Q4FY20 call notes. There could be some errors so please verify/add

2500cr revenue target in FY22 pushed to FY23.

* Adjusted for COVID, revenues would have been flat. Low utilization in April, 60% in May, 80% in June.

* Gross margin improved substantially 2-2.5%? Product mix sply in Q4, EBITDA margin improved inspite of lower sales. EBITDA margin didnt increase as much as gross margin? Fixed costs have remained same inspite of lower sales. New products and efficiency measures (costs cutting and Increasing automation) will improve margins from this year.

* EU/Japan demand to shift out of China? Higher inquiries from customers who are planning to de-risk supply chain. we have a good footprint with environment clearances in place. We will also look at improving product mix towards higher margin products. Are things really happening or is it just a story? Lot of good things are said but on-ground implementation is yet to happen.

* RM- 30-35% comes from China. Target is 20% over 2 years. There were initial issues due to logistics. Non-availability of some RMs. domestic sourcing of key RMs wherever possible

* Additional capacity in Bangalore that came in H2, started contributing. Both facilities got re-certified by the USFDA.

* 3 new DMFs in generics.

* Successfully developed API for Favipivir (for COVID) at pilot scale and currently supplying test batches to many clients. Commercialization by Sept-Oct. Difficult to guage revenue potential currently because Clinical trials are still ongoing.

* Reduced gross debt by 16cr from 661cr (FY19) to 645cr (FY20). Net debt down 48cr from 629cr to 581cr (FY20). Not opted for moratorium. WC days improved from 120 to 110, improvement of 47cr. Just in time inventory policy is gone at least for few months and customers want us to maintain stock. Net CFO before exceptional item was 219cr (FY20) vs 115cr (FY19). Adjusted CFO=204cr. FCF= 61cr(FY20) vs -12cr(FY19). We have the same debt today as we had 10 years ago but today we are 2-2.5x bigger. We are in growth stage so need capex. This business is capex intensive. Many times companies dont want to wait, they want to see free assets.

* Capex commisioning was planned for Q2/Q3, now pushed by few months to end of FY21. Already spent 158cr out of 300cr, rest to be spent in FY21. Capex will start contributing from FY22 and can get fully utilized by end of FY23. Products are already lined up, DMFs have been filed and customers have taken trial batches. Asset turns ~1.5x. Existing products will take up 40-50%, rest will be new products. We are also looking for Contract manufacturing opportunities so cant fill up the full capacities.

* Many cos have given good outlook on crop protection while Hikal Q4 was muted? There was inventory correction from some of our major customer. We expect it to be over this year. 80% of crop protection is from exports. 20% is from domestic. Growth is expected from FY22, given the COVID uncertainty this year.

* Pharma- We have legacy molecules like Gabapentin. Gross margins dont show contribution from new gen diabetes molecules. We have launched some products and are in small qty, expected big delta from FY23. Legacy molecule contribution will go down in next 3 years. US is 45-50%, EU is 20%, Japan is 10% and growing rapidly. Some new molecules in CV have big market in India and some products will be launched.

-

Pharma has 9-10 products in Custom manufacturing and 14-15 in own generics. Every year we add 1-2 in CRAMS and own. Crop protection has 11-12 in CRAMS and 5-6 own. We try to do few and try to be leaders with no 1 or 2 in those molecules.

-

Pharma CDMO Pipeline has 4-5 intermediates (which are coded so we dont know the end use, and can go in multiple products) at any time, of which 1 in phase 3 and 3 in phase 2.

-

Agrochem CDMO Pipeline has 2-3 products. These are early stage products. Commercialization in agrochem takes longer because product registrations are country by country, its not pan EU like in pharma. Generics pipeline has 1-2 products

-

32% revenue is from generics, and 68% ie 936cr from CDMO. Blended margins are only 18%. CDMO margins cant be below 25% (Suven and divis do 35-40%) so does it mean that generics margins are very low? What are margins in generics, is it 8-10%? We dont give the split. We do have some legacy molecules that are low margin so we are replacing them with higher margin products incl generics.

