Thanks @asarda

What should be the reason for sudden resignation of Mr. Dhirup? I believe that was not planned hence do you think performance of ex MD can be the reason?

Also how you rate profile of new MD - CEO Mr Akshat Seth?

Thanks in advance.

Thanks @asarda

What should be the reason for sudden resignation of Mr. Dhirup? I believe that was not planned hence do you think performance of ex MD can be the reason?

Also how you rate profile of new MD - CEO Mr Akshat Seth?

Thanks in advance.

Hello @Deven ,

I do not know the reason regarding the departure of Mr. Dhirup. The global scenario for the company is not very favourable. The availability and the cost of MDF/HDF was a big issue and the fibre cost was also very high. I think the best way to know about this is to wait for the Q3 con-call. The company is very candid about the operations to its investors. The disclosure is amazing.

This is the latest con-call report - HIL Limited (HIL) Q4 FY23 Earnings Concall Transcript | AlphaStreet

The bottom-line is that the worst is behind them and they will perform better in FY24.

Q1 FY 24

BUSINESS

HIL has reported a revenue of Rs. 1,016 crores, with a PBT of Rs. 74 crores.EBITDA for the quarter stood at Rs. 91 crores as compared to Rs. 137 crores

Roofing Solutions business grew by 4% year-on-year to Rs. 466 crores.Higher fiber cost relative to Q1 last year has negatively impacted margins in this segment.

Building Solutions business grew by 8% year-on-year during Q1 FY24, coming in at Rs. 134 crores.Revenue and profits were negatively impacted on account of the ongoing strike at Chennai. FastBuild’ business has been instrumental in augmenting our volumes.Building Solutions perspective, we had mentioned that the revenue is about Rs. 134 crores, of which Rs. 77 crores come from Blocks and the rest comes from Panels and Boards. Ebidta margins for blocks will be in the 10% range. For the rest, it’s more in the 20% range.

Polymer Solutions business, de-grew by 16% year-on-year on a revenue basis to Rs. 120 crores, 17% year-on-year growth in volumes of Pipes and Fittings, With the recent commissioning of the state-of-the-art multilayer Foam Core production line, we are amongst only a handful of players that offer underground drainage products.Big segment of Agri pipes, which is typically high volume, lower margin where we do not play.

The Flooring Solutions that is Parador business de-grew by 20% year-on-year and stood at Rs. 294 crores in quarter.

David Bradham, who we call Neel, as the CEO of Parador

Present at nearly 20,000 outlets across the country and cover more than 60% of Tehsils in the country.

We grew Mr. Ajay Kapadia has stepped into the role of Chief Financial Officer,

Capacity Utilisation- Blocks and Roofing, we are in the high 90%,Panels and Boards is at about 80%, rest of the segments are about 70%. We expect to double our size in each one of them in the next three-odd years.

The new product line is on Construction Chemicals, where we feel we have just about started, and the growth potential is tremendous.

Quarter 1 from a Roofing point of view is the most pronounced quarter.Q2 slightly softer.

Order book of nearly EUR 75 million, which is today about 25%, 30% of our total business Commercial.

Capex- 150 crores this year.

The Made-in-Germany tag that we carry the brand is known.

MANAGEMENT GUIDANCE

Parador a EUR 500 million-plus global brand over the next three years to four years.

First growth drivers are to open up key markets in North America, Middle East and Asia.

Second area of growth will come from a more solid coverage of the commercial segment.

Third area of growth is quality and innovation in products and design, and creating product lines, which can help command a price premium.

Planned capacity expansions in Golan, Jhajjar and Hyderabad come on stream in quarter 2.

Early teens, so 12% to 14% would be the first milestone for us to hit.

Q3 onwards is where we expect normal service to resume, we should start seeing the trend reversing in that period.

RISK

Mr. Saikat Mukhopadhyay anothe CFO has left the company in less than a year.

Higher fiber cost relative to Q1 last year has negatively impacted margins in this segment

Revenue and profits were negatively impacted in the Building solution segment due to the ongoing strike at Chennai.

Our expectation is it will take anywhere between six months to nine months for it to fully absorb the high fibre price increase of 22% to 24% which is going to stay as Russia is not supplying and everyone has flocked to Brazil.

We’ve seen a period of high inflation, now followed by a period of high interest rates. And that has led to subdued consumer sentiment, which is playing out also in the Construction segment and so on.

There are very few sources of fiber globally. And most of those sources are also in geopolitically volatile geographies of the world. And hence, continued uncertainty in that segment.

30% of the business or revenue is coming from Roofing, but our profitability is still highly dependent upon Roofing.

