too worried. But if results do not come through as expected, I usually exit. Letting winners run is a thing that comes with experience.

Thank you so much Hiteshbhai for so simply explaining as always the qualitative aspect of investing .

Hitesh bhai ,I dont have any idea of technicals . Whats the best resource to learn technicals so that it can help me along with my fundamental analysis for determining entry point .

Many thanks

)How to determine that this factor is not significant at the time of the issue ?

)How to determine that this factor is not significant at the time of the issue ?