Hi

Is there anyone tracking GRP these days. I am just trying to understand their business, valuations, opportunities and threats in the present scenario

Kind Regards

Jose

Thanks Ayush for your views and this thread. I would like to read up more on the company

I could not download the file properly…Tyre Asia Aprl10.pdf. each time I got a corrupted file. In case you have a copy saved, and any further info, could you please mail me that.

Kind Regards

Jose

Feautred in Tyre Asia Mazagine.pdf (1.1 MB)

Sharing the same

1 Like

Thank you very much, Ayush firstly for this forward and secondly towards your valuable contributions…

GRP Ltd AR21 notes

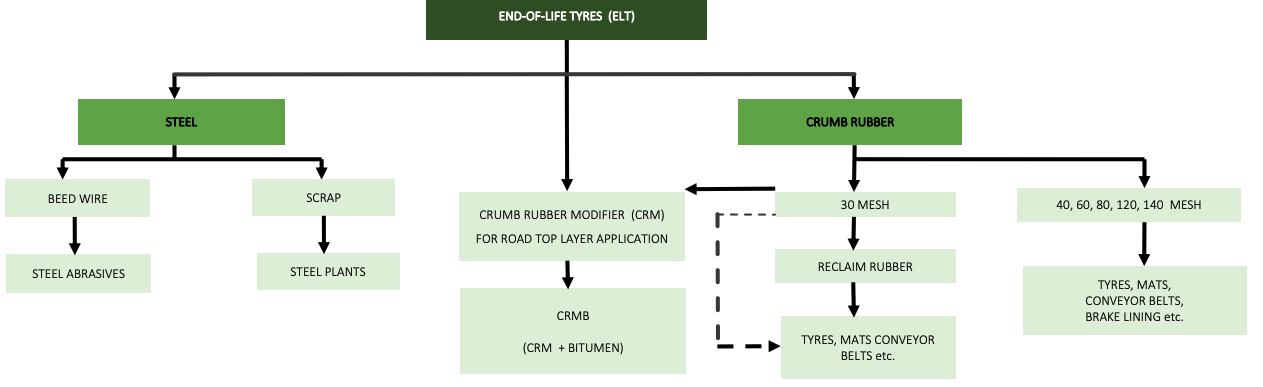

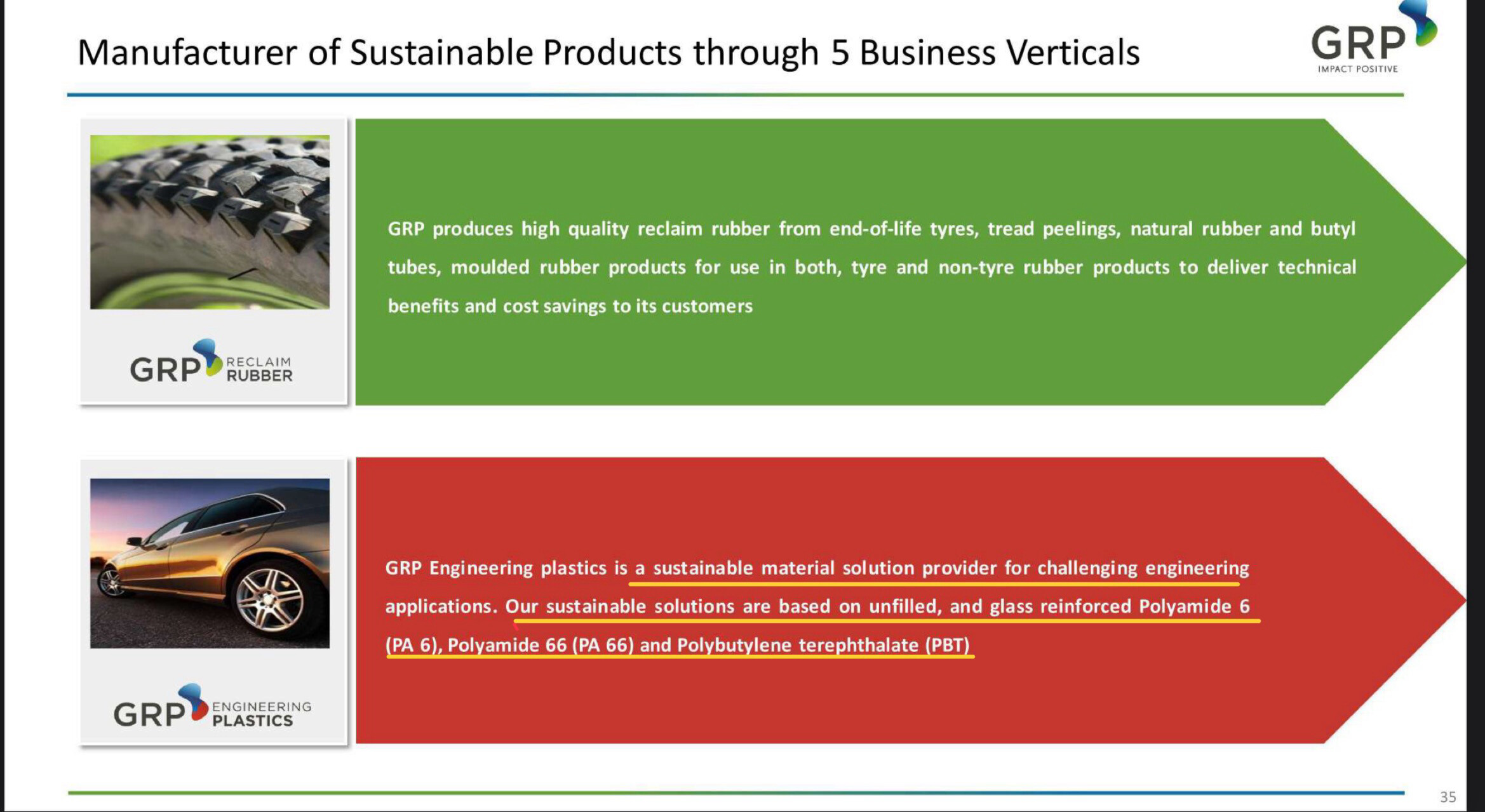

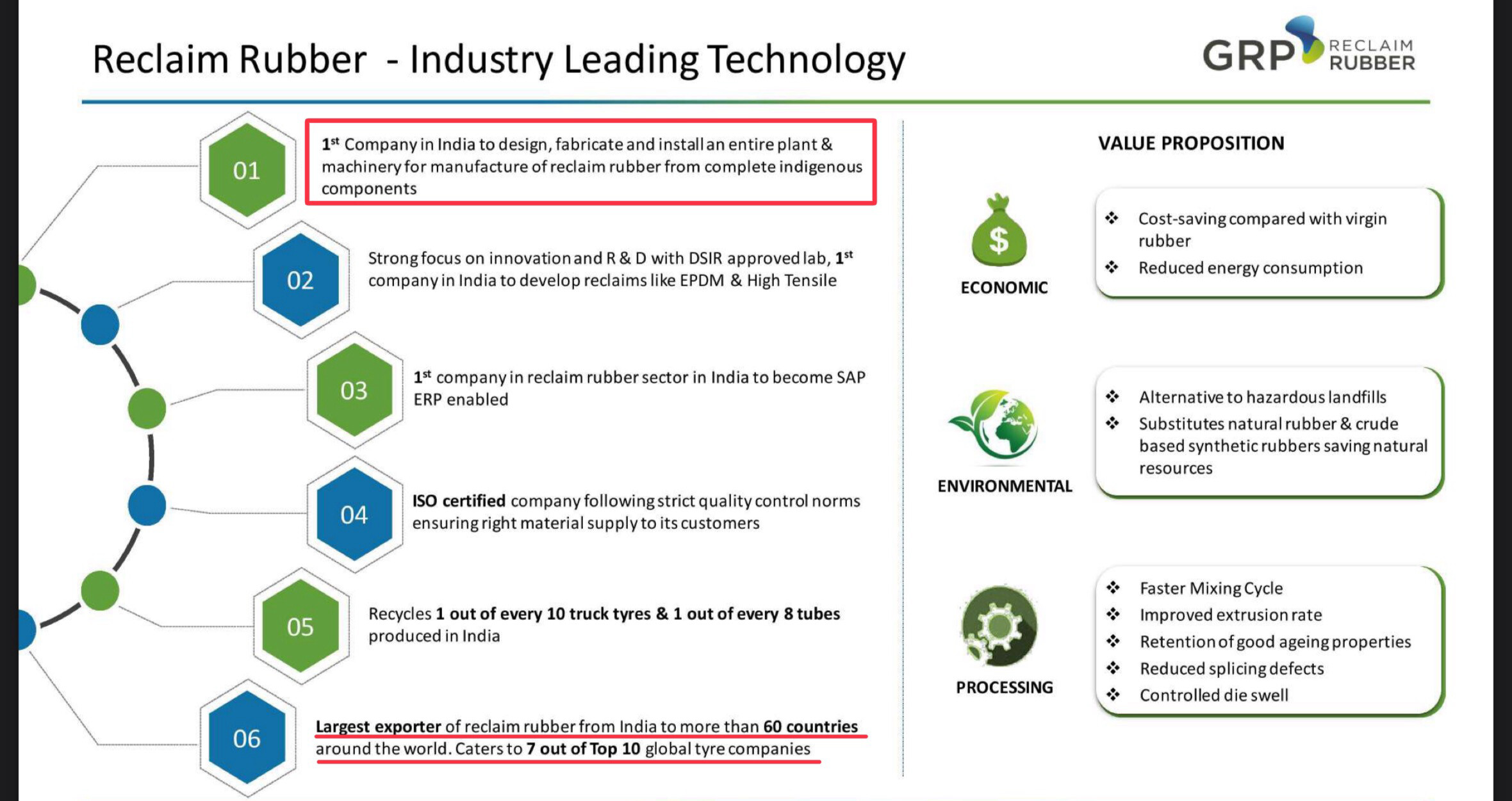

- Reclaim Rubber: This was the genesis of the company and this business procures tyres at its end of life, to produce reclaim rubber (a replacement to Natural & Synthetic Rubber) for use predominantly by tyre manufacturers.

- Engineered Plastics: Another business recovers Polyamide waste from tyres and along with other forms of EOL waste to produce Engineering Plastic compounds for sale to the plastic manufacturers in the automotive and electrical applications.

- Polymer Composites: The residue rubber from the above businesses is used by yet another business to blend with recycled plastic waste to produce composite material which replaces wood & concrete. The applications for these composite boards are mainly in the transportation industry and currently limited to North America only.

- Tyre Retreading: A Commercial Vehicle retreading business in Joint Venture with a global company, Marangoni SpA to help fleet owners extend life of their tyre by providing additional life.

- Your company is the leader in the tyre recycling industry not just in India, but is among the Top 5 manufacturers of the above products globally

- The financial year gone by has been one of the most challenging years your company has faced. Beginning March of 2020, when the COVID pandemic forced the world into a lockdown, businesses across the world focused on survival.

- In the backdrop of a human tragedy at a global scale and a near shut down of operations in the first 4 months of the fiscal, your company delivered a revenue of Rs 28,134 lakh in the fiscal year 2020-21 compared to Rs 34,930 lakh in the previous year, a drop of 20%. This was mostly due to a 21% drop in volume of Reclaim Rubber sales.

- The silver lining in the performance has been the growth in revenue from the nonReclaim Rubber business by 23% from Rs 1,660 lakh to Rs 2,052 lakh and a return to profit after tax of Rs 164 lakh compared to Rs 300 lakh in the previous year. This was on the back of an 18% volume growth with the rest on account of improved realization and product mix.

- With a growing customer base and addition to capacity including several Tier-1 and MNC customers, we expect to gain further traction in the non-reclaim rubber businesses going into FY 2021-22 with a higher share of revenue.

- The Engineering Plastic business of your company was primarily driven by Nylon 6 but during the year under review, your company has also diversified in Nylon 6,6, PBT & HDPE compounding. Your company’s strength in new product development using EOL waste materials has helped in product and customer approvals across other polymer categories also. As we leverage our supplier network to collect alternate waste plastics, this business will have strong interdependence with Reclaim Rubber.

- The rise in commodity prices provided an opportunity to increase price of our products thereby resulting in margin improvement in the second half of the financial year.

- The performance of the Other businesses has been encouraging. Your company’s Engineering Plastics business has gained product approvals from several reputed customers in the Automotive, Furniture, Electrical applications and has successfully commissioned additional production lines during the year under review. By the end of the fiscal year, it had an order book to cover the capacity addition for the year.

- The Polymer Composite business has grown volumes during the year under review and with a recovery in North American transportation markets, is poised to continue its growth in the current fiscal.

- The Other Business segments have strong interdependencies and have potential for long term partnership with brand owners and material manufacturers which should help your company in reducing its concentration risk.