Good note. Really liked the insights. I have two queries, if you can provide some inputs will be helpful:

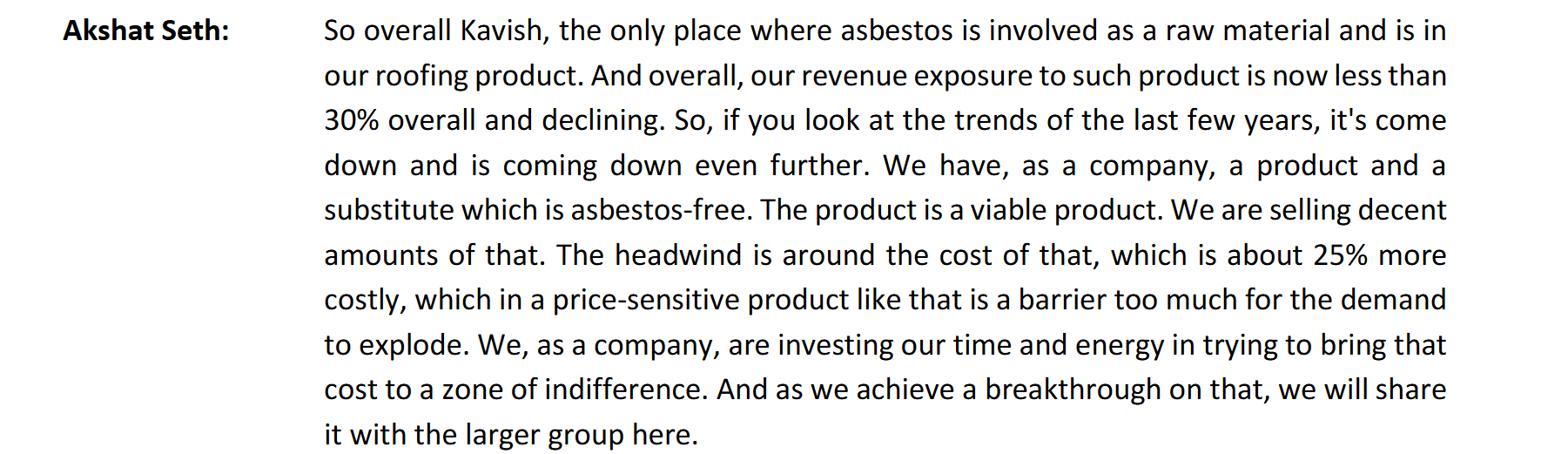

What %age of their roofing business is Asbestos based. Also in case asbestos gets banned, how do you feel it will impact HIL?

HIL is into 4 different broad segments. For the company of their size, do they run the risk of spreading too thin. What are your views on the same?

This was addressed in one of the post earnings interactions last year. Majority of the roofing business is asbestos based. They didn’t see this to be an immediate threat, as in rural sector - there are no other alternative products available which are as cost effective, with high durability and high longevity. However they are the only company which has a strong non-asbestos based roofing product (Fortune brand). WIth some more cost efficiencies, they intend to make it most cost competitive and would be positioning it as the replacement for asbestos based product. So should not impact as much.

Flooring, Polymer and Building solutions business were newer businesses and meant to have a higher growth rate as compared to the legacy business. Also its in line with their aim to becoming a 'One stop solution; provider.

However the downside in such cases is managing the supply chain for multiple businesses and ensuring raw material availability, etc. In case of a unforeseen geopolitical event causing raw material scarcity, can result in headwinds for the business. Something which impacted the flooring business last year.

totally agree with karthi plus i see it as adding growth triggers as they are diversifying into building material products not into other area. 30% of income come from roofing out of which fortune which is non asbestos sheets are very low in single digit but growing fast.

HIL LTD Q4FY24 CONS

NET LOSS OF 0.11 CR VS 4.6 CR PROFIT (YOY), Q3 7 CR LOSS

REVENUE 852 CR VS 863 CR ( YOY), Q3 784CR

EBITDA 17 CR VS 37 CR (YOY), Q3 2 CR

EBITDA MARGIN 2% VS 0.37% (YOY), Q3 2%

Bottom line affected due to 158.44 cr worth they purchase share in

Crcstia Polytcch Private Limited,

Topline lndusuies Private Limited,

Aditya Polytechnic Private Limited,

Sainath Polymers,

Aditya Industries

CO RECOMMEDNED DIVIDEND 22.5 RS PER SHARE

Need to listen the concall now to get more understanding on the outlook moving ahead, Anyone tracking this company in the forum?

Financial Performance:

Operational Performance:

Future Outlook:

Concerns:

Other Points:

I believe the next 2-3 quarters will be very important or a key deciding factor to see if management is able to execute it as expected or not.

