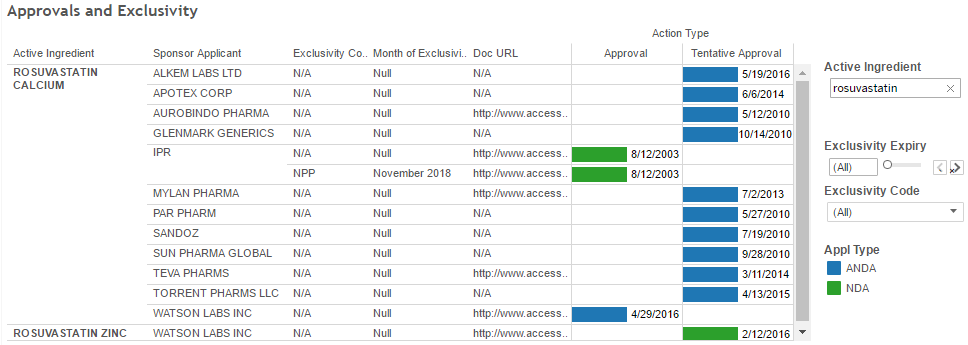

Based on the above, Watson labs has got the 180 day exclusivity.

Above information can be retrieved from FDA portal or from the below dashboard.https://public.tableau.com/profile/vishnu1702#!/vizhome/ValuePickrDrugsFDADashboard/Dashboard1

For more details, lookup the following thread:

Updated the Drugs@FDA dashboard with the data-set as of April 13th.

Couple of enhancements:

Converted “exclusivity month” filter as a slider with each step/slide interval of 1 month. Alternatively one can use the auto-suggest search option and specify the relevant date in MMM YYYY format (eg: March 2017).

Rest of the text box filters are Wildcard match-based filters. (just FYI… for new users)

Exclusivity code is a multivalue list drop-down. NCE and ODE are the relevant codes for estima…

11 Likes