- During the year under review, the company has invested Capital expenditure towards enhancing capacity in the Engineering Plastics business and continued automation of Reclaim Rubber processes. The company has also invested in enhancing capacity of a mechanical process for manufacture of Reclaim Rubber with a long term aim of reducing process emissions and effluents. This alternate process has received approval of key global customers and will help pave the way to increased adoption in the future

- Retreading

- The core of MGPL’s strategy – RINGTREAD – grew by about 60% but shortage of material due to production and global shipping challenges dented the growth somewhat. A key focus area for the year was to compete with market leaders in ‘bias/cross-ply’ segment like MRF, Elgi, Indag and Midas. MGPL’s product brands, UNITREAD and CLASSICO doubled their sales thus helping MGPL becoming an ‘all-solution’ provider to fleets.

- Industry’s first fully online / remote commissioning of a new retreading plant was achieved in first quarter of financial year 2020-21. Later the entire training too was delivered digitally and appreciated by the new Franchisee.

- Fledgling partnerships with a tyre major and online tyre retailer are gradually getting established with the former contributing 3% of monthly sales and expected to get into double digits next year. At the end of the year, there was a healthy pipeline of prospective Franchisees that will help MGPL achieve a truly national footprint in the next 12 months.

- As the world limped back to normalcy post the lockdowns in Q1 of fiscal 2021, the onetime surge in passenger vehicle sales was followed by a sustained recovery in replacement tyre sales globally. A spurt in commodity prices meant a close to 50% rise in Natural & synthetic Rubber prices and this provided an impetus for a rebound in demand for Reclaim Rubber starting end of Q2. With your company’s focus shifting from commodity grades to high performance grades of Reclaim Rubber, demand for certain product categories has witnessed a robust growth in the second half of the year under review. This demand spurt, along with a price rise in virgin rubbers has helped your company in improving margins across this business. The company continues to engage with its key customers in enhancing the quality of its products and also opening opportunities in increasing use of Reclaim Rubber in formulations.

- During the year under review, your company temporarily discontinued manufacturing at its plant in Tamil Nadu. This was necessitated on account of the lower orders and lack of approvals for the location. This turned out positive as some of the capacity from the plant was added in the other plants and helped in increasing share of wallet at key customers.

- The pandemic also brought raw material availability constraints to the business on account of lower generation of EOL tyres. This coupled with rise in oil prices meant a tight supply chain and our inability to service all orders in time.

- A major shortage in container availability globally (which continues in Q1 of FY 2021-22) has led to further delays and increase in freight costs. With 2/3rd of your company’s volumes being sold to customers across 50+ countries, the global shipping crisis in the year under review had a major impact on potential margins and has put in question the advantage that the Indian Reclaim Rubber industry has had over its competitors globally.

- Exports Rs. 184 cr in FY21 as compared to Rs. 250 cr in FY20.

2 Likes

New Hiring !

Circular economy is catching a lot of tailwinds in the western world.

Interesting company to track.

Appointment of President Marketing & Business Development

Discl: Small position

1 Like

I am analyzing Tinna Rubber vs GRP to understand the differences, competitive positioning & the reason for a vastly different P&L & balance sheet. Some initial insights I have been able to gather:

-

Tinna Rubber & Infrastructure Ltd. - Valorem CXO Meet - YouTube Please see from 56:10 He tells diff between grp & tinna

Grp is only into non road segment, tinna gets 40% or so from road segment Also, grp only makes rubber reclaim products, does not make micronised rubber powder. Tinna does Not sure what implications this has on Gross Margin & opex but will try to dig deeper. - 1 more key difference which came out in grp concall : grp receives shredded tires so no steel is present in them they don’t process the steel Tinna receives ready made tyres which have steel in it & tinna produces steel abrasives out of the steel wire present in the tyre & sells it as well.

- One more critical difference: 90% of sourcing for grp is biax tyres only 10% is radial tyres. Tinna 100% is radial tyres. According to both concalls, Radial tyres are growing much more rapidly than biax types. Tinna also says in their concalls that radial tyres are higher quality & enable them to make higher quality products.