Key Concern: The company is in to a competitive business segments so the only thing to watch is execution of management as per guidance and there are too many variables in this business to let it move as per expectations.

MD/CEO trying for 8% net profit as remuneration is a bit too much, dont u think?

The below is from latest Annual report.

During the financial year 2023-24, the overall managerial remuneration paid/ payable to Mr. Akshat Seth, Managing Director & CEO exceeds the limits stipulated under the provisions of section 197 of the Act, i.e., 5% of the net profits of the Company, calculated as per Section 198 of the Act. The Board in its meeting held on May 7, 2024 has proposed to increase limit of the managerial remuneration in excess of 5% of the net profits of the Company, calculated as per Section 198 of the Act, up to a limit of 8% of the net profits of the Company, for the financial year 2023-24, subject to approval of shareholders.

I understand that the salary might be higher than usual, but in small companies where profits can be unpredictable or sometimes when below normal levels, it’s common to see elevated salaries when the company is aiming for significant growth. To lead the company through a successful turnaround and drive it onto a structural growth trajectory, hiring a strong MD & CEO is crucial. This often comes with a higher salary, which is acceptable because it reflects the value they bring to the company. It’s preferable to see a substantial salary for the CEO rather than having funds diverted through other means, which could present a misleading picture to shareholders. I mean this is my perspective to look at this may be this may not be same for everyone. As an investor we should keep an holistic approach while looking over these issues.

Nothing wrong with a CEOs taking very high salaries and they deserve them when their companies are performing well. But CEOs of high ethics and integrity, put their skin in the game by taking a hit on their compensation when company is struggling.

A CEO continuing to draw high salary during bad times is akin to telling the investors that CEO is not accountable and board either is not doing its job or it’s too weak against promoter and CEO nexus.

Also higher salaries to CEO doesn’t mean that a company could not be diverting funds through other means. It’s not binary. If you need proof, look at Enron.

