Gulf Oil Lubricants Taking Look at Making Electric Vehicle Batteries

1 Like

Why the Lubricant players having low PE compare to other Auto sector companies? even the Castrol trading at low PE.

can someone from the forum share his/her current views on Gulf?

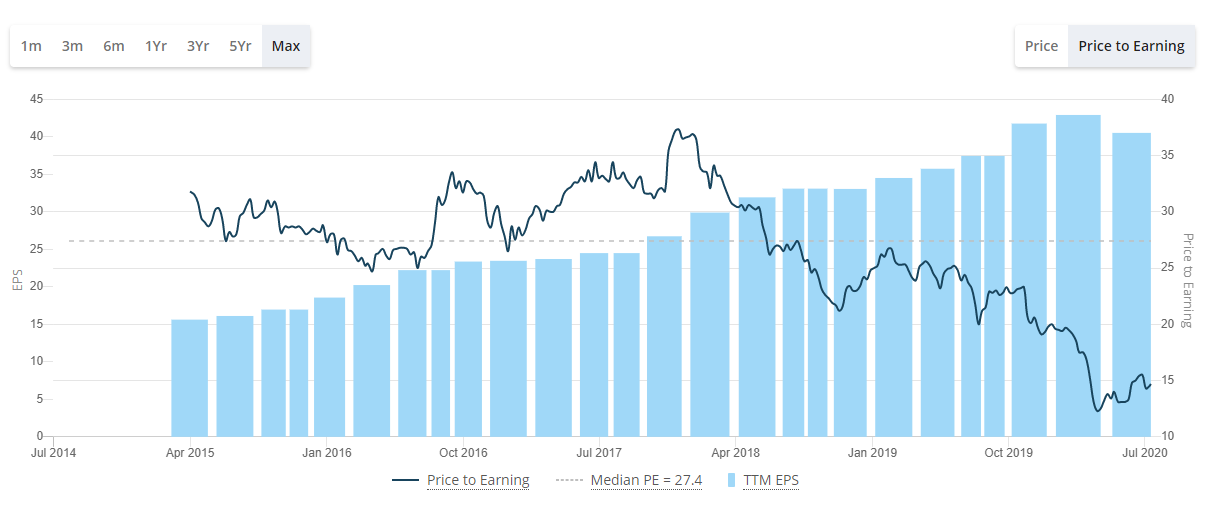

- Gulf is trading at cheapest levels in recent history on TTM PE basis (which maybe due to COVID)

- Axis small cap fund (whom I admire a lot, see Axis Mutual Fund schemes top returns charts across categories - The Economic Times) has recently entered into the script.

On initial look, Gulf looks like a steady/stable business with 5-10% topline and maybe a 10%-15% EPS growth to me. Slowdown in Autos/CVs should not be a problem for them coz existing vehicles which are “on road” are major share of customers for them (please correct me if I am wrong).

This might even be a buy for just 1-3 years till the time PE’s revert back to more “normalized” levels.

Views welcome!

1 Like

Will the tie up between Gulf oil lubricants and Indra EV and smart energy technologies be a game changer and will kickstart an uptrend in this stock. The current valuations look pretty good, financials decent, though these aren’t reflecting in the stock price. Will this be the right time to acquire this stock? Seniors please advise.

Con-call highlights

Volumes

In Q4FY21, all segments delivered double-digit growth yoy, with OEMs (incl. factory fill), B2B and exports also doing well. March base effect was there. B2C-B2B share was 60-40 as some parts of West India started suffering from Covid second wave in March 2021.

Industrial volume share rose by 1-2% qoq. Industry growth in Q4 was stable (10-15%).

Gulf Oil Lubricants India (GOLI) FY21 lube volume was 115mn ltr. The industry declined in double-digits, while GOLI grew by some points, thereby gaining market share. GOLI gained share in 2W-4W and agri oils. Only first 2-3 months of FY21 was severely affected by Covid and national lockdown. DEO and 3W took time though.

Q1FY22 saw the second wave affecting demand conditions (last 2-3 months), but management expects a sharp bounce-back once lockdowns are lifted as seen last year.

Lube is in the semi-essential category and anticipates an uptick in sales from Jun’21. OEMs are looking at good growth in next one year and are coming back in a good way. PM preference went up in Q2-Q3-Q4FY21 and more personal vehicles will be used. Maintains 2-3x of industry growth guidance.

