IBHF has RoE of over 30% but P/B is much lower compared to bajaj finance and kotak. P/B is like beauty eyes in the eye of the beholder.

Mkt does not look at only ROE to come up with higher P/b it also looks at risks in the book, quality of lending, ALM, nature of business, management past records and decisions before assigning higher p/b. IBHF management is shareholder friendly with such ROE but mkt sees risk in nature of lending and such high growth which could make npa look optically smaller. Higher growth in real estate is much riskier than higher growth in retail or corporate credit. As you mentioned banking is a leveraged business. How much risk adjusted returns I get on a comparable leverage between 2 similar banks makes a better shareholder returns in long term.

price to book and price to earnings in isolation dont mean much. We have to take into context

ROA and ROE of the company.

The quality of portfolio. Kind of asset quality over the years

Opportunity size and competition for the company. Will the company be able to have a really long runway for growth.

Management quality and promoter pedigree.

Demonstrated track record.

For a company which has compounded its topline and bottomline over last 10 years at a scorching pace and all the above boxes ticked, one cannot value it on conventional parameters.

I would suggest you to listen to a recent interview of Mr Bharat Shah talking about long term investing. It should be available on youtube. Interview taken by sourabh mukherjee (ambit fame). There he talks about paying up for franchises like gruh with explanation.

I dont know much about delta corp or about the gaming industry in general. I see govt interference as a big risk in this business and hence keeping away.

@newone I have never invested in unlisted space. You can go through @Anant presentation on the subject which he made in first VP meet at Goa.

Here no dliution has to be looked at in an inverted way. What if gruh dilutes at such a high price to book.? The obvious thing is that book value post dilution would go up drastically and the price to book ratio would come down. So for financial companies not diluting frequently there’s a premium attached to valuations provided performance has been good and consistent.

Hi @hitesh2710 - I just read the Mark Minervini book ( thanks to the mention by you) and planning to experiment with his method. Question for you - If you implement his process, how do you go about selecting companies ? Look for technicals first ( 52 weeks highs, 50 day ema above 150 above 200, etc) and then narrow down into potential candidates and look into each ones’ fundamentals… or screen fundamentals ( wrt earnings, sales and margin growths, management quality) and then shortlist candidates for technical analysis of stage 2 etc…

The ideal thing to do is to first prepare a list of fundamentally good cos with strong business momentum. And then wait for the technical picture to play out and take a call.

Hi Hiteshji,

What is your view on KarnatakaBank? With asset cleanup and recent crash to Rs 100, the stock is available for a Price to Book of 0.56

Also kindly let me know your views on EquitasHoldings? They recently did some changes so that there is less exposure to microfinance.

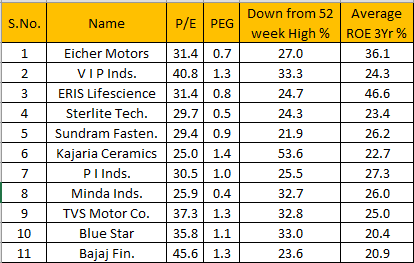

Want your views on utility of PEG ratio. Its a very simple ratio, not very complex. IMO, it captures Price vs Growth in a good way. If we use additional filters for good efficiency ratios then screener throws up some interesting names, for further research. Especially in such times of market correction, we can pick some good names with future growth story intact. Whats your view on the below portfolio.

Query

Price to Earning >25 AND

PEG Ratio <1.5 AND

PEG Ratio >0 AND

Market Capitalization >5000 AND

Average return on equity 3Years >20

PEG ratio can be a good starting point to look out for growth stocks. But one needs to be careful about the change in the fortunes of a company . e.g A company growing at say 20-30% cagr for say 4-6 years hits a road block suddenly. The PEG ratio would look very good but the growth in near future looks bleak. In such sceanrio one needs to be careful.

Having said that it serves as a very good tool to screen out good companies to work on and do a deeper dive.

Just to give an example one of my screens provided the name of Oceana Biotek. Reading the first few pages of the annual report gave me an aha moment. And going on to read the auditor observations and management response gave me the creeps.

But amongst the list you have put up I think companies like eris, sund fasteners, pi inds, minda inds, bajaj fin and sterlite tech look interesting atleast to do a deeper dive.

Eicher motors seems to be slowing down as I think the base was getting too big and after a point its difficult for companies to maintain scorching growth rates unless its a company with huge opportunity size.

I dont know the details of how much percentage pledging has been done. Besides looking at the sterlite group I wont attach too much importance to the pledging if all other things are in place.

@shyamutty I dont track karnataka bank. I have put up my views on equitas earlier while I had decided to invest in equitas. Post that due to the headwinds I saw in the sector I had booked out of the company but it remains in my radar.

@hitesh2710 Hiteshji, As Sarthak posted, thank you for being generous in sharing your experience and guidance to novices and others in this forum.

You and many other VP veterans used to track seed companies. I was looking at Kaveri Seeds, Nath Bio-genes and JK Agri Genetics. Out of them while going through recent ARs I think Nath Bio-genes going through some changes in positive direction as R&D efforts are bearing fruit and they are revamping marketing. AR commentary looks positive. I can see it sells to historical PB and cheaper compared other two after the recent correction.

But the thread on it in VP do not have any recent attention, left abandoned for 4 years and that may be indicative of red flags. My notes from AR updated on the thread, but I could not get any comments, positive or negative. Historically this company was considered as low management quality one as it took almost 10 years relist.

Since my experience in markets are very limited, what’s your view on this company and especially the management quality ? This is part of my exercise to review my holdings based MQ and your views would be greatly appreciated.

I dont track Nath Biogenes specifically so not much idea about it as a business or its management quality.

If you are following it closely then you need to go through management communication since past few years be it through annual reports, presentations or concalls, tv interviews etc and then take a call on MQ.

How safe is a fixed deposit in the small finance banks compared to a Public or Private sector banks. I am asking for amounts around 10 lacs since uptil one lac is insured by RBI.

I seem to be addicted to checking stock prices (of companies I am holding or interested in) atleast twice a day! Since you are a doctor as well, could you suggest how I could try to overcome this addiction

Regarding safety of fixed deposits with small finance banks I dont have much idea. But the difference between fixed deposits in good quality private banks and the SFB should not amount to more than 1% or so. In such a scenario why should one take any kind of risk with SFB. There is another interesting instrument Indigrid Invit which quotes at around 90 or so and gives out Rs 12 as payout which amounts to a more than 13% yield. Promoted by Sterlite group it seems to be a steady company. And there is good liquidity also in the instrument.

About checking stock prices 2-3 times a day there is nothing unusual about that. The cliched answer is to look at business performance of the company and not focus on quotes but in these volatile times some times one gets the urge to check the quotes. Regarding my being a doctor I am a dermatologist and not a psychiatrist. I can treat the itch but not the urge.