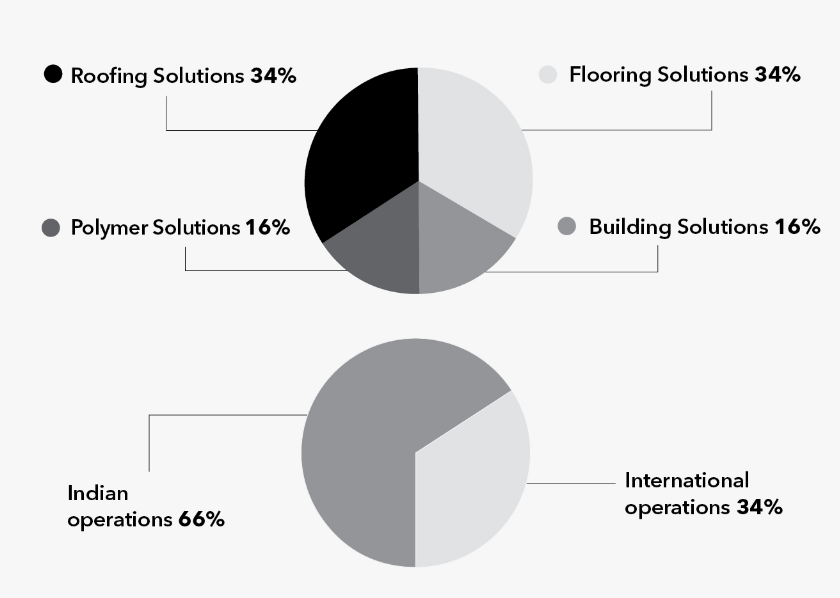

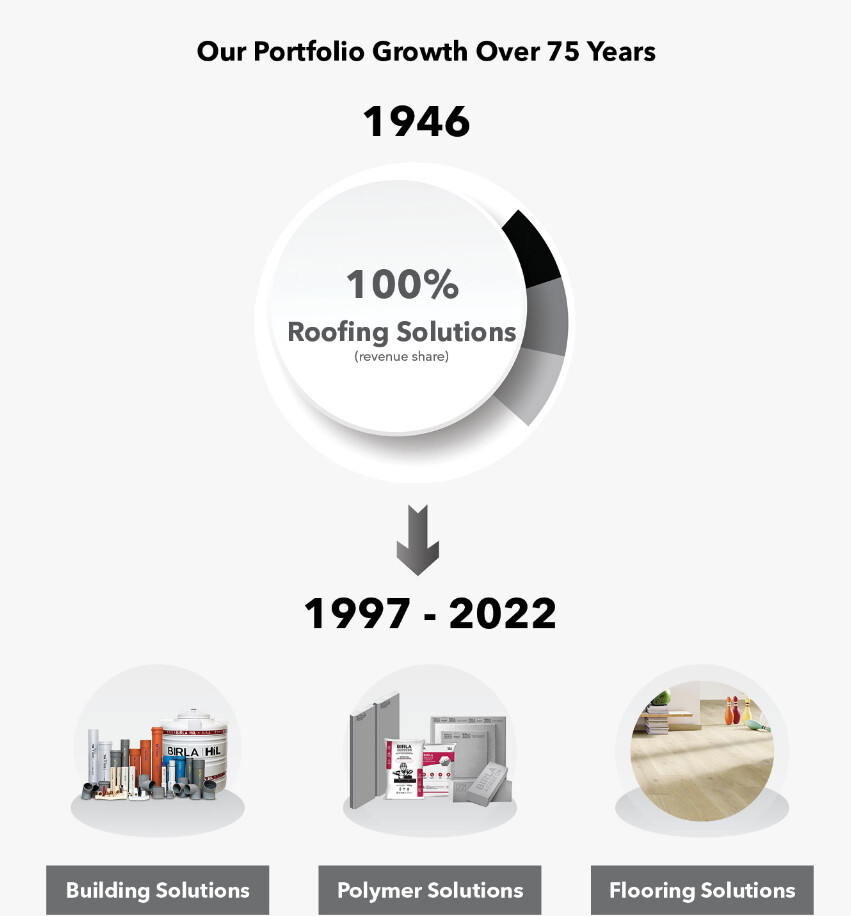

HIL Limited, a C.K. Birla Group company headquartered in Hyderabad, has a legacy of over 75 years in the home and building solutions industry. HIL operates 32 manufacturing facilities globally, including plants in Austria and Germany. It serves its market through an extensive distribution network of over 3,500 distributors and 21,000+ retailers.

Operating across four key segments—Roofing Solutions, Polymer Solutions, Building Solutions, and Flooring Solutions (Germany)—HIL has recently expanded into Construction Chemicals.

HIL used to be a roofing solution company, its flagship roofing brand, Charminar, carries a legacy of over 75 years of trust in the Indian market. Under this segment, HIL offers a diverse range of fiber cement products. However, a key raw material, asbestos (Chrysotile fiber), faces supply constraints due to mining bans in most countries, driven by serious health risks. This has resulted in limited global supply and supplier concentration risks.

Thus HIL used the cashflows from its roofing solution business to acquire other businesses and diversify its portfolio from highly competitive roofing solution business. Additionally, it has introduced non-asbestos-based fiber cement sheets, using synthetic fibers as a substitute while capitalizing on the strong reputation of its existing brand. Thus it is transforming itself from a roofing solution provider to a one stop home and building solution provider.

Key Acquisitions by the company:

HIL’s businesses:

Roofing Solutions:

HIL is a dominant player in the domestic asbestos Fiber Cement roofing segment with

24.7% market share. It currently contributes around 30% to the total revenue, they want to further reduce it, thus have developed an alternative non-asbestos based fiber cement sheet. They have a network of 11,000 stores, which they are leveraging to sell adjacent products such as color-coated sheets, ultra-cool sheets, and roofing accessories. It has 6 manufacturing facilities and a cumulative manufacturing capacity of 1.17 million of fibre cement sheets p.a.

Key Products:

The industry has experienced a 10% decline due to the rural slowdown. High competitive intensity, coupled with rising raw material prices, has further pressured margins, which have collapsed due to the lack of pricing power. Also cement prices are expected to increase from Q4, as indicated by the management.

New BIS (Bureau of Indian Standards) quality norms for asbestos or fiber cement-based products could reduce unorganised competition.

The industry’s expansion of capacity inspite of low margins may suggest strong future demand or indicate that competition is becoming increasingly irrational.

