MEN who are WORKING- QUALITY OF MANAGEMENT (II)

Bernard Baruch- A legend who dreamt freedom for human

Walkover investment legends Warren Buffett, George Soros or even giant speculators like Arthur Cutten, Jesse Livermore; Bernard Mannes Baruch was undoubtedly the most influential investor of all time. There is seldom any debate on this question as no one influenced five American presidents, two world wars. All major political leader of the era has once travelled in the back seat of Baruch’s Rolls Royce. Such was influence of Bernard Baruch he was awarded Army Distinguished service medal by the President then. Baruch was investor, speculator who turn to political advisory before world war which perhaps saved him from wrath of 1929 crash. Otherwise known for grand philanthropy donated 63 kilometres of land among many other things. Please do read about Bernard Baruch in case you haven’t; these kind of personality comes once in a hundreds of years.

He has wrote several books, you can find them all in Amazon. Here is link to his biography

Few very important quotes of I came across during classroom session ongoing! It may be relevant for the threads like this:

“I keep an important fact in mind that I am very unusual. You call it my biological upbringing , I like to repel my cognitive biases and that’s the basic DNA behind my career of investment.”

“I knew investment was right decision for me as I was always an individualist, never afraid to disagree with authority.”

“I want to define myself at deathbed whether I made a difference , whether I lived fully and well.”

“People don’t follow their dreams due to single fact they are afraid of falling in their endeavours. They like to follow predetermined path as they know they can achieve rather than one of their own making where they will be tested.”

“If we don’t take a certain step we don’t believe we will succeed, we have placed a barrier in front of that success that is far stronger than reality. If we try we may fail but we may succeed. If we never try at all, we make it impossible to succeed.”

“I learned more from mistakes than accomplishments, this could never have been possible without risking failure.”

“Don’t worry about how much time you have spent on a career you don’t like or how much you have invested in relationship that you know will not work. “

“It is easier to make a lot of money if you don’t really want it badly. Being wealthy doesn’t make you happy. I know. I have tried it several times. I went bust many times, it didn’t affect my life as I was sleeping in same house on same bed before and after wealth”.

These are quotes from Curtis Faith, Bernard Baruch and so on. No CAGR, no cash reserve or yield anywhere. Food for thought?

Fair, lets grind back to topic of management. Last time we said management must take decisions on five things:

- Operational efficiency

- Above the line decisions as business restructuring

- Accounts, finance and control

- Capital allocation

- Trading off rewards and risks

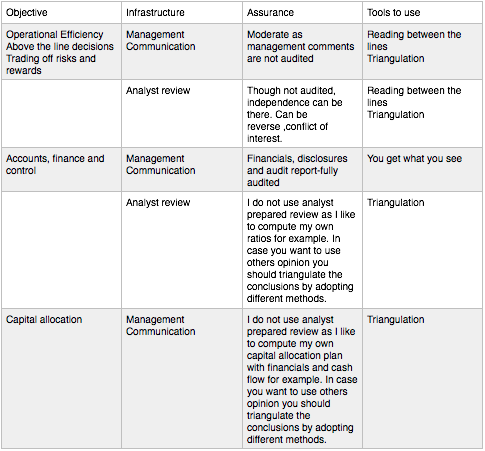

Great, how do we know all this? No matter what ever we do, we may not get all information. The idea is to draw a reasonable conclusion.

This is what I am trying to do:

- You get what you see- available crisp and clear information

- Reading between the lines- moving from literal interpretation to objective interpretation

- The triangulation technique- using different methods for checking same subject

You can only perform any of 3 activities above if something somewhere to start with, isn’t it?

- Management communication- financials, management discussions/presentation and all other communications to stock exchange.

- Analyst review and analytics- all sort of wise analyst publishing different reports on buy, sell call or even commentaries on management. Idea is to screen them not believe them.

Here is a little known secret, the second best information prepared and analysed is not available to us. These are income tax authorities, second is financiers if they are involved. Nevertheless we can do only what ever is available to us:

How to establish a relationship tools against available infrastructure, bellow is a table I use:

Rather than going a complete analysis which will take time let me pull out some specific workings and its basis here:

A. Operational efficiency

Management operational efficiency begin with published numbers, what are the ratios help you is :

Around profitability- consistent tax rate, net margin, asset turnover, ROA, financial leverage, ROE/ROIC, interest coverage

Growth- sales, operating profit, net income and EPS

Cash flow- operating cash flow growth, free cash flow growth, capex/sales, FCF/Sales, FCF/Net income

Financial health- current ratio, quick ratio, financial leverage, debt/equity

Efficiency- Cash conversion cycle with break up, fixed asset turnover, asset turnover

All these ratios are well known with detailed commentaries. The trick is level basing and interpretation.