There was 5% gross margin erosion in Q4 due to the jump in base oil prices. It was operating leverage from strong topline which lowered the opex impact. The company did cost optimization and travel was also not there. The situation is challenging but would try to manage EBITDA margins in the 16-18% guided band. The company took 2-3 different price increases across categories in the bazaar segment in last 4-5 months.

It has taken price hikes in response to increase in raw material costs and has covered for recent increases. Q2FY22 will see the full impact of price hike on realization as it flows into channel inventories.

OEM pricing is a standard process and is formula-based with 3-6 months frequency, but B2B is negotiation based. The upward trend in base oil prices now on may not be as steep as it is stabilizing at higher levels. Refineries are increasing runs globally with improved travel and fuel demand which should mitigate base oil supply issues.

No drastic change in competitive scenario was there in the market, and pricing was more or less in line among players. GOLI calibrates its pricing with the market.

GOLI has been adding retail outlets with 70,000+ now and focus remains on expansion.

Bikestop was same yoy at 8,000+ as it requires extensive BTL activities, which was affected by Covid. Rural stockists have increased. GOLI is 2nd-3rd in terms of brand position. The battery business did well in FY21 with Rs800mn in revenues and a positive bottom-line.

Cash flow from operations was strong in FY21 at Rs1.95bn, or 95% of PAT. Dividend was healthy. Capex-CWIP in FY21 was on plant relating to tankages, peripheral infra etc. done annually.

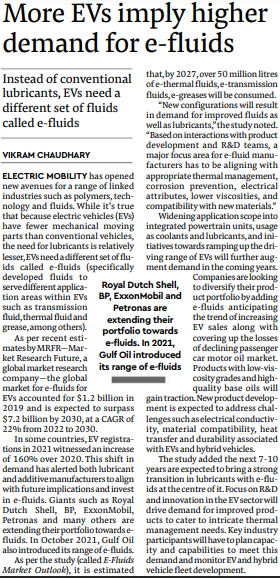

Ad activities included Gulf Pride with Dhoni, IPL etc. A&P spends stood at 4% of sales in Q4. Lots of Covid-related CSR activities were also done. Lube requirements in EVs is very low as there is no engine oil. There will be other oils such as transmission, gear and coolant. The company is looking at the EV value chain.

GOLI expects lube demand in India to grow for two decades with EV impact very less now.

It will start from cars and 2W. GOLI is looking into EV fluids. It has launched globally though not yet brought to India. It did investments such as Indra (home battery charging) as GOLI does not have retail fuel pumps.

It has single-digit volume share in synth-semi synthetic. So aims to grow multiple times of 2-3x normal market target. The focus is on mineral and semi within PCMO, etc. The company wants to increase market share.

Industry’s share of synth-semi is 4-5% as per internal estimates, and GOLI’s share is also similar. Pure synthetics are expensive and are for high-end vehicles. Management is not sure if the Indian market is ready as it is still a niche. The company is learning from other countries but has to manage local sentiments in synthetics.

Performance-wise, BS 6 lubes are also better despite being mineral-based. The market will move to BS 6 more and more. It is low on ash and sulfur emissions. It is a new product, so more costly and hence priced higher. BS 6 can be used in BS 4 engines also and will give higher life. The price difference between BS 6 and BS 4 engine oils vary from high-single digits to double-digits.