- Tinna employee costs are around 9-10% compared to 15-17% for GRP. Even tinna used to be around 15-17% mark until fy21, only fy22 onwards, employee cost fell sharply to 9%. We find the reasons in FY22 & Fy21 annual reports: excerpts below:

- On EBITDA margins, GRP freight costs is massive at 50cr, so we have to validate whether export is really high margin for them (ex of the freight costs), Tinna in comparison being largely domestic focussed has negligible freight costs (Tinna gets 5% from exports, GRP gets 40% from exports)

- Material cost: wise both are neck & neck, around 45% material costs in FY22 for both of them.

-

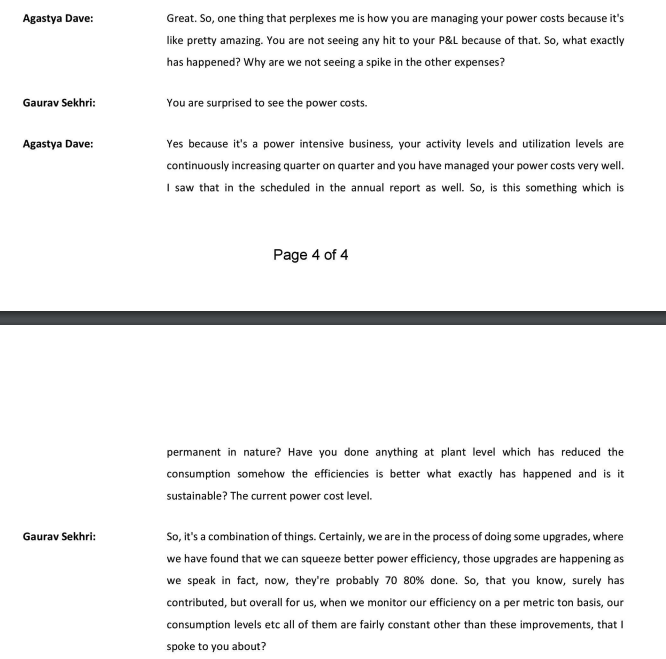

Power costs: Even on power costs Tinna has some details in Concall though not very satisfactory. Let us examine.

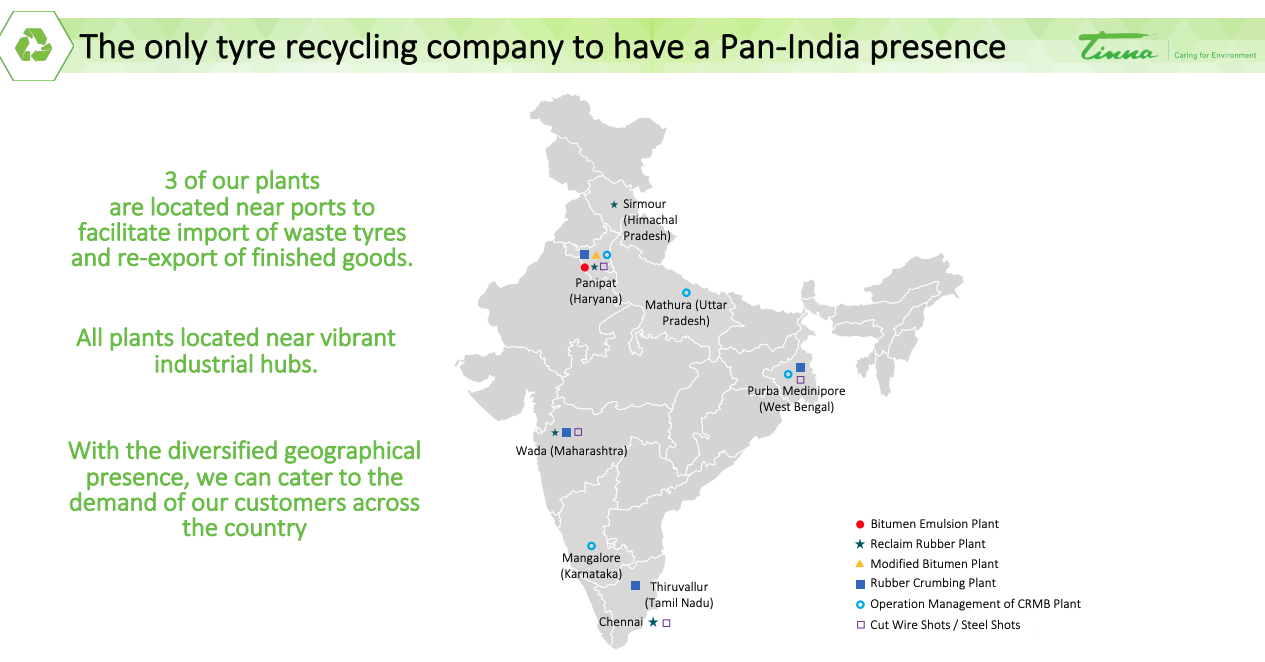

This is a little bit vague & i would love to ask Tinna management what these exact upgrades are which enable higher power efficiencies. One thing to note here is that Tinna has a more diverse manufacturing footprint with plants in Himachal, harayana, Maharashtra, Tamil Nadu & West Bengal

As opposed to GRP which has its manufacturing footprint concentrated in West India (Gujarat, Maharashtra, MP).

The power costs in Gujarat are 6.6 Rs / Unit.

Power costs in Maharashtra are around 8-10 Rupees for commercial users.

Power costs in madhya pradesh are around 7 Rupees per unit. The blending % would depend on the % mix between the manufacturing footprint. A simple average of the 4 plants gives us a blended cost of Rs 7.5 / unit.

As compared to this, for Tinna, the cost of power in Himachal is around 4.2 Rs / unit post subsidies.

Harayana is around Rs 4.3 / unit

Maharashtra has 1 plant which from previous work is around Average of 9 Rs / unit

Tamil nadu is around Rs 6.35 / unit

West bengal is around 4.5 Rs / unit (see during day hours for industries)

Averaging it out for Tinna, we get

(4.2+4.3+9+6.4+4.5)/5 = 5.7 Rs / Unit.

Effectively what this means is that there is a possibility that Tinna might be sourcing its electricity at 30% cheaper rates (we should confirm these assumptions via concalls of both GRP & Tinna). This can partly explain some of the differences in power costs for tinna & GRP. For GRP power costs / revenue is around 12% versus 8% for tinna. Normalizing for the rates of power, The difference is not much. of course these calculations are not exact because Tinna & GRP both could be sourcing some of power in-house as well (solar, wind).

Summary of Findings in tabular format:

| Attribute | GRP | Tinna |

|---|---|---|

| Fy22 Revenue | 388 | 237 |

| Tonnes sold | 60000 | 50000 |

| Realization / Ton | 64666.66667 | 47400 |

| FY22 Material Cost | 47% | 46% |

| FY22 Employee Cost | 15% | 10% |

| FY22 AR on Employee Cost | Statement on ‘continues to invest in upgrading its plant processes towards increased automation’ but cannot see material impact in Employee costs | Implemented automation to save manpower costs. talked in FY21, walked the talk in FY22 AR |

| Fy22 Power & Fuel Cost | 47 | 19 |

| Fy22 Power / Revenue | 0.1211340206 | 0.08016877637 |

| Cost of power unit blended avg in Manufacturing locations | 7.5 Rs / Unit | 5.7 Rs / Unit |

| FY22 Freight & forwarding expenses | 53 | 5.45 |

| Product mix | Only non-road products. Only reclaimed rubber products | Road segment products & non-road segment products & micronized rubber powder. Also sells to building material cement additives |

| Raw material mix | 90% biax tyres & 10% radial tyres | 100% radial tyres |

| Raw material state | Receives shredded tires so no steel is present in them they don’t process the steel | tinna does the shredding & so processes the steel, sells steel abrasives |

this analysis is by no means exhaustive, will continue to add whatever i learn on GRP & Tinna.

Disclaimer: have a position in Tinna, studying both tinna & GRP more deeply.