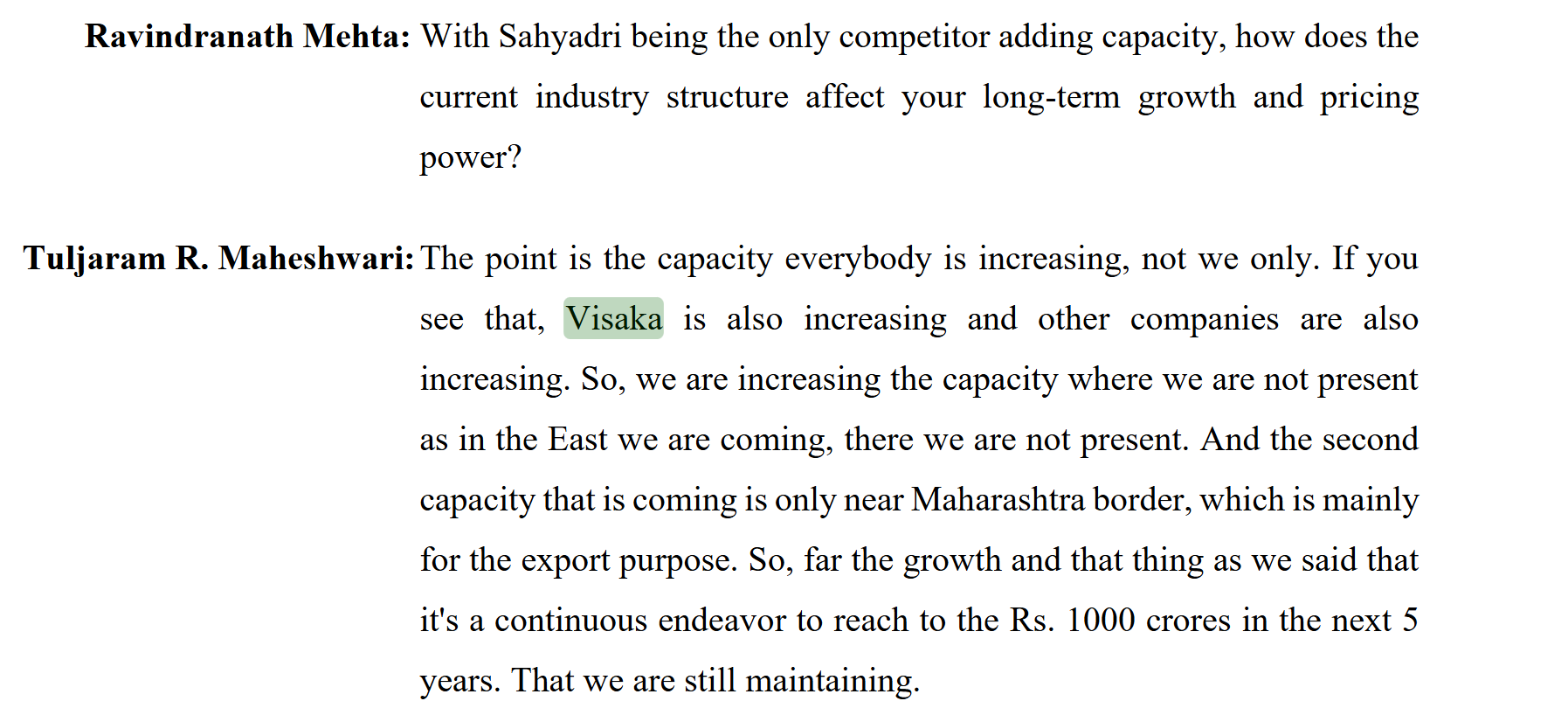

Source: Sahyadri concall

Historically, Sahyadri has achieved an OPM (Operating Profit Margin) of 6-24% and Visaka 6-17% between FY13 and FY24. However, in Q2 FY25, Sahyadri reported an OPM of -2%, and Visaka achieved just 1%. Despite the high competitive intensity in the industry, I anticipate that margins are bottoming out, with a gradual recovery expected from H2 FY25.

Building Solutions:

Birla Aerocon is India’s leading green building solutions brand, offering both dry & wet walling solutions. The portfolio includes AAC blocks, panels, fibre cement boards, sandwich panels, ready mix plaster, block jointing mortar and panel jointing compounds. It currently contributes around 16% to total revenue.

It has 9 manufacturing facilities. The Cumulative capacity of various products is as follows -

Blocks – 1,1 million CuM

Boards & Panels: 2.3 lakh MT

Key Products:

They have been actively working on cost optimization and have successfully reduced costs by 250 basis points, with further scope for additional reductions. Despite achieving an OPM of 5-9% between FY19 and FY24, their margins dropped to 5% in Q2 FY25 due to weak pricing. However, with the real estate upcycle and increase in construction activity in H2, I expect a gradual recovery in this division. Also its margins are not comparable to BigBloc

Management has guided to achieve 12-14% margins in the medium term for this business.

Polymer Solutions:

Key Products:

Birla HIL is the prominent brand for this segment. Currently it contributes around 16% of total revenue which should increase going forward.

HIL has strategically focused on the tiling segment within the Construction Chemicals category, they did 85 cr in sales in FY24 for their construction chemicals.

HIL emphasizes the advanced “True Colour” technology used in their putty, it has broadened its putty offerings to include variations like waterproof putty and gypsum plaster. In FY24, HIL’s Putty business faced lower-than-expected revenue, primarily due to industry-wide price reductions and increased competition. Current putty capacity is 250,000 MTPA.