1 Like

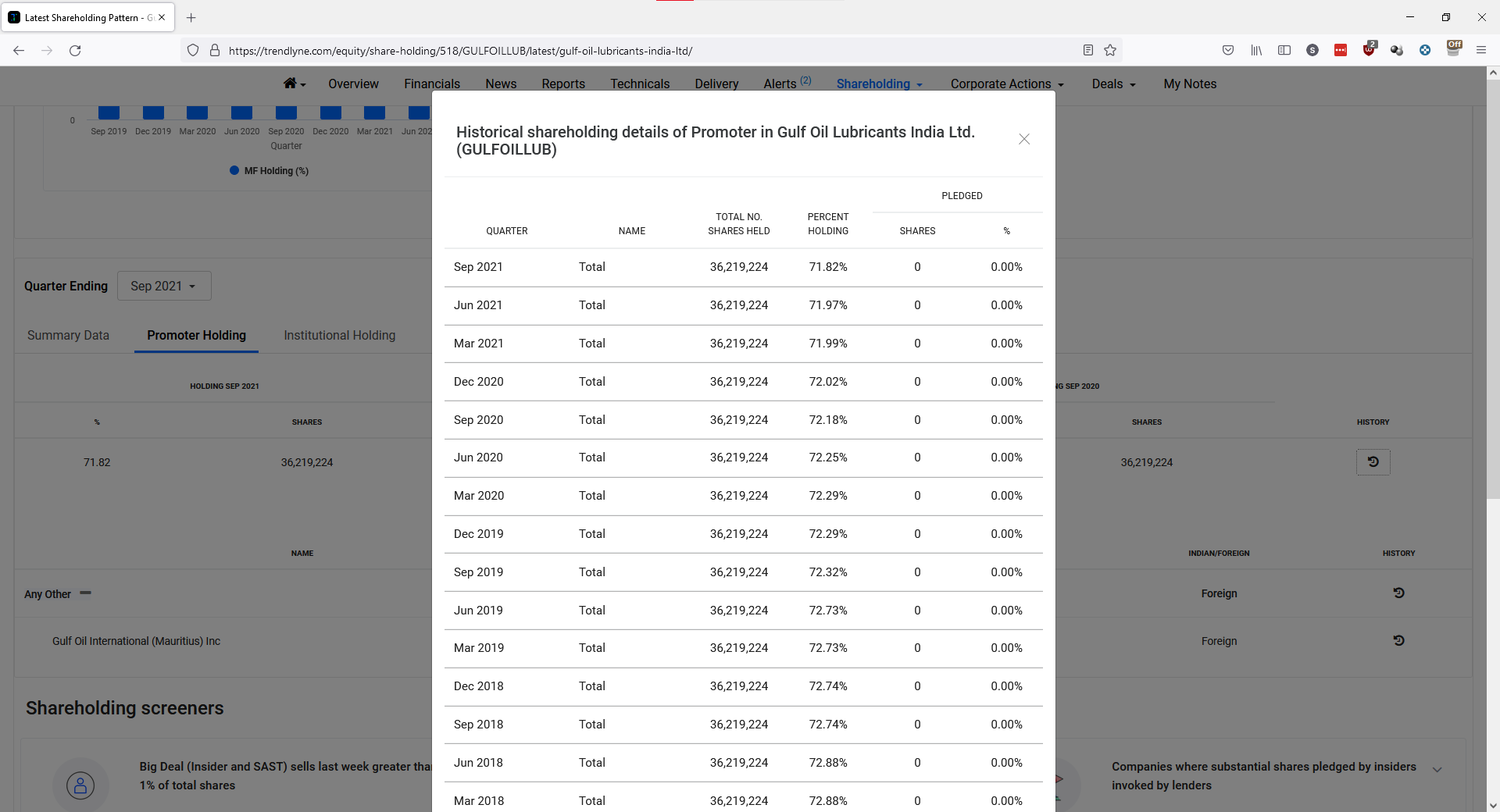

tq where can i see this number of shares held data ?

Hi guys, I was going through value stocks available. Gulf Oil Lubricants have strong balance sheet, good growth on a 5 year basis. It has a revenue of 387 Per share and 5Y avg EPS of 39 rupee per share. Has a good ROE. Only con I can see is emergence of EV.

Although I do see increase in EV usage among urban population, I still doubt that it’ll penetrate deep in india and also I honestly believe EV is still not an all purpose vehicle and it’s a nice additional vehicle to have at home. I have a strong urge to buy the stock. But I wanted to understand if there’s more to such strong negative sentiment over last one year. What do you guys think?

2 Likes

Look up Savitha oil tech…it has more moat and diversification than this …as it’s also into transformer oils and more EVs means more transformers …they also have vehicle lubricants… It’s cheaper than this …

3 Likes

I think this article and more specifically the comments will give you some idea.

this is 2016 industry report. I found on Google for Castrol. This will give you idea of industry landscape.

PC_-Indian_Lubricants_Sector-_Sep_2016_20160920081315.pdf|attachment (994.7 KB)

Thoughts of novice investor, invested in Castrol

I had looked at Castrol and Gulf Oil.

I finally chose Castrol. I had bought it when the dividend yield was 4% for Castrol, which was greater than that of Gulf oil.