19 Likes

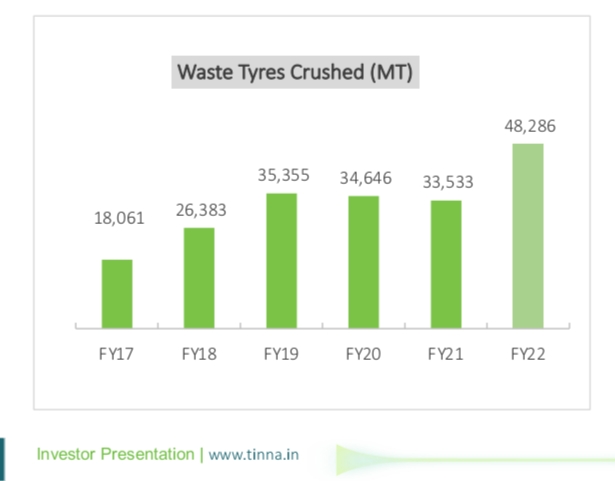

While analysing the Power and Fuel cost, we should also consider the difference in volume of waste tyre crushed by Tinna Rubber year on year.

Tinna Rubber has crushed 48,286 MT of waste tyre in fy 22 against 33,533 MT of fy 21, an increase of 44% yoy.

Source of information

https://www.bseindia.com/xml-data/corpfiling/AttachHis/ad6f07e6-f3bd-4ad3-bdd2-eb8e882654db.pdf

While Power and Fuel cost of Tinna Rubber increased to 19.31 crs in fy 22 against 13.94 crs of fy 21, an increase of 38.52%.

9 Likes

2 Likes

Mr. VK Misra, Technical Director, JK Tyres & Industries Ltd. expressed that contrary to the global scenario, we do not have any waste tyre and every kg is consumed in various processes in India. The important aspect is proper use of end-of-life tyres which are environmentally friendly. We need to collectively plan steps to ensure this and find solutions to hurdles to which we are expected considering not an organized process. While it is important generalize disposal of waste tyres, it is even more important to recover raw material from these which would be true circularity. Currently, in India the recovery is very limited and we need to work towards getting support from the government. A lot of work is happening to recover carbon black, a key material for the rubber industry and polymer as well. This is the area which requires large investment with various adequate technology.

2 Likes

A Waste to Wealth Approach

A little bit old but very extensive and insightful:

https://www.google.com/url?sa=t&source=web&rct=j&url=https://www.chintan-india.org/sites/default/files/2019-01/Tyres%20Report_Final.pdf&ved=2ahUKEwix0uXphbX5AhVO_mEKHZv8B2gQFnoECBYQAQ&usg=AOvVaw1AEwQEvXKYQE0m-KkbxWk6

This policy brief is based on Chintan’s study ‘Circulating Tyres in the Economy: A Waste to Wealth Approach to Old Tyres’. It draws from Chintan’s extensive experience in informal waste management and recycling in northern India to shed light on the economic and environmental benefits of utilising Crumb Rubber Modified Bitumen (CRMB) made from ELTs for road construction and maintenance in India.

This report attempts to capture the salient policies and practices of reuse and recycle

of ELTs that are being undertaken across both India and globally, while also exploring,

in detail, the best possible alternative currently available to India for safe end-of-lifehandling practices for tyres.

The first section provides insight into the scale of the problem of ELTs at both the

global and the national level. This section also attempts to provide an overview of the

current systems of recycling that are prevalent in the country. Given that there is not

much direct documentation on the scale and pattern of recycling in the informal sector,

the section draws extensively from Chintan’s on-ground study and experience, which

focuses on the informal sector of tyre recycling in North India. The section also provides

an overview of recycling in the formal sector of ELTs with an introduction to the Indian

reclaim rubber industry. This industry comprises of only 60 odd manufacturers of which

6-7 manufacturers like Balaji Group, KK Reclamations, Tinna Rubbers, GRP, Kohinoor

Rubbers etc. serve as leaders.

7 Likes

One of most important insight i have found on GRP vs Tinna in Tinna’s Q4 concall

Question:

Hi, sir, could you help understand about MRP on reclaimed rubber usage in tyres, so, do the

applications vary or is that MRP can contribute to higher replacement potential.

Answer:

See MRP and reclaim both are having the different applications so MRP is picking up, reclaim

is More degenerated. It does not add the added advantage to the rubber compounds it is just

a cost saving option for the user whereas the micronized rubber powder MRP is a semi

enforcing filler. So, this is basically helps in the cost saving as well as it also gives the stable

parameters technical parameters to the tyre producer.

GRP is primarily in Rubber Reclaim segment:

No mention of MRP in its investor presentations, Concalls or annual reports.

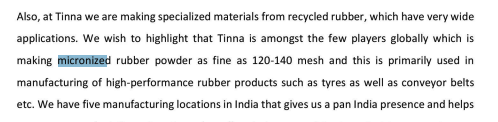

Tinna on other hand is among one of only MRP producers in the world (from tinnas Q1fy23 concall):

He also explains what the diference between CRM & MRP is. MRP is just a finer/smaller version of CRM. CRM are large rubber chunks.

^ The one on extreme right (above 120 MESH) is MRP.

Expectedly they would not bond or dissolve easily with bitumen or other rubber of the tyre (he explains that here: The Tyre Recycling Podcast | Episode #24 | Business Witness: Gaurav Sekhri - YouTube).

This is why MRP is a superior product (easier & more structural integration with virgin rubber or bitumen).

Tinna did 10000 ton of MRP in FY22. Source: Tinna Rubber & Infrastructure Ltd. - Valorem CXO Meet - YouTube

That is roughly 20% of their volume output (must be higher % of value output).

Could be part of the reason why GRP has not been able to grow its topline is it possible that MRP usage increase is causal or correlated with CRM usage plateauing?

Disclaimer: invested in tinna, studying GRP as well for competitor analysis

8 Likes

Thanks Sahil. More on MRP here

Came across this company called Lehig Technologies in the US which sort of pioneered this product it seems. It was acquired by Michelin in 2018

Very interestingly came across this ex Employee who was advisor to Tinna Rubber’s CEO.

I am not sure how much of the MRP that Tinna produces they are selling to tyre co’s at the moment

3 Likes

How is your product similar/different to reclaim?

The core difference between Lehigh’s MRP and reclaim is the treatment during the manufacturing process. Generally, reclaim rubber is chemically and heat treated, causing the properties of the base compound to degrade. Lehigh’s rubber is cryo-mechanically treated, preserving the properties of the base compound. This enables MRP to provide performance benefits in many applications.

Safety and the Environment

Is your product safe?

Micronized rubber powder has gone through extensive testing in the U.S. and Europe by independent laboratories and government agencies for health and safety. A list of these tests and conclusions, including Lehigh Technologies’ third-party REACH/SVHC report, can be obtained by contacting us here.

How does using Lehigh’s MRP help protect the environment?

By incorporating MRPs into products, users:

- Prevent end-of-life tires and post-industrial rubber from entering landfills

- Preserve resources like oil and rubber by reducing the volume of oil-derived, virgin materials, which reduces energy consumption tied to manufacturing new products

- Lower CO2 emissions derived from production of virgin raw materials by about 40 percent per pound of MRP