After acquiring Crestia Polytech, HIL added the Topline brand in March 2024, expanding their portfolio and market presence in pipes and fittings, particularly in Eastern India. With this acquisition they have 3x their capacity to 1,15,000 MTPA. Skipper pipes has 62000 MTPA capacity and does 500 cr sales, HIL can do 800-1000 Cr sales considering 2-2.5x Asset turns.

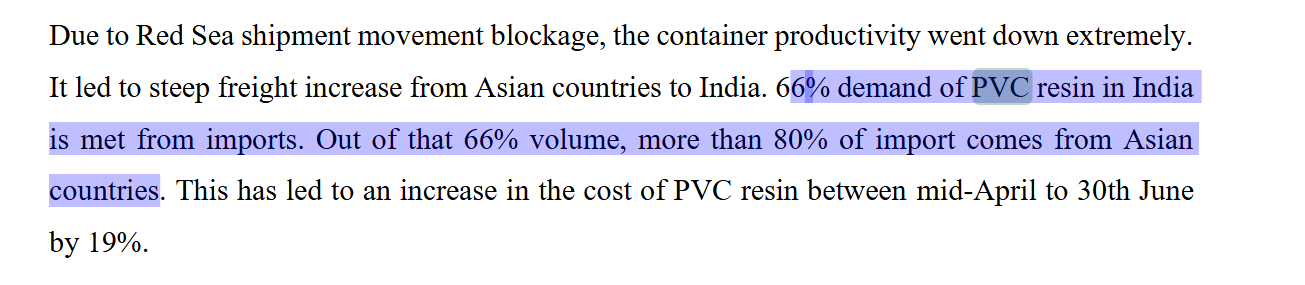

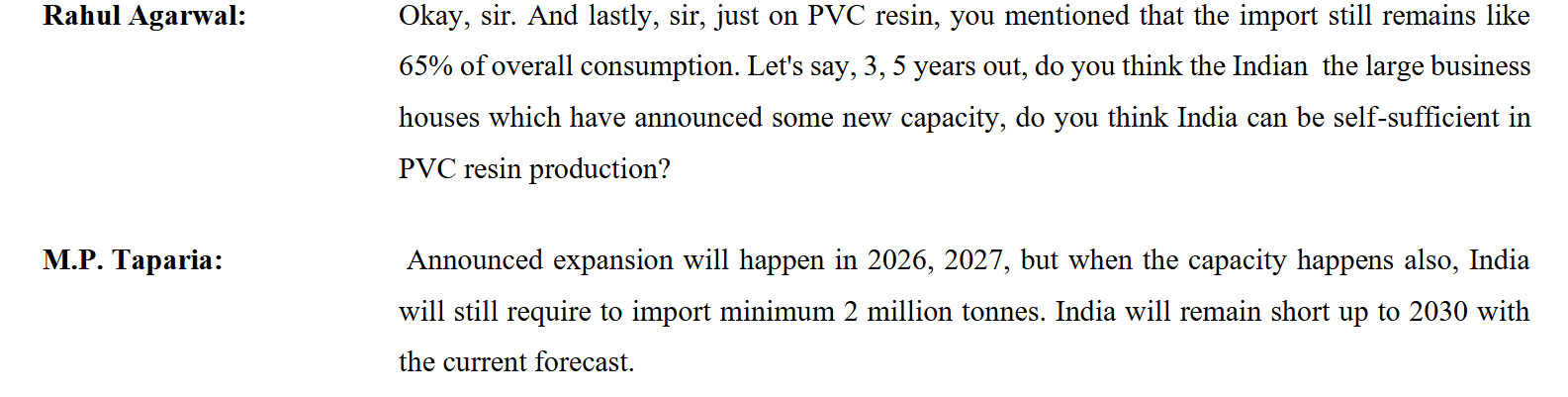

In the pipes and fittings business, PVC resin, the key raw material, has a 66% import dependency. This reliance on imports exposes the business to significant volatility in raw material costs, which can lead to inventory losses during price fluctuations.

Source: Supreme industries concall

Competitive intensity:

Prince Pipes has mentioned strong capacity addition by all players, inspite of weak margins industry is adding capacity. Apollo pipes is also planning to expand capacity to 286000 MTPA in next 18 months.

Even Skipper Pipes has struggled with terrible margins of around -2% to 4% in the pipes and fittings business over the past six years. Despite this, they aim to become the fastest-growing player in the industry, arguing that increasing scale will enable margin expansion. Prince Pipes and Birla HIL have also cited similar reasoning for their capex plans. Moreover, every player claims their technology is superior or unique, but I find it difficult to discern any significant differences between them. All of them are spending money on brand building too.

Source: Skipper AR

Currently, 35% of the industry remains unorganized. With the implementation of new BIS norms, the share of the organized market is expected to increase. Additionally, government capital expenditure under the Jal Jeevan Mission is anticipated to accelerate in H2 FY25.