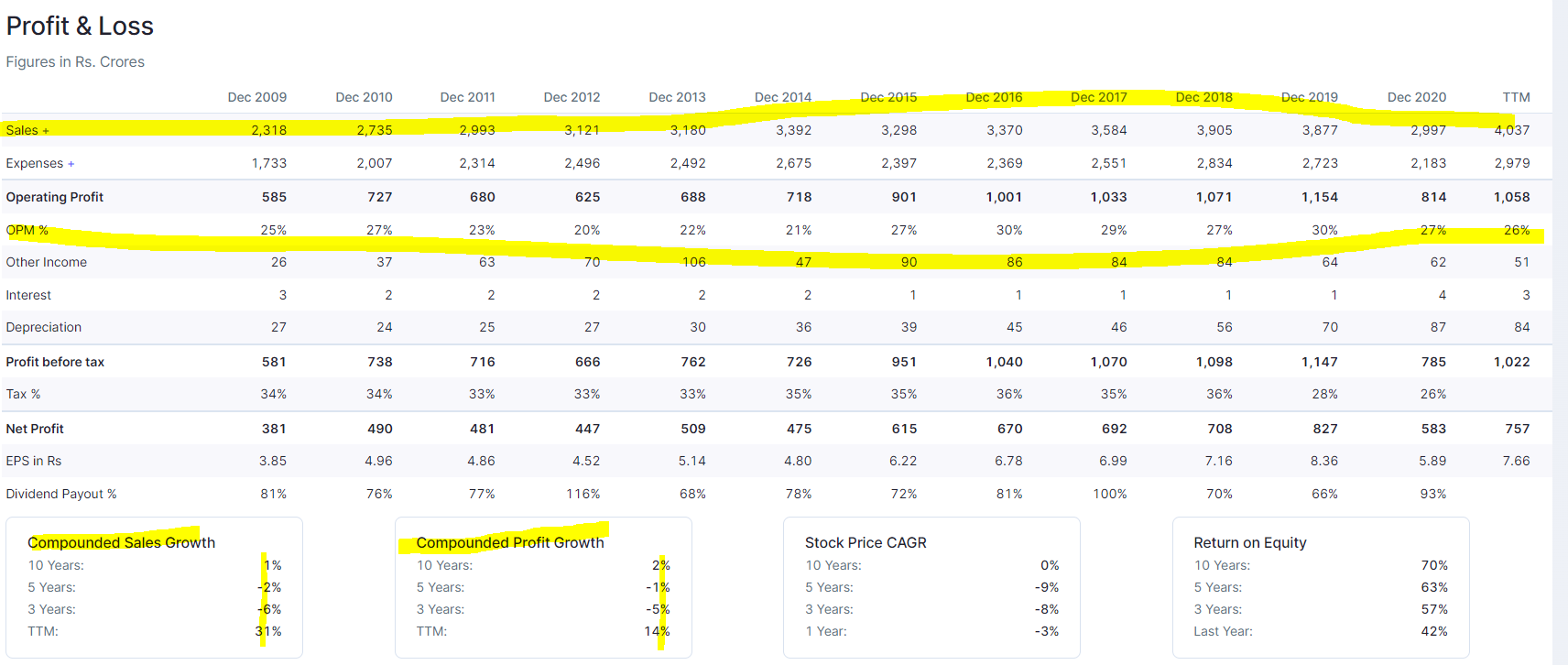

Furthermore, I liked the operating margin of Castrol (27-30%) compared to 16-18% for Gulf Oil. I believed the high opm means better pricing power.

Castrol

Sales have not grown much and opm is range bound. The company is not trying to gain market share by cutting price.

Castrol has made limited investment in PPE in last 10 years. So the mgmt itself believes there isn’t going to be growth in sales.

the company was planning to increase size of its Silvassa plant (from 80ml to 120 ml) but as per latest news the mgmt. seems to have shelved the plan.