4 Likes

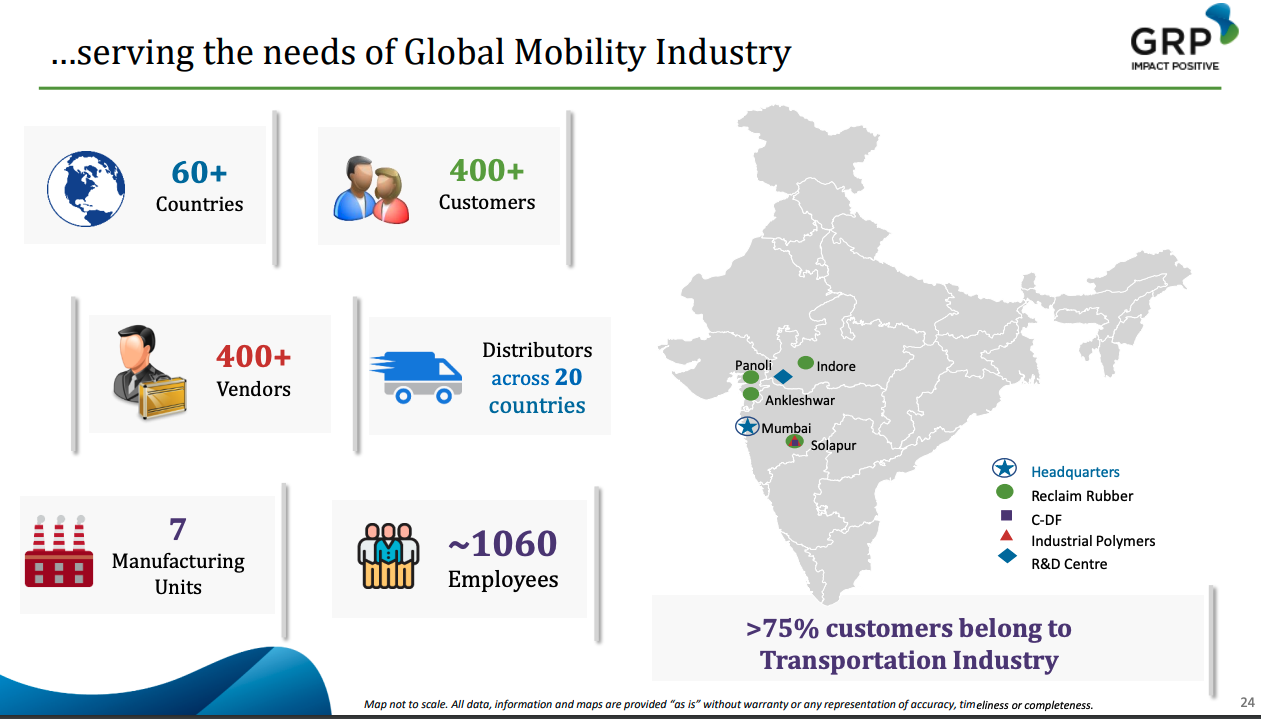

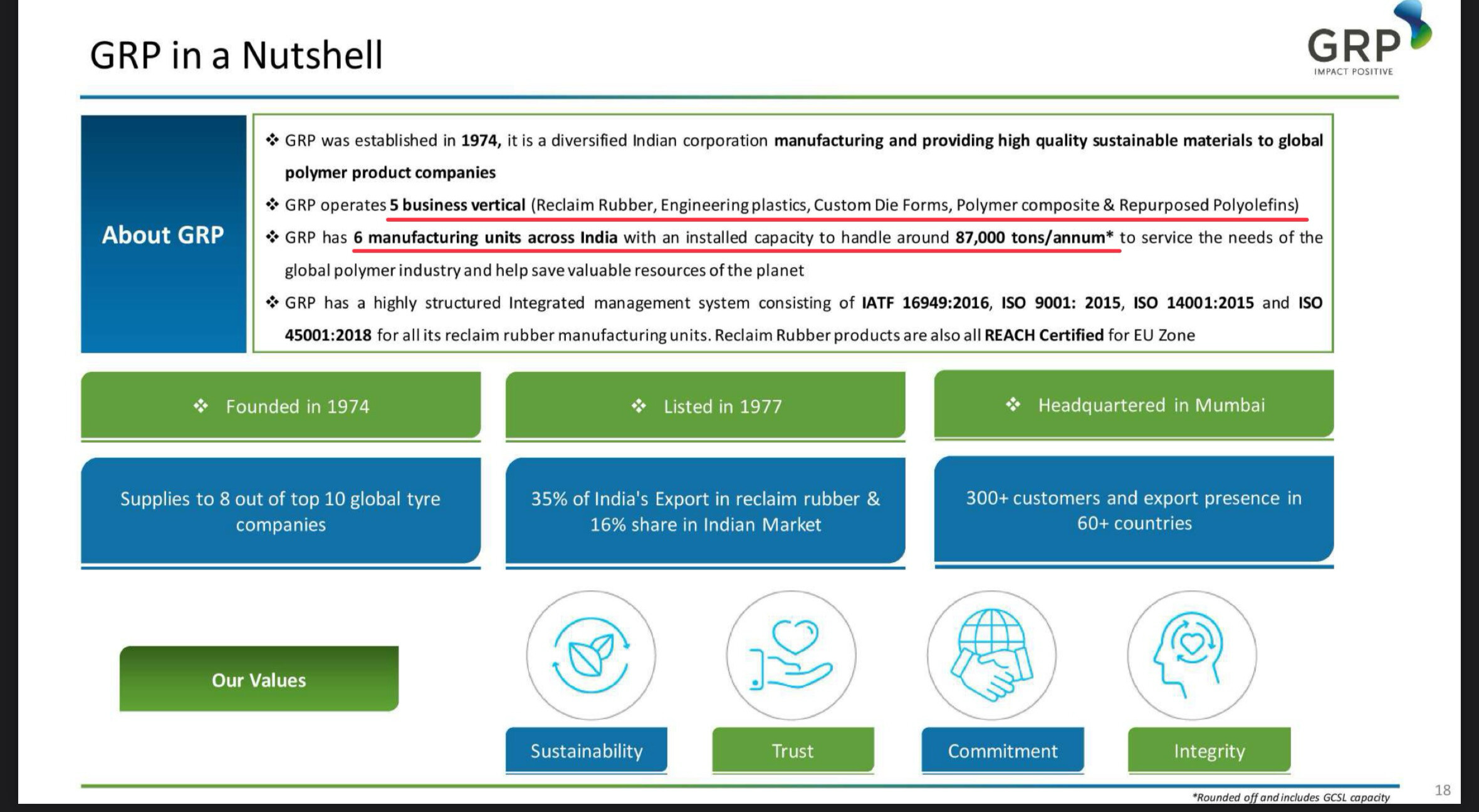

Annual Report 2023 notes

Highlights

• Supplies to 8 out of top 10 global tyre companies

• Certified by IATF, ISO, EMS, OHSMS, REACH for EU Zone

• Exports to 60+ countries

• Globally, ESG as a framework continues to gain momentum.

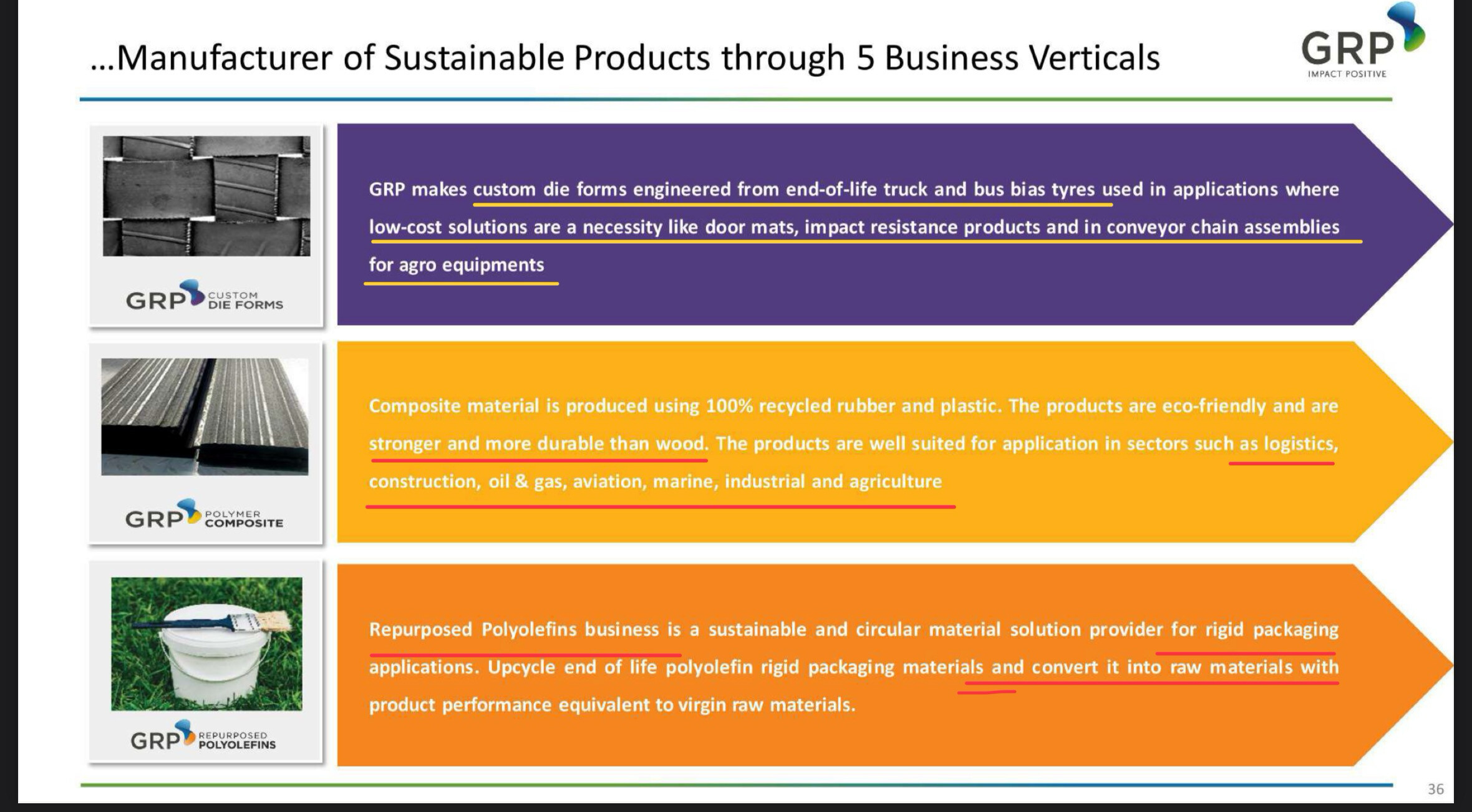

Businesses

-

Businesses centred around serving the mobility sector,

a) Reclaim Rubber (RR) business which has a 70% dependence on the automotive sector (tyre manufacturers, automotive component manufacturers)

b) Engineering Plastics (EP) has a 40% dependence on automotive OE supply chain

c) Rubber Composite (RC) has a 80% dependence on the transportation sector

d) Custom Die-forms (CDF) has a 40% dependence on agri and earth moving equipment. -

Reclaim Rubber (RR): Business has the capacity to process 72,000 tons per year.