Since the pipes and fittings, construction chemicals, and putty businesses are still in the growth phase, margins can be volatile. Additionally, the recent acquisition has resulted in significant one-time costs.

Flooring Solutions

HIL Limited acquired Parador at an enterprise value of €82.8 million (approximately ₹687.2 crore) in 2018.

Parador offers a diverse range of flooring solutions, including engineered wood, laminate, vinyl, and the innovative sustainable product Modular One. These products are designed to cater to both residential and commercial spaces, blending functionality with aesthetic appeal. Available in over 80 countries, Parador’s flooring solutions are widely used in the design industry and distributed through retailers, providing customers with premium-quality flooring and complementary accessories. It currently contributes around 34% to total revenue.

Parador primarily operates in the European market, with a strong presence in the DACH region (Germany, Austria, and Switzerland). In recent years, the company has experienced a significant revenue decline, largely driven by a challenging macroeconomic environment in Europe, which has led to a market contraction of around 30%. Despite this downturn, Parador has managed to increase its market share. Furthermore, the company is expanding into new regions, including North America, the Middle East, and Asia, in a bid to diversify its geographical footprint and tap into emerging opportunities.

Parador is aggressively pursuing opportunities in the commercial sales channel, which is expected to contribute to higher sales volumes and profitability in the long term.

Management has guided for EBIDTA margins of 6% in FY26 and 12% by FY27.

Premiumization play:

The management also plans to launch Parador in India, leveraging the upcycle in the premium real estate sector and positioning it as a premium offering in building materials. Parador could serve as an attractive option to capitalize on the long-term trend of premiumization in the Indian market.

Management Change at HIL:

Akshat Seth was appointed as the new Managing Director and CEO of HIL in February 2023. Prior to this role, he was the CEO of the CK Birla Group’s Healthcare Vertical and also led the growth and strategy initiatives at the CK Birla Group.

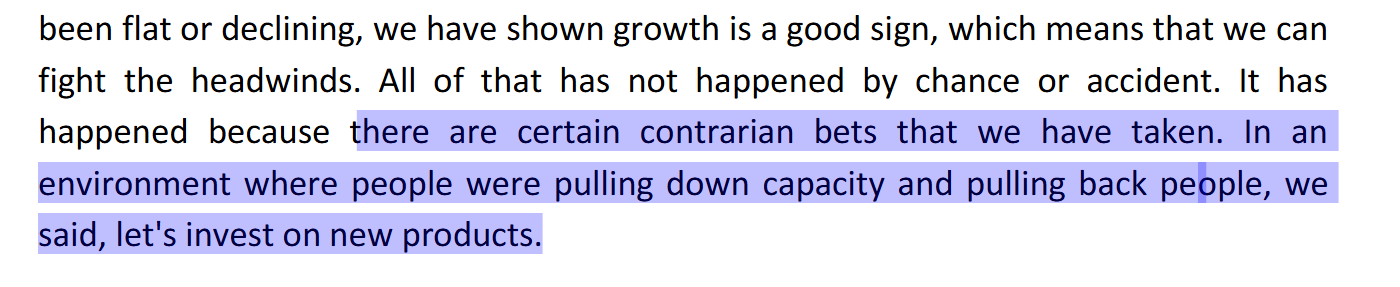

I like the management’s contrarian approach. Despite facing falling realizations and macroeconomic headwinds across all business divisions, they are still investing in new products. This gives me confidence that management views this phase as a temporary downturn and is focusing on growth by reducing costs and introducing new, margin-accretive products.

Supply Overhang for HIL:

