Calculating of Risk Premium is a science and is based on complex calculations. Actuarial science applies the mathematics of probability and statistics to define, analyze, and solve the financial implications of uncertain future events. The insurers have Acturies who do the same.

When an Insurer writes a policy they factor in the future premiums what they will be receiving from the client for the policy period. Since most of the expenses for sourcing of policy is written off during the first couple of period the remaining premium is actually income for them less of claims which they reinsure.

Again it depends on the company to decide what they perceive as a Good Risk and not so Good Risk, unlike General Insurance the Insurers are free to reinsure the risk at will. However we have seen that the insurer prefers retaining risk of smaller values on thier books and try to reinsure high value risk to the reinsurer to ensure their bottom line does not get effected by big claims, say for example if I buy a Term plan with a sum insured of Rs.5 Lacs the insurer might retain the same, but if I buy a term plan with Rs.50 Crore sum insured the Insurer might like to reinsure. It completely depends on their underwriting team.

LIC Of India has literally worked in a monopoly market for close to 50 years before 2001 when the sector was opened for private sector. So their market domination is there, and also the fact that they have a huge distribution force of agents across the country help them retain market share. Their brand still is very strong, infact in India when you want to buy a Life Insurance you say “EK LIC karana hai”

The Private players are still focussed on the Urban market and fight for the market share in there while LIC rule the rural belts. Lets not forget what happened with Air India and BSNL who were in similar situation when they had monopoly and see how are they placed now. LIC needs to reinvent the wheel to retain their position which they are doing since last few years.

Also, we must not forget one such PSU Unit Trust of India and its spectacular collapse

Millions of pensioners would invest in its Unit 64 scheme and was considered rock solid like the LIC

Well, Air India and BSNL were in businesses involving too much capital and infrastructure. Banking business suffered due to NPA on lent money. On the contrary LIC takes money from consumers. It seems highly unlikely to go the way other PSUs have gone unless there is total collapse of Finance sector in India, which is again highly unlikely. General Insurance companies may falter due to poor underwriting skills in niche area of general insurance which keep propping but LIC is a different giant alltogether.

It is really high time that private insurers should focus on rural India, which they are doing gradually. It could be that LIC has suffered from misselling of policies but still even today its every Q metrics is envious.

As an investor in Private life insurance space, LIC needs to be watched very carefully. If Private players are able to gradually corner LIC market share then we can have a great outcome. Point is, I am still not convinced if LIC would let its market share go or would rather gain more market share at cost of Private players in times to come…

I think I could not convey what I meant… to make things clear again, my mention of Air India and BSNL was to suggest how companies tend to fare when they move from a Monopoly situation to a competitive market and LIC needs to reinvent itself to continue its dominant position in the market.

However lets discuss in and around HDFC Life which is doing better than the other listed peers ie SBI Life and ICICI Prudential Life…

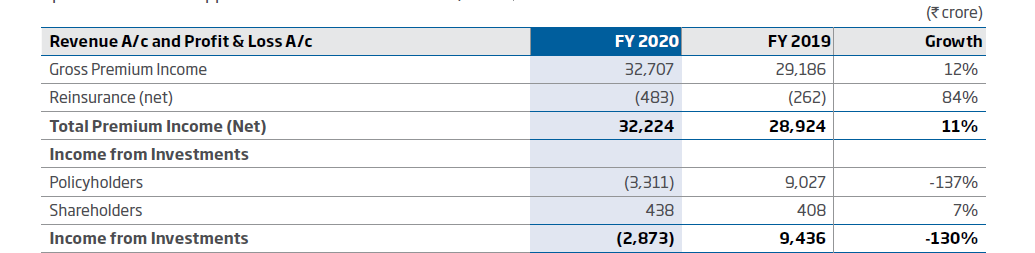

Being a complete noob in this sector, can someone please shed light as to what this severe reduction in income from investments (policyholders) actually means in complete layman terms (-137%)? Was this due to March 2020 ULIP losses ?

You can get the number from screen, every quarter the shareholding gets updated and every six month the balancesheet also gets updated. If you notice i have pasted screenshot from screener only.

Also i do track my portfolio stocks all sort of events. I have concentrated holding so no other option