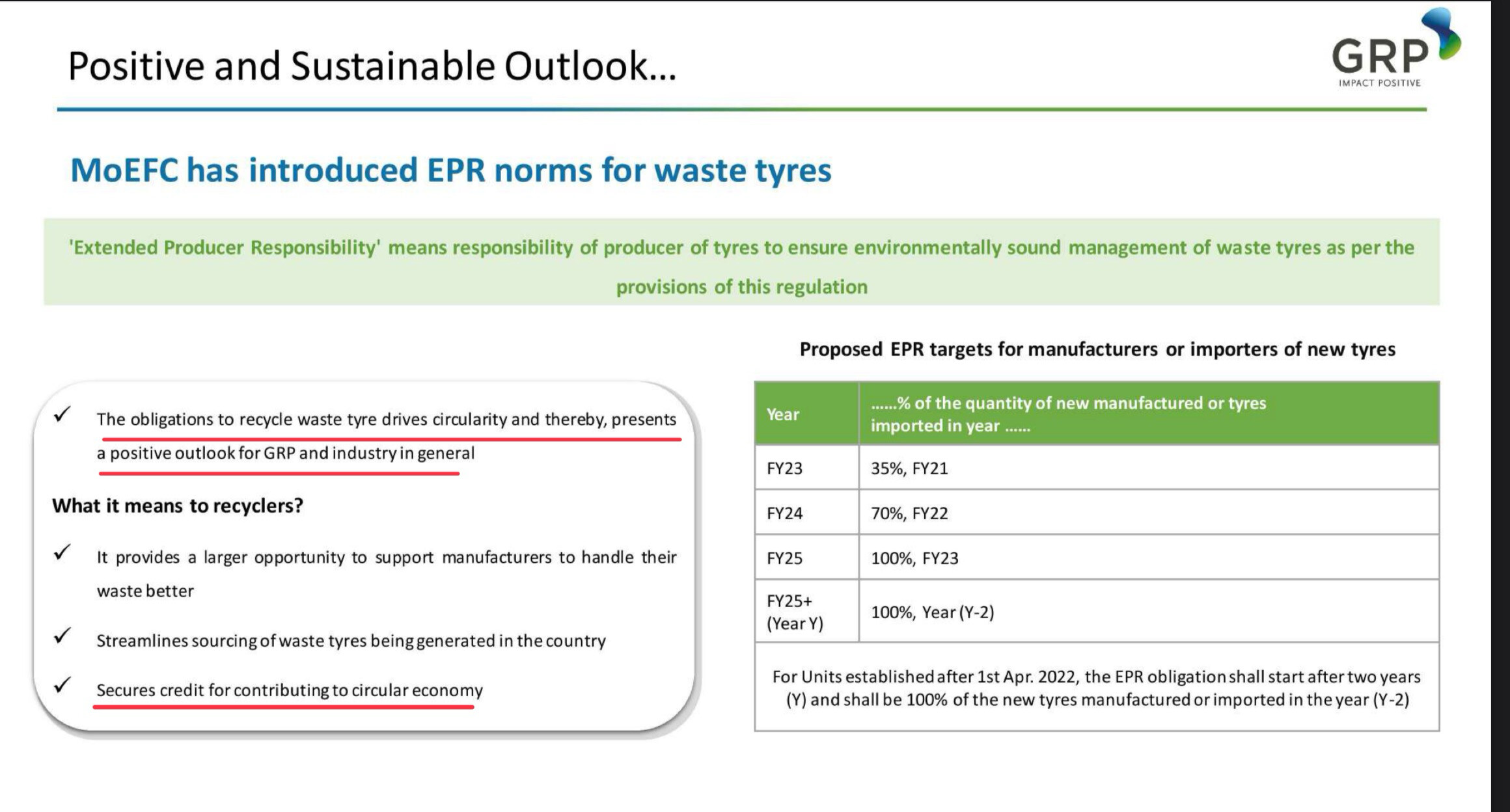

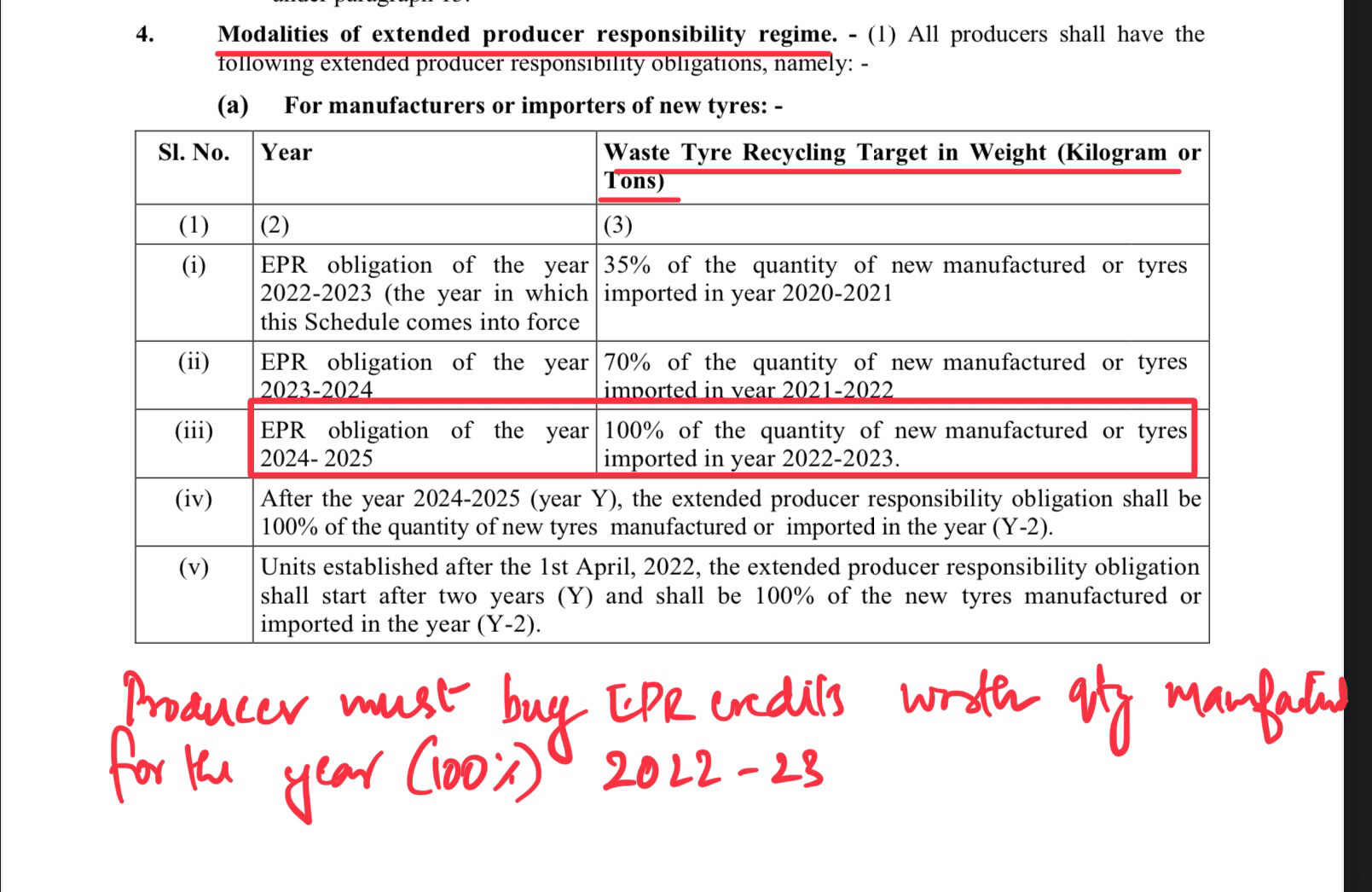

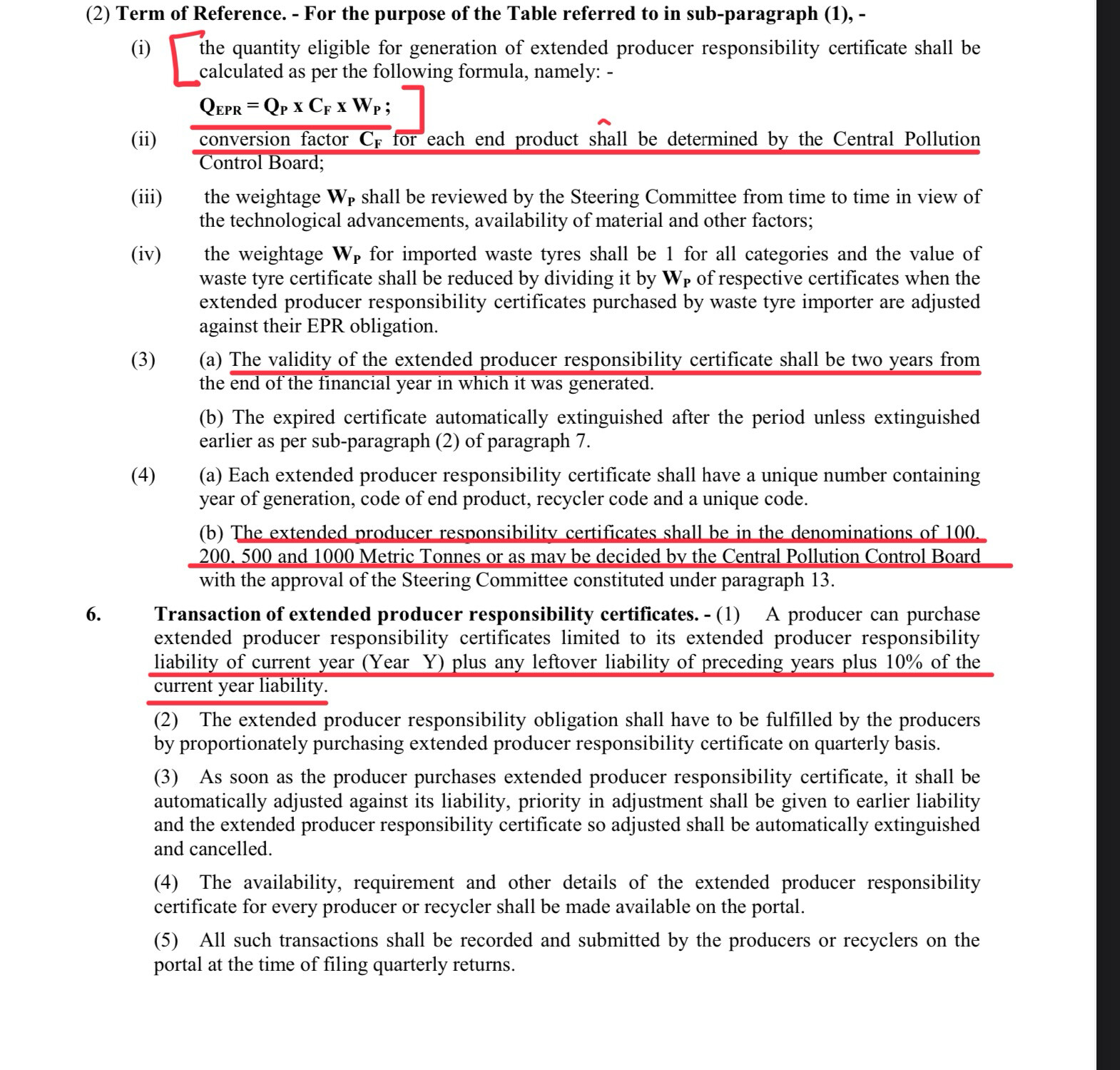

Extended producer responsibility (EPR) regulation

a) Regulation mandates tyre producers to offset their production with purchase of EPR credits from recyclers, who’ll be entitled to receive credits for the production of specified materials from EOL tyre waste.

b) Likely to be implemented during the HI FY 2024

c) Will provide recyclers an additional source of income, which is intended for use in new technology development, offset costs associated with supply chain for sourcing EOL tyres

d) GRP shall be a major beneficiary of the regulation and help it generate additional revenue to help create an inclusive supply chain. -

EP business

• The company undertook expansion of recycling capacity from 2600 tons to 3600 tons and compounding capacity from 3,400 tons to 6,200 tons

• Business witnessing increased customer approvals and acceptance of the product portfolio.

• With several customer approvals in automotive, electrical and compounding industries, the overall non-RR business witnessed doubling of revenue, with EP leading the way with a 56% growth. -

Repurposed Polyolefins:

• Company at the forefront of development of materials from rigid EOL packaging waste based on Polyolefin materials (mainly Polypropylene, Polyethylene).

• Gained approvals from premier global petrochemical brand Mobil for use of its materials in their packaging.

• (From last Con-call) - Only supplier to Mobil, for use of the material in commercial pails made with 50% post-consumer recycled polypropylene.

• Engaging with several brand owners for product approval, and are fairly confident to be able to gain more prominence during the year

• Provides impetus for other brand owners to work with GRP in establishing use of its products. The capacity for the business stands at 6,000 tons annually.

Industry dynamics

RR business

• The domestic tyre industry grew at 4% YoY.

• GRP has been successful in growing its market share amongst the leading tyre companies and continues to develop alternate products for future use.

