The Strategy of Having a Concentrated Portfolio

Moving away from bit of continuous stuff on stock analytics, this was something I was discussing in my group couple of hours back. Couldn’t wait more to share post meeting.

It has been an eternal debate whether to have a concentrated or diversified portfolio. One section believes diversification means diversifying the risk, hence it’s better off to manage a big carnage. On the other hand second section believes diversification stems from not knowing, if you know everything about a company (which is available at good valuation alongside better earning prospects) then why other company is required even? Chalo, at the worst case another 3-5-7 companies. And even with wide diversification how come 50 bad companies together create wealth? Approach to concentrated portfolio became a ran away hit term with time as Mr Buffet keep emphasising.

First and foremost no matter however we discuss we wont get a concrete answer to this question, the irritating and common excuse again is “specific to individual”. But I want to get in those attributes what one should be aware before thinking of a concentrated portfolio.

In common parlance we understand concentrated portfolio as:

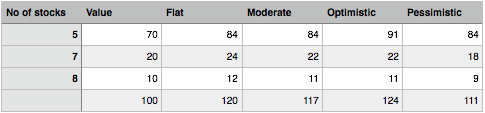

20 Shares market value- 100, 5 of them -70, 7 having -20 and balance 8 have 10 bucks market value. Basically we are saying the value of portfolio is focussed to few stocks. By doing this what happens?

See the below table:

This is a favourable outcome where we are expecting our big stocks (in terms of value) will out perform others. If price goes for all of them by 20% then it becomes 120, take this as base; 20% return for us. If big stocks appreciated by 20% and smaller ones goes up by 10% my return falls to 17%. If I take optimistically 30% growth for big boys and 10% for small then my return moves to 24%. If I become pessimistic with a negative growth rate for small ones and 20% positive for big ones my return fall to 11% but negative. The key message here is if a small number of stocks properly selected and out perform, even with so many mistakes with large number of stocks we can still deliver positive return. But the big assumption these concentrated stocks need to perform, now what happens if they don’t perform.

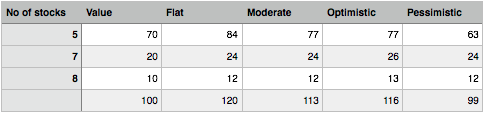

This is the table where small ones perform better than big ones, we can see even return can plunge to negative in a pessimistic scenario against positive return of 11% in the first table. That’s a whopping difference of 12%, this can do wonder as compounding marches on.

Fair, drawing fine lines:

- A concentrated portfolio accelerates CAGR in turn creates wealth faster. Easy and simple.

- Negative CAGR in market turmoil or even a carnage can be minimised when times are running bad. And this is a huge plus for long term investors who can minimise the negative CAGR.

- Pyramid becomes easier i.e. adding positions on shares which prices are rising. You need to allocate capital on few winners (rather having a large population) and this is very helpful for salary earners.

- Even minimum error in selecting a stock will push you to a negative CAGR. And every negative CAGR you need more force to recover next year making challenge higher. It break few people to lower down the expectation. Negative CAGR is one of worst thing than can happen to an investor.

But these are arithmetical probability of concentrated portfolio. What about scenario planning, we all know neither market is linear nor index is static.

Scenario 1: 5 stocks today have 70% market value of portfolio, after 3 months plunged to 30%. How you are going to react assume you don’t have to deploy additional capital? Are you going to sell profitable shares (smaller ones) and consolidate again? Or you maintain reduced percentage thinking they will come back, then where is value based concentration?

Scenario 2: the concentrated stocks fundamentals plummeted without a correction in price. It justifies value base concentration knowing fully concentration will collapse soon. The smaller ones are still fundamentally solid.

Scenario 3: Smaller ones prices are rising distorting the concentrated values. How you are going to react? By selling them and adding further positions to bigger ones.

Honestly speaking an investor having concentrated portfolio shouldn’t bother about these situations. But only after knowing what is concentrated portfolio. The concentration is not build around value which is a market variable subject to wild gyrations.

Key attributes of concentrated portfolio

- Circle of competence: one must develop a strong circle of competence before even thinking about concentrated portfolio. One of major signal of achievement when you can start saying “I don’t understand this business”. This is the first and key attribute of concentration. Once upon a trading stock became 13% of my portfolio due to price rise, immediately I removed the amount from calculation.

- Clear differentiation: You should able to tell very clearly the concentrated stocks are superior to other ones. Either a strong competitive advantage, super business catalysts etc. Once again the testing line would be you should be able to say “my company A is better than company B and I know why, documented as well”. Larsen & Tubro and Punj Lloyd both looked attractive once upon a time, which led me to doom.

- Period of differentiation: some differentiation exist for a longer term like network effect companies where as few enjoys a cost or regulatory protection for a shorter period. You must be able to compute prospective concentration for a specific period. E.g. till 2019 my 5 stocks will continue to be in concentrated, by 2018 I must replace 1-2 stocks. Symphony was a great stock for me, but this time I was sure of a s shut down point and move accordingly.

- Never ignore valuation: you might have great companies as concentrated portfolio but at higher valuation. This though is quite normal as my best companies should be fundamentally sound, who cares for valuation gap. This may impact your CAGR materially, people use a mix of value gaps and value rich but fundamentally steady. Gillette is a great company but I was getting Marico at better valuation.

- Treating growth stocks: catch 22 situations whether to include growth stocks in concentrated portfolio. One of major attributes of concentrated portfolio is less volatility as we are looking to long term. When Wim Plast was blasting away I thought what will this plastic company do, I never added positions. Wim Plast ran like a horse leaving my CAGR behind for showing disrespect.

- Never ignore risk: concentrated portfolio shouldn’t include stocks which are politically or externally risky.I haven’t faced such situations till date.

- Gradual vs immediate sale: when market going downwards immediate sale can prevent downside and free up funds for reinvestment or wait. This is always problem for me as generally I go for one shot sale. With high concentration it can create a benefit or loss, say if the market is going upwards.

I didn’t want to include the common acts like long term investing, good management etc. The concentrated portfolio requires more hard work and documentation, update. Please keep on adding, I may do few more once it hits my mind.

Recently I red a book called “Concentrated Investing” by three authors. This book focus on few investment philosophies of highly respected concentrated investors profile.