For example take a case of level basing:

When I calculate Return on Assets I use Net Operating Profits After tax. Two major reasons it removes all below the line effects and neutralise tax rates. Second my cost of capital for valuation calculation is basis NOPAT, every margin above cost of capital is a economic profit for me.

Now interpretation:

This can be complex and easy depending on methods you are using. Say over years my assets have gone up by 45% of which 80% of increase is supported by tangible asset. This is good and bad both. Liquidation and balance sheet valuation goes up where idle asset may hit your ROA/ROE. Hence use PL and Balance sheet ratio combined for an interpretation.

B. Above the line decisions

This is a specialised area for assessment. If you are beginner my suggestion is avoid. We may need separate thread for this. You can read this book meanwhile:

C. Accounts, finance and controls

This is the most assured area as large amount of transactions are audited. The task is here to tie management discussion, financial statements and disclosures etc. For example:

In Management discussion and analysis:

Management says we feel receivables are good and recoverable. And we have not provided any provisions accordingly.

In notes to account auditor says:

An amount of XXX receivables is more than 2 year old, in management’s opinion these are recoverable and accordingly no provisions have been made.

Come next year management has written off all old debts at one go. Here it become a battle of intent- was it purely business decision or manipulation of balance sheet?

Investment stated at cost than M2M….can be double edge sword.

D**. Capital allocation**

Use five year cash flow statement and spot following:

- growth and maintenance capex

- dividends paid

- buybacks

- acquisitions

- borrowing repayment

- investments made

Idea is to compute A. Gross Capital distribution-all adjustments stated above B. Gross surplus/deficit- cash flow from operations minus gross capital distribution C. Non operations funds managed i.e. borrowings or capital taken to manage deficit or pay off surplus via dividend/interest. D. Net surplus/deficit- Gross deficit/surplus minus non operations fund ; if management is managing capital efficiently net surplus should be minimal which is nothing cash balance held for working capital max.

E. Trading risks and rewards

Spot changes in management compensation to two variables, one is performance i.e. ROE, second trade off decisions.

For example by taking a decision of leasing an asset on lease instead of buying management has been able to reduce capital expenditure funding. The return on invested capital is superior to cost of capital which resulted higher ROE/earnings. It deserves a case for compensation rise.

Few other questions from the book “The Investment Checklist”

- Whether management is owner operator or hired hand? This is a good point but most of good small cap are owned significantly by promoters in India due to unfavourable valuation and reluctant financiers.

- History of manager to rise - if he has spent lot of time from floor to board room considered as an asset. Bit dicey to me, likes of Bansals or Zuckerbergs will vanish then.

- Compensation to ownership- preferably one should own more shares than taking big salary. This is again debatable, it depends on governance structure. Vishal Sikka leads Infosys well, but don’t expect him to own 15% of Infosys…he just can not afford to. Mukesh Bhai reducing his salary every year, does it really matter?

- Management buying and selling- valid point, if management is selling what is the point of buying. Except the intent, if Mukesh Bhai sell 200 shares it may be some technical requirement, how does it become relevant to his burgeoning billion dollar wealth.

- Involved in day to day operations- agree, that’s why I call them Men at work.

- Earnings guidance- if company is issuing guidance management may be under pressure to achieve target and in process takes decision which are not good for long term health. In India few issues earning guidance , small cap almost zero.

- Decentralised business- agreed, but struggling for long time…how? And what is the impact on competitive advantage?

- Valuing employees- no comments!

- Capital allocation- agreed

- Buy back- agreed, part of capital allocation decision

- Passion- love business not money; great but how do I know?

- Moment of integrity- lots of good guys never publish goodies what they do. If you know fine.

- Management communication consistent- agreed, we spoke in detail

Lastly few years back one of my seasoned investor friend was gung ho about a owner promoter who was chatting with normal shareholders at break during AGM. I immediately drawn his attention to iconic William Durant who was known for all these chit chats, ultimately he went bankrupt along with feel good investors! Not trying to say every story echoes in same way.

The point I am trying to make is 98% efforts should be applied for reading between the lines, triangulation than AGM chit chats, news paper philanthropy. For that I guess we need to be least bothered if my CEO use chartered flight as long as he is delivering stellar returns and profits for us. Not all of us like same lifestyle, frugality is a feel good factor, but can it be forced decision???

Good wishes