Gulf OIL

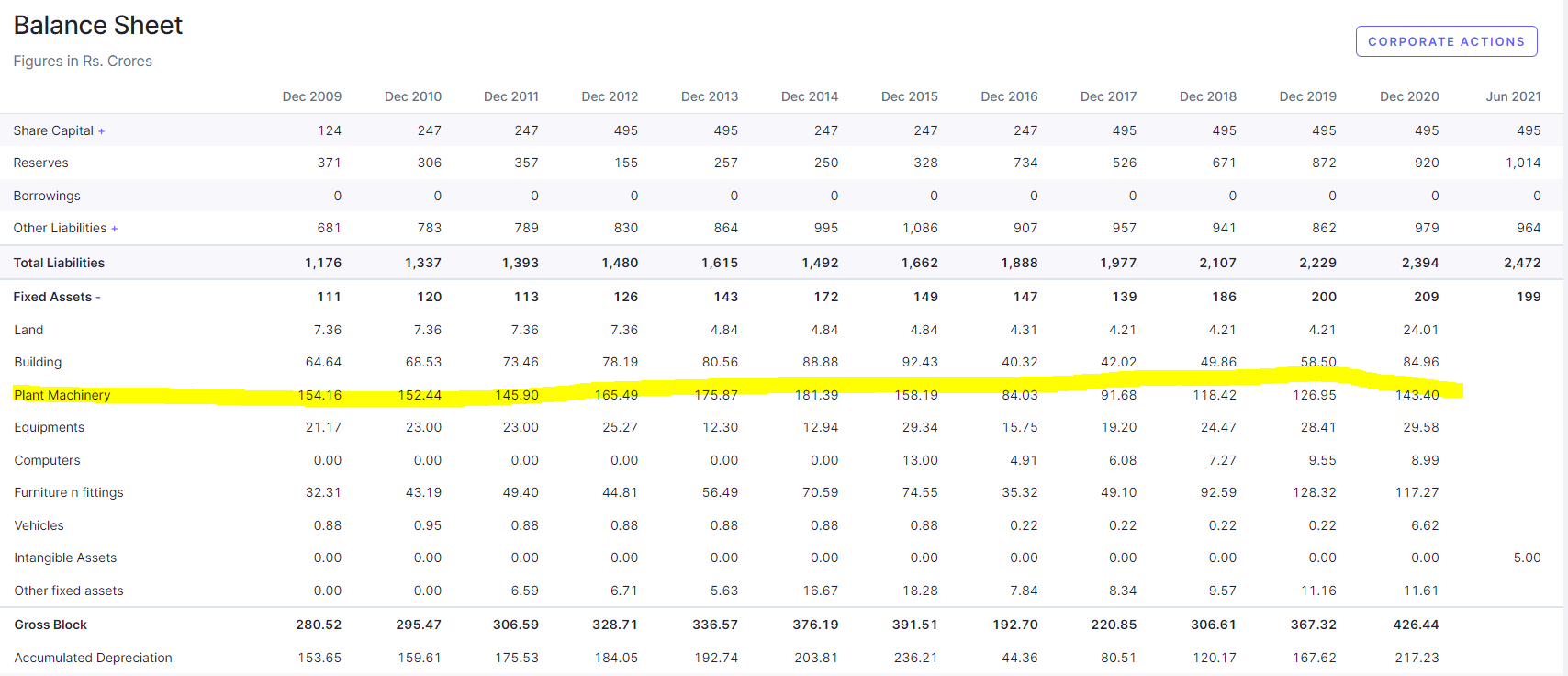

there has been increase in capex and opm has stabilized

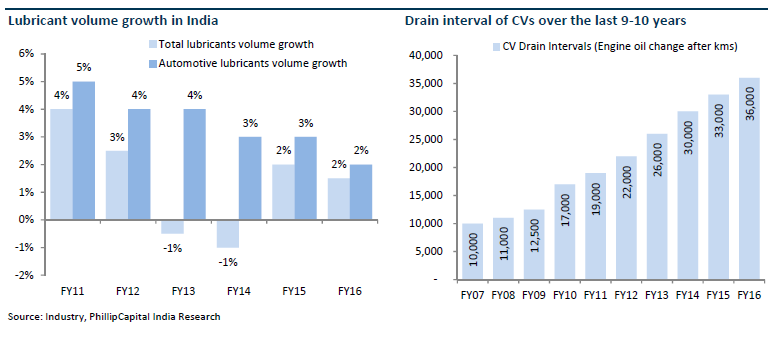

The problem with this industry is that volume growth is very slow.

The commercial Drain interval of CVs over the last 9‐10 years has increased. This has led to slower volume growth.

One thing I would like to add is the CV drain interval is distance as well as time interval concept. I feel the market understands drain distance intervals but not the concept of time interval.

