looking at the chart, I can’t find anything strange or interesting there. the stock has been in a steady uptrend. it does spike up whenever one wants to buy a few thousand shares due to nil liquidity and then comes straight back down after that and then resumes the steady upmove. most of the high volumes have been associated with up spike which indicates buying by strong hands. i personally don’t like taking positions in such stocks unless i have conviction to hold them for 3-5 years because any bad results or correction could turn nasty and may not give one a chance to exit. one caveat is that most good smallcap stocks owned by strong hands have very little liquidity. page ind even today with more than 3000 crs mktcap continues to be illiquid.

The reason is that one of the ex promoters Kothari has sold off almost 9 pecent stake. He has finished his selling just last week. Hence there was an over supply of selling orders on the already low capital base.

This plus the drop in both topline and bottom line has resulted in the drop in prices.

The management has come out with a clarification that the next quarters will be much better due to more customers and better environment in the European markets. Plus there is also the proposed reverse merger with HIM technoforge.

Hi Hrushikesh, any idea as to why Kothari has been selling his stake through open market sales and why not for example through a negotiated deal to other promoters or funds.

It will be good to understand the economics (margins/ROCE) of Him Technoforge. GAGL is a great business, run very efficiently, but will HIM Technoforge also be a similar business? Last I checked was margins for Him Technoforge were pretty average when compared to GAGL, maybe market has factored that in and thus the cheap valuations.

Its merger with Him TF is a must happen thing as the promoter has changed his stake too. Now this is getting huge orders from Europe and has a great product mix. I assume once Euro(currency) issues and the business model will settle down it will not trade below its Graham Number. Its a great value buy at these numbers. Not a potential multibagger but looks strong in giving RoC

Plz. come in on this one sir. I have done a fair bit of understanding and it feels a safe bet for technical reasons, fundamentally the above discussions are a place for you to start the deduction. I think its a big idea in export ancillary.

sorry, to hijack @suns, but it looks like gujarat auto has a corporate governance issue if you read the AR of the company. I would be very wary of this company.

True, I took note of that. I am however thinking its a one off and the company actually changed changed hands and registered office too. Its giving frequent guidance now. Their Europe business seems roaring and Make In India is going to benefit the new plant in Haryana

well, not sure but on what basis can we say it’s a one-off thing. Also, the amazing capital management was done by their previous owners. We are not sure if the present owners would be as good in capital management and ultimately capital management was the only thing that was giving such wonderful return ratios to the company…anyways, this is my own view …

True. I agree, but the holding of this prev. promoter was always in the same % as the new one and I see that slowly the new promoter actually had stake in this company for very long. HIM TF was owning shares of GAGL from enough long. Its mostly a shift in owning pattern but nothing else I guess, lets see this quarter results, they said its going to be great due to Euro fall and new orders.

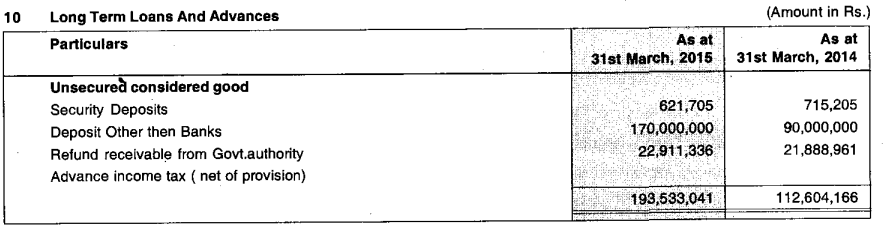

The company that has done EPS of 27 Rs, paid dividend of 0.70 Rs only. Majority of earnings are carried forward to balance sheet. Balance sheet Item of "long term loans and advances is about 19.3 Cr. Checking that item, an amount of 17 Cr is in the form of “Deposit other than banks”.so why does the company carry a huge amount of 17 Cr relative to its market cap of 35 Cr in the form of deposit other than banks?

from the time, last post was updated it has been a year and the share price has swung from INR 180 to INR 253. This is trading at PE multiple of 8.3 and PB multiple of 1.64 with market cap of 44Crores. the delivery %age has ranged in 60-70% range so far. Annual results are expected in late April or early May 2017. has any fellow valuepickr gotten chance to review this company in last 1 year?