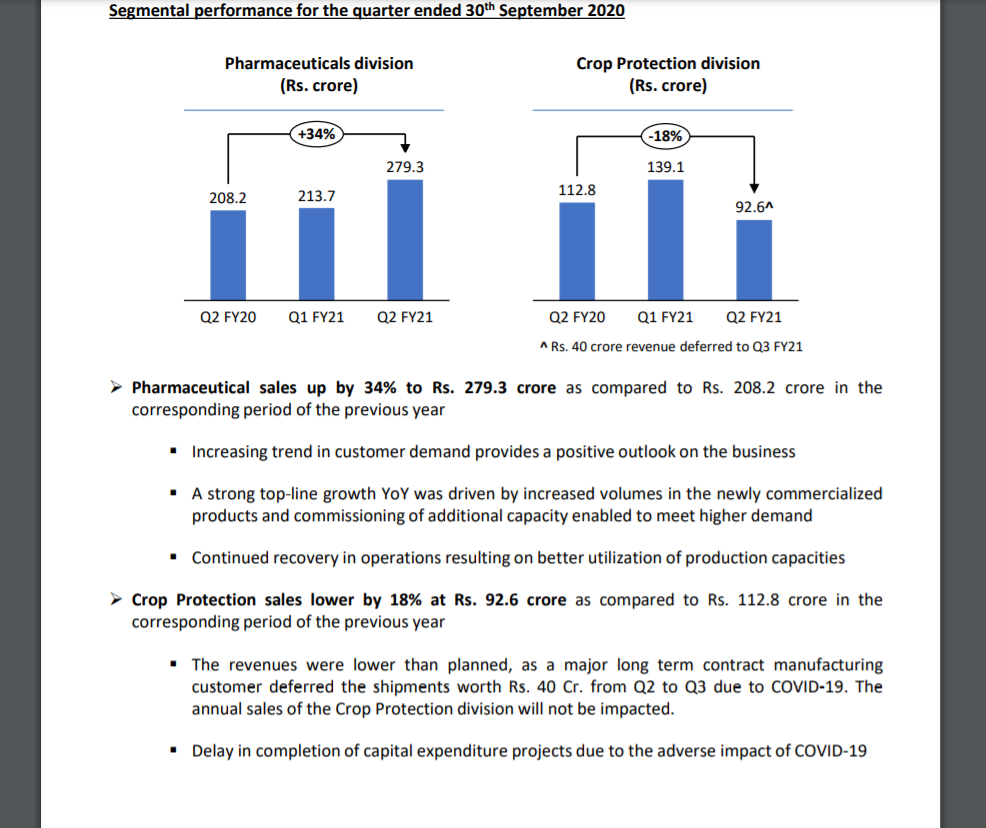

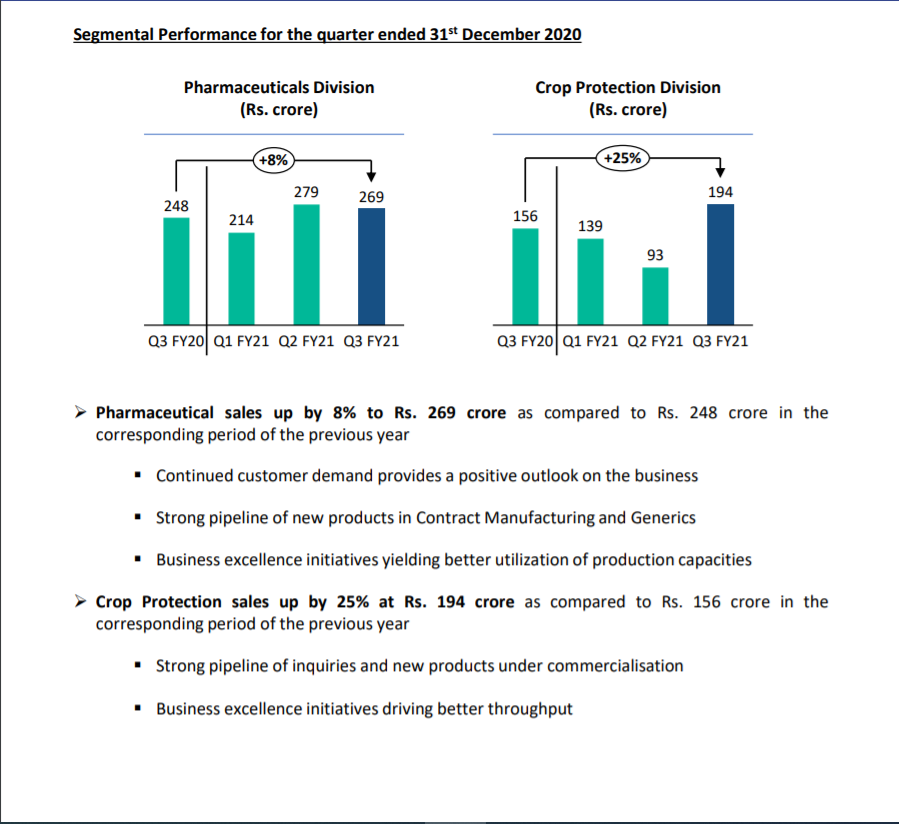

Increasing trend in customer demand provides a positive outlook on the business

Increasing trend in customer demand provides a positive outlook on the business