• Share of exports continues to remain around 35% and while the share of sales in India has dipped marginally to 16%, the share amongst tyre companies remains at around 30%.

• While the overall rubber consumption in India has grown by 4%, GRP sales in India has grown by 7% in CY 2022 over CY 2021. Global consumption of Rubber has witnessed a reduction by 0.8% vis-à-vis GRP export volume change of 7% from CY 2021 to CY 2022.

• In international markets, GRP continues to be recognized as the industry leader and brand owners are engaging with GRP to switch to cleaner technologies to produce high performance RR.

• Remain confident of being able to introduce improved technology to produce high performance RR during FY 24.

(from last con-call) – Asset turns will be higher with this new technology compared to traditional RR business

Non RR

• Brand owners such as Kia, Hyundai, apart from other global brands have announced targeted use of 30% recycled plastics by 2025, providing much needed impetus.

• India continues to remain attractive for several large material manufacturers to invest in (Lyondell Basel, CPH Chemicals, Radici, Domo all setting up new capacities in India)

• GRP’s key strength is the backward integration to the source of EOL waste. This coupled with the focus on development has and will continue to bring growth for this vertical.

• The new facility for EP will be operational within H1 of FY 24 and facility shall incorporate improved infrastructure and processes.

Opportunities

• With a large export customer base, company has access to low cost EOL materials from around the globe

• Approached by several global waste management companies for possible cooperation, joint collaboration and is evaluating those opportunities

• Tyre industry experts are expecting an uptick in Indian market for next 3 years owing to

- available new capacities

- anticipated infrastructure growth

- internationally rubber consumption is expected to notably recover driven by expected growth in auto sector and rebound in China

Risks

• Restrictions for import of EOL waste could possibly lead to increased prices of key raw materials across all BUs

• Gujarat Govt has increased minimum wages by 25%, putting pressure to automate quicker