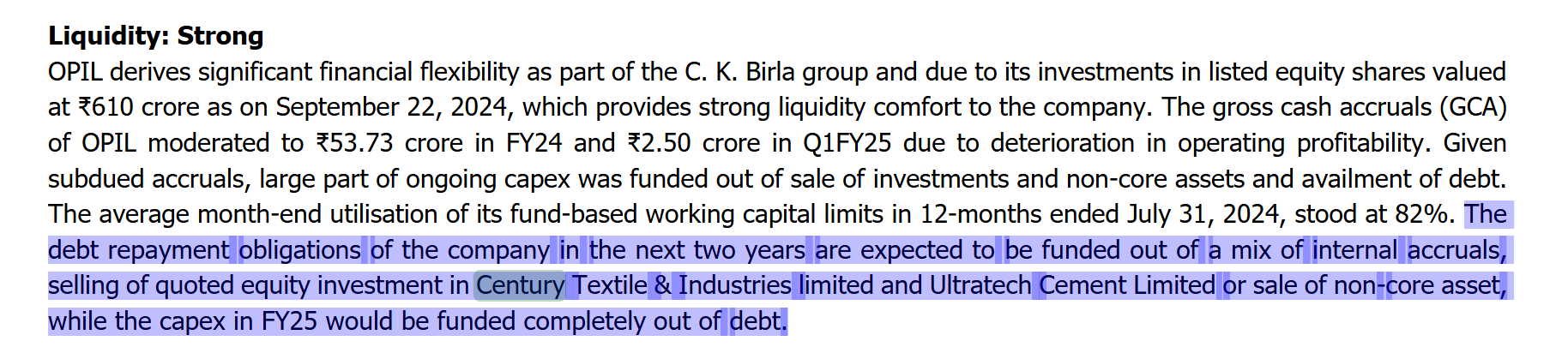

Currently Orient Paper holds 12% stake in HIL, it has certain debt obligations, capex plans and a lot of contingent liabilities too and based on its credit rating report it can dispose some of its holdings to meet its liquidity requirements.

Valuations:

Currently, HIL has an enterprise value of around ₹2,900 crore, with a price-to-book ratio of approximately 1.5 and a price-to-sales ratio of about 0.5. It’s important not to compare its current valuations to past figures, as the company has undergone significant changes in its product mix. Management has guided for sales of $1 billion (₹8,500 crore) by FY27, with expected overall margins of around 10-12%. Initially, in 2021, they had targeted $1 billion in sales by FY25, but this target was later revised to FY26 and then FY27. With new management in place, I am optimistic about their growth prospects. I believe the company is at an inflection point, and starting in H2, we can expect margin improvements. Additionally, with rate cuts expected, the real estate cycle should benefit significantly. Their transition from a roofing solutions provider to a comprehensive home and building solutions provider should also help command better multiples than in the past. I believe they could achieve ₹850 crore in EBITDA by FY28. Given that all their business divisions have been in a downturn, a recovery could be highly beneficial, and with strong cash flows, they could potentially become debt-free.

Disclosure: Hold a small tracking position

I believe if turnaround in paradoor happens this will create good wealth… presently earnings are depressed due to losses from Paradoor

Interesting interview with the Parador CEO. The guy doesn’t even refer to HIL or the Indian ownership even once. All the focus on just the German heritage. That aside, looks like they are shifting focus a bit to commercial opportunities (hotels and expensive residential projects). Also introducing a number of new products, it seems.

This analysis was quite helpful. Thank you for sharing! Have you scaled your position since you wrote this or has the industry context and demand scenario led you to change your opinion? Will be great to get your thoughts.

Major development !

CK Birla agglomerates the whole of the promoter holding in BirlaNu in his own name, buying out rest of the promoter entities! The question is Why? especially when the company is just not getting it right… All its recent to not to recent endeavours are bleeding.. the core asbestos sheet biz is also facing head winds.. profitability has all but vanished

and CK doing this..

That was quite cryptic. I am interested in understanding the motive behind this. Standard answer is to tie this all to together with succession planning. But are you intrigued with timing or do you see any other motive.

Discl : Invested

I was thinking the exact opposite. He is likely buying the business at the bottom of the cycle. It was mainly their European business (Parador) that put pressure on their margins, but it is about to rebound now that the EU has imposed anti-dumping duties on engineered wood flooring from China. This improvement was visible in the last quarter. Plus, Gemini is saying that renovation market in Germany is surging.

I think the Indian roofing business will also turn positive going forward, supported by rate cuts, the push for affordable housing, and the increased rainfall this year. Let’s see.

Was planning to enter Birlanu by March but promoter had other plans ![]() so, bought some last week and today.

so, bought some last week and today.

I have built a simple 2–3 year forward projection to estimate a potential earnings-based valuation, based on management commentary.

Key Assumptions for FY29

Revenue: Expected to double over three years - ₹7,200 crore

Operating Margin (OPM): Conservative assumption at 10% (low end of double-digit guidance)

Net Margin (NPM): ~4%, assuming 30–40% conversion of operating profit to net profit (in line with historical trends)

Revenue: ₹7,200 Cr

Operating Expenses: ₹6,480 Cr

Operating Profit: ₹720 Cr (10% OPM)

Interest, Tax & D&A: ₹432 Cr

Net Profit: ₹288 Cr (4% NPM)

With a current market capitalization of approximately ₹1,300 crore, the stock is trading at roughly 4.5x FY29 estimated earnings.

Note: These estimates are intentionally very conservative. Management has guided toward achieving $1 billion in revenue within the next two years and is targeting mid-teen operating margins. In contrast, my projections assume revenue of ₹7,200 crore and an operating margin of just 10%. Therefore, the assumptions are meaningfully below management’s stated targets, providing a conservative buffer in the valuation estimation.