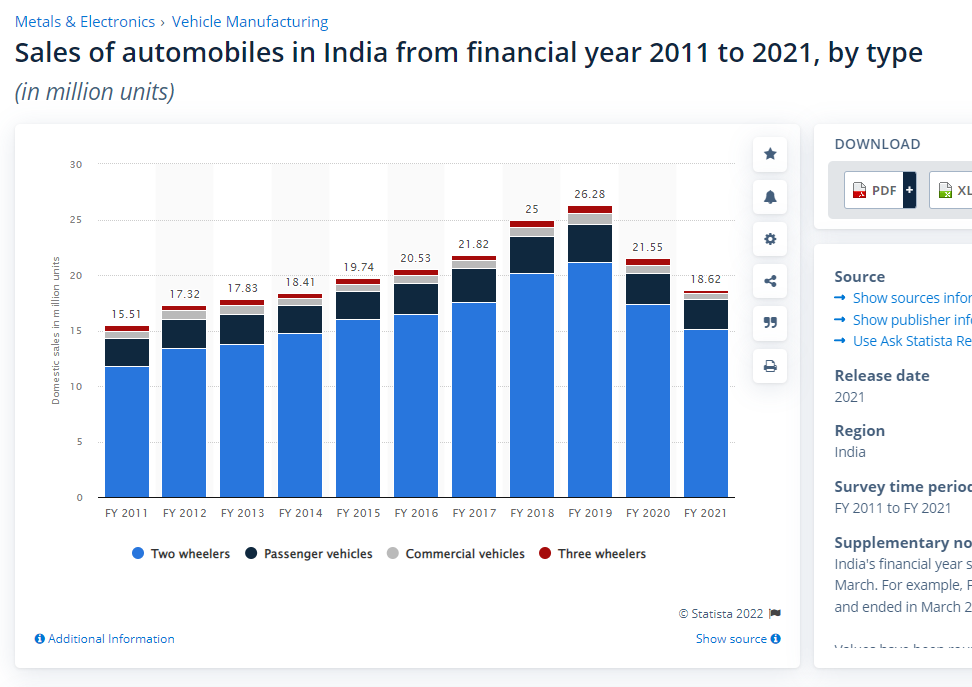

Another issue is that new vehicle sales have been very sluggish.

Source: • India: automobile industry sales by type 2021 | Statista

EV Technology is also a concern. I believe it is a big concern for 2 wheelers. Majority of the users wont travel long distances using a 2W, so EV technology for 2W will be economically viable . But I am not worried about Commercial vehicles and Passenger Vehicles. For Castrol considerable sales come from 2W.

Although, even EV do require fluids and castrol has some product offering for this segment. But sales are negligible as of now.

I own Castrol stock(6% of portfolio). I kept it because it pays a decent dividend. From a 20 years holding period perspective, this sock may make some money. The lubricant market will grow but I am not sure exactly how much will be impacted by EV. However the growth will be slow and agonizing. I still remain invested because I like the odds but I won’t be making any more investments in the near term.