4 Likes

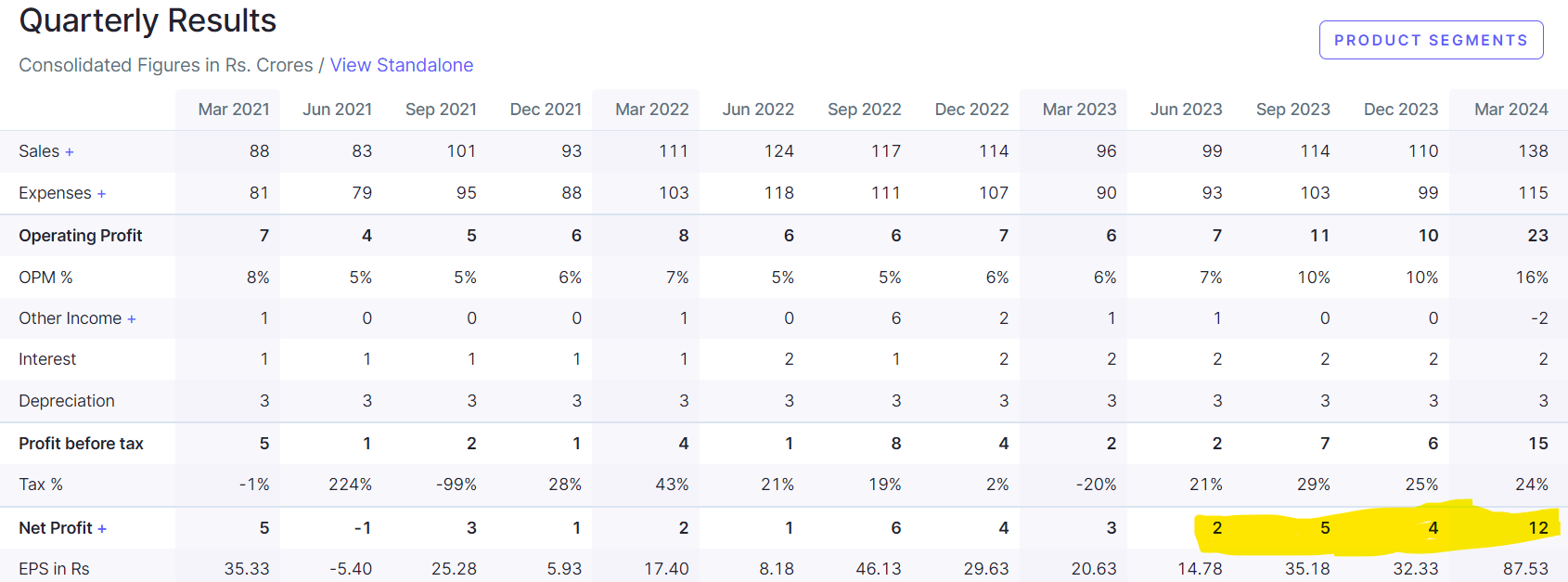

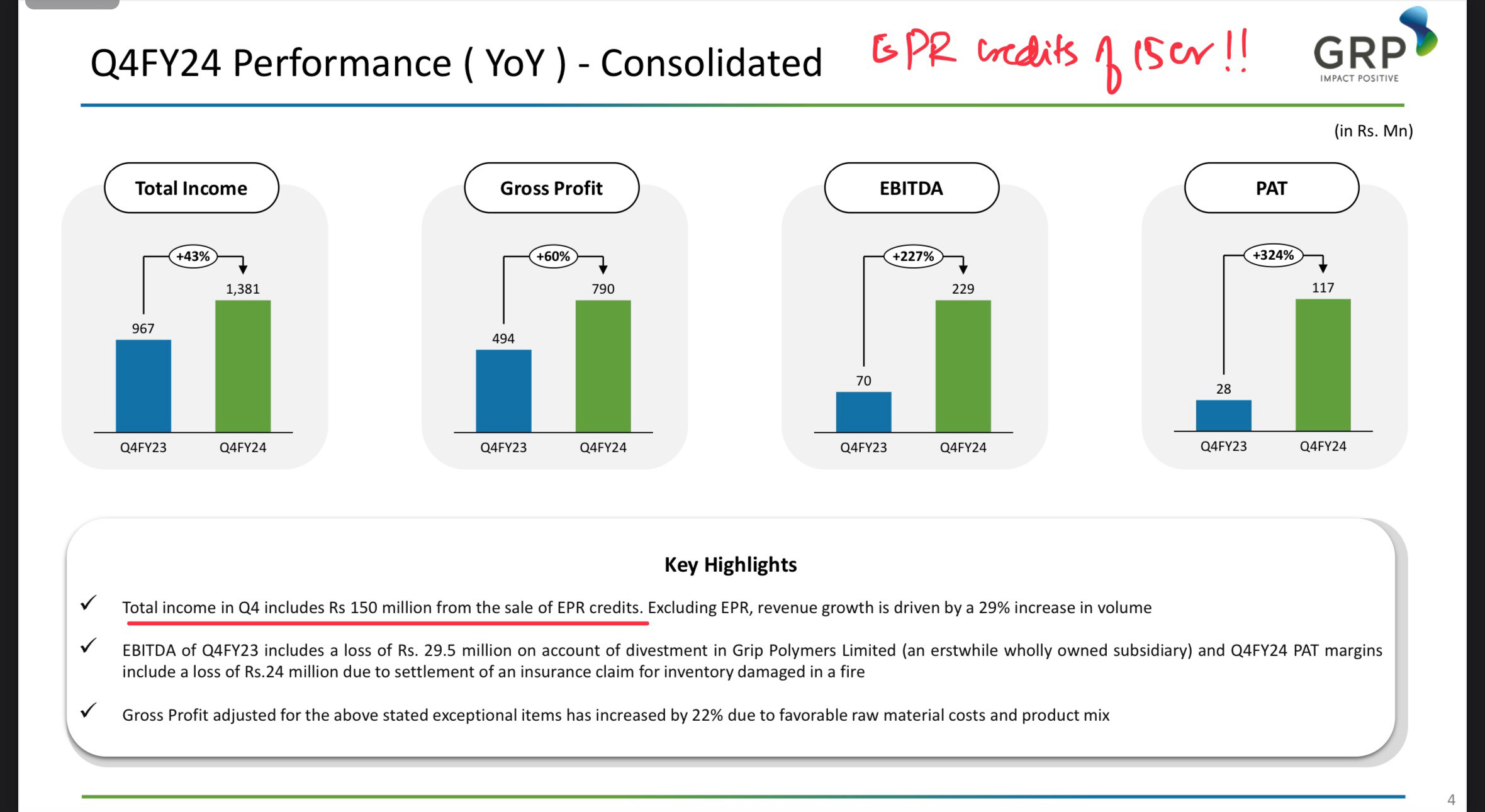

This stock delivered 3x of their usual PAT avg in Q4 . This is what piqued my interest.

.

Part of the reason for this bumper performance is due to EPR (Extended Producer Responsibility). I believe this has the potential to change the fortunes of this once loved now forgotten company.

Back of the Envelope Calculation on the EPR credits for GRP:

Current Capacity: 72000 MT

Capacity Utilization : 85%

Production : 60,000 MT

Q(EPR) = Q(P)x C(P) x W(P) = 60000x .78x 1.3 ~ 60000 certificates/ 600 certificates of 100 MT denomination.

In Q4 FY24 GRP has realised 15 Cr from EPR credits (As per management only partial credits realised for FY 22-23 ).

Assuming 60% of the credits are realised for FY 23 we can arrive at approx Rs 4000/MT as addnl realisation due to EPR credit .

The beauty of this is that this amount directly flows into the the EBITDA and boosting the margins as evident from Q4 .

P.S : Realisation for EPR credit is negotiated one on one with the tyre manufactures and this value is bound to vary depending on the demand and supply. However since GRP has several years long relationship with major tyre manufactures they have a natural advantage.

Brief Note on the company :

Concall Notes :

-

EPR for tyres started after 3 years of extensive work including the govt. /CPCB/ Tyre brands etc.

-

Partially realised EPR credits for FY 22-23 . Company has generated credits in CPCB portal for FY 22-23, 23-24 and 24-25 .

-

Global brand owners are also focused on the sustainability initiatives of the recyclers. GRP is the first Indian company to be certified for ISCC- " International Sustainability and Carbon certification "

-

100% subsidiary launched for repurpose Polyolefins business . Applications in paint and Lubricant sector.

-

Successful approval of Engineering plastics business by a European major , paving the way for entry into major auto OEMs.

-

Successfully commissioned new technology for manufacturing reclaimed rubber.

-

Additional land acquired in Sholapur for crumb rubber plant and venture into down stream recycling.

-

EPR regulations in plastics is getting delayed for implementation , expected in current FY.

-

New range of products in engineering plastics business from ocean plastics. Eg : Fish net waste.

Conclusion:

GRP is positioning itself not as a tyre recycler but as the most important cog in the circular economy .Their entire business is in the ESG domain. With the current tailwinds on environment, recycling etc and with introduction of EPR looks like good times are ahead.

Disc: Invested after Q4 results.

7 Likes

A Chat with Harsh Gandhi

1 Like