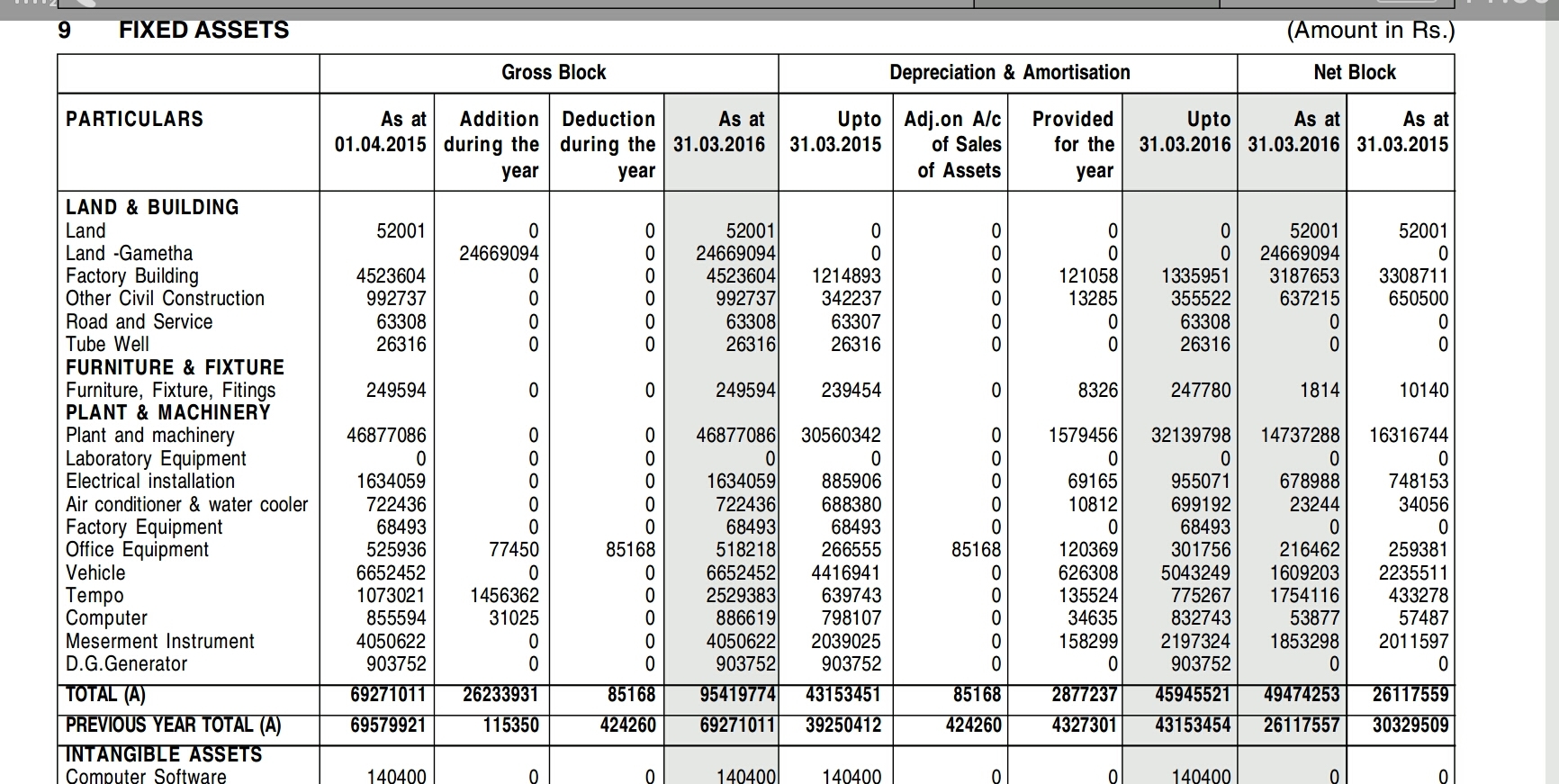

While analysing found from 2016 AR that there is a purchase of land worth around 2.46 crores , it seems to be an initial process for future expansion plan.