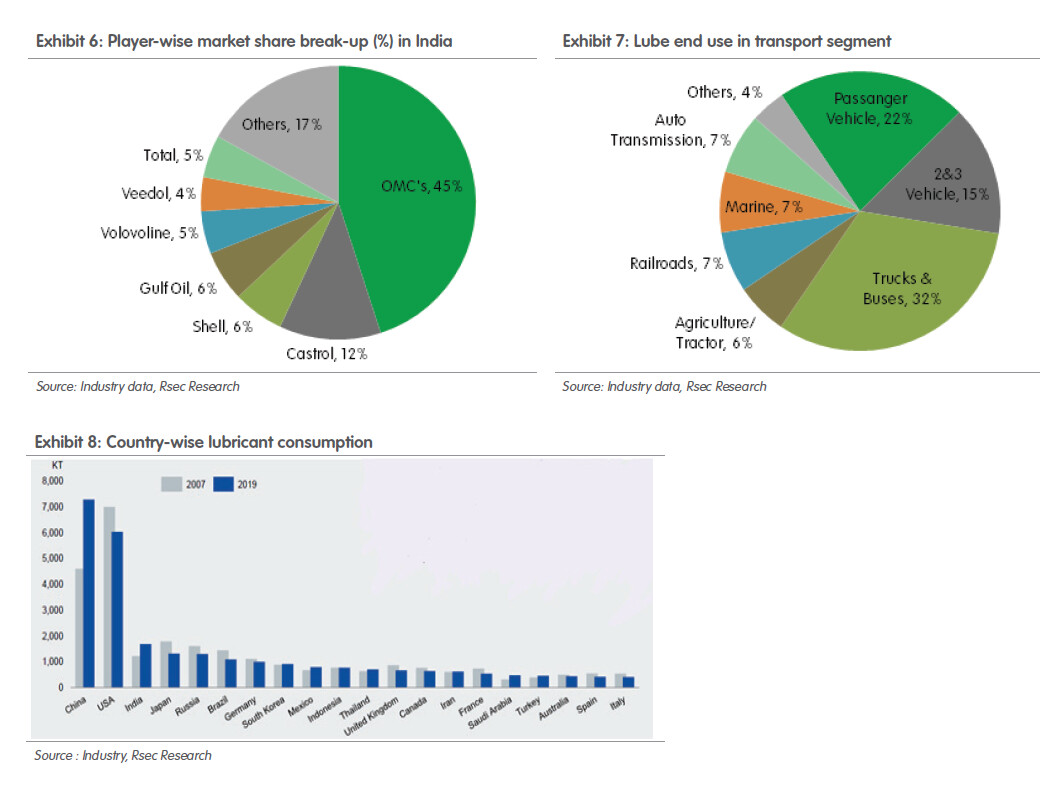

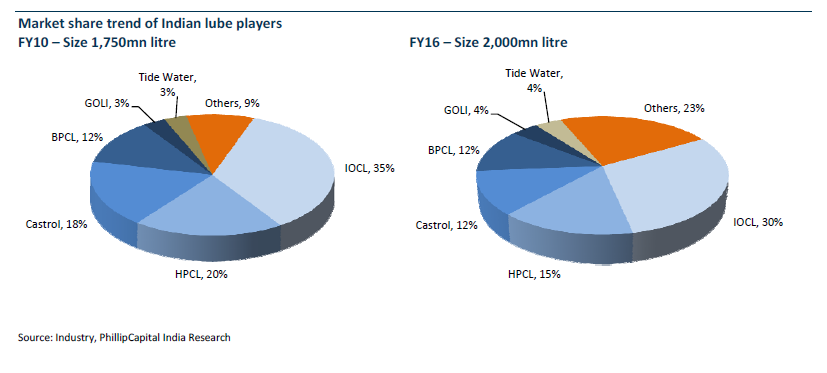

one more thing castrol has been losing market share from 18% (below)in 2015 to 12% (above) in 2019. Gulf has increased its market share.

Source:

castrol—initiation—211020 (1).pdf (1.2 MB)

PC_-Indian_Lubricants_Sector-_Sep_2016_20160920081315.pdf|attachment (994.7 KB)

9 Likes

Ever since dividend distribution tax is removed and govt started taxing it in the hands of the investor, it is more inefficient for retail investors who are on the tax bracket of 20% or above.

I have a good amount of Vedanta shares and the qoq dividend is too good despite the investor unfriendly management. But the tax out go makes me feel I should sell out and invest in a business that reinvests more than give it as dividends. I’ll ride the commodity cycle and will exit when I feel the peak is reached.

Disc:

No investment in Castrol or gulf lube.

Will delete the post if someone feels it’s not relevant to the thread

2 Likes

IDirect_Castrol_CoUpdate_Feb22.pdf (464.8 KB)

3 Likes

1 Like

Rising demand for lubricants and oil from original equipment manufacturers (OEMs), given an upswing in the commercial vehicle cycle and an increase in freight movement on national highways bodes well for the Hinduja Group company - Gulf Oil Lubricants (GOLIL). Besides, GOLIL is making strategic inroads into the battery business and during FY24, the company is planning to localise production to boost battery availability in the B2C market. This expansion is expected to fortify GOLIL’s position in the battery industry and drive growth in the coming years, analysts at Ventura Securities note, who recently initiated the coverage on the stock.

Source : Zee Biz

1 Like

Company is doing well on prospects.

1.Growing faster than industry rate

2.Entering into EV segment

They have cash equivalents of 654 crores. Despite they are utilizing short term borrowings of 332 crores. They are even paying hefty dividends and buyback also.They have even paid interest of 37 crores in Fy 2022-23.I couldn’t understand the reason behind non payment of borrowings.

1 Like