not a mistake. Ply business is good and flourishing… for MDF business there is stress and over-capacity, the valuation will be lower… price to book wise for MDF part.

Hi @zygo23554

You’ve been a long term investor in this stock. Would love to hear your opinion on the below points.

-

How do you see Greenply’s business compared to that of Centuryply?

-

Why did you choose Greenply over Centuryply?

I don’t see any stark difference in their margins or ROIC.

The rationale of Greenply to demerge their Plywood and MDF was to focus more on individual segments as the consumption shifts towards MDF from Plywood in-line with global trends. On the other hand, Centuryply, with all its segments under one umbrella, is in a better position to leverage its distribution network, branding, etc.

Except for the fact that Century is trading at a higher valuation than Green, I don’t see any reason to pick Green over Century.

Thanks for your contribution to this thread.

Greenply AR Key Points!

https://drive.google.com/open?id=1-6Kh-lUCqIqRTKkfQzm1gsazX9kZNN9B

Listing of its demerged entity Greenpanel from 23rd Oct, 2019! Seems to be a good investing opportunity!

(Disclaimer: Not an investment/trading recommendation)

Greenpanel Industries lists at around 500 Cr market cap, book value is 680 Cr so that presents an interesting situation.

One should expect the near term pricing pressure on avg MDF realization to persist for some more Q’s but as the company starts to sweat assets through higher utilization by selling in export market, the numbers at the EBITDA level should logically start to improve.

Unless the company is going to make losses for the next 3-4 Q’s market cap being below book value looks like an anomaly on the face of it. Also likely to see selling pressure in the first few days since a lot of people might want to exit.

Tracking Greenpanel Industries seriously here on, not decided on course of action. I hold Greenply since 2014 so automatically am an investor in Greenpanel after the demerger

3 Likes

so are you comfortable with the gradual fall in Greenpanel price currently?

Greenpanel results out (link)

One thing I don’t understand is when the PBT is negative then how come PAT is positive for previous years.

Also, financing costs have significantly come down. Any reasons for this?

Disclosure: Tracking

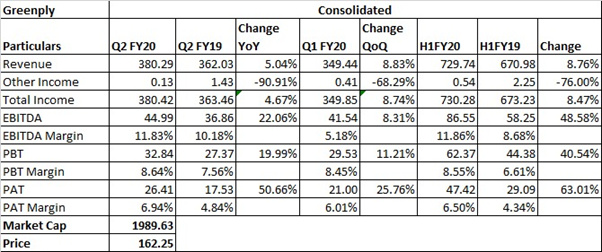

GreenPly Q1 Result Update!

https://drive.google.com/open?id=1jlzGQTjO__KI1iFml-zE5XWhBsaSqmjs

(Will Update Q2 soon)

Prepared by E-Global Group of Companies!

https://www.e-global.in/about-us/#Endeavour_Wealth_Management

(Disclaimer: Not an Investment/Trading Recommendation)

Kudos @zygo23554 ji, Your greenpanel future prediction (like ur HDFC AMC prediction regarding distributors fee) is turning out to exactly as you mentioned.

Exports increasing, gross margins coming down due to exports, capacity utilization going up due to domestic market growth, finance costs coming down due to $vsRs stability (?).

Management is targeting 62% capacity utilization in MDF for this year (according to presentation).

I read in some blog that the demerger is due to brothers dividing the business. Is it true?

Any insights on why IKEA is importing MDF despite logistics cost playing big role in MDF procurement cost?

Thanks in advance.

Discl: Invested in Green Panel after demerger (<5% of PF)

1 Like

Greenpanel new topic created as the company got listed recently.

Greenply Q2 Results!

Promoter holding has increased 0.67% in Q2 FY20 – a reflection of Promoter’s confidence in the strength and prospects of the Company.

Future:

- Yes, well, in quarter – in H2, we believe the market will further improve and a lot of the corrective actions that we have taken in Greenply regarding our better cycle and total of the center being under control. So I believe the H2 will be at least 8% to 10% growth we are expecting as compared to H2 last year.

- So we have likely started decorative business last year. So quarter-on-quarter, we are improving our sales in the decorative veneer. So if you see in the H1 FY '20, we have INR 55 crores of volume of value from the decorative business and our current year target was around volume [130 INR crores to 125 crores]. So that will give the additional growth. Apart from that, PVC and lower-end plywood. That will also contribute to the top line in the H2 FY '20.

Debt Levels: - That debt level compared to H1 last year has gone up but if you compare to Q1 – against Q1, in Q2 we have marginally reduced the debtor levels and this is mainly because of the cash flow and overall scenario in the market. And some – our production for the growth was also much higher because of a lot of tightening in the debtor cycle as to control over working capital cycle. We have kind of compromise on the growth also in H1. So we are working on various parameters to control this. I’m sure in the coming quarters, it will become much better.

- So if you see we have around INR 38 crores of long-term loans and balance of around INR 130 crores of short-term loan. So INR 38 crores will be pick up in the next 3 years. And working capital will remain in the business because as we grow, we require cash-free and other form of borrowings, with discounting and other borrowings. So long term, we will be paid off in next 3, 3.5 years.

Veener Business: So Gabon, in quarter 2, we had a top line of INR 35 crores and with an EBITDA margin of 17%. And EBITDA level profit was 3.5 crores. And this year, we have a target of INR 200 crores from Gabon business with EBITDA – blended EBITDA 18% from Gabon. That was 78 crores top line and EBITDA margin was 17.5% in H1 FY '20. So Gabon unit, we have a little bit – a little higher working capital cycle. So if you see on a consol level, particularly on Gabon, we have working capital cycle of 133 days. In Q2 FY – you can H1 FY '20. And these are 66 days and inventory days is 55 days.

Capex Plans: In India, we have a CapEx plan of INR 14 crores. Out of which, we already have INR 7 crores in H1. And then the balance will be in H2. And in Gabon, we have a proven CapEx of around INR 21 crores and we already have INR 13 crores in H1. Balance will be in Q3 and some will be normal maintenance CapEx in Gabon in Q4 because we already started the plant on 6th of November. So the balance CapEx will be in Q3 and some will be in Q4 out of INR 7.8 crores.

1 Like

Concall Highlights

A weak demand climate coupled with tight working capital control affected

sales during the quarter. GIL(Greenply Industries Limited) now expects its plywood business to grow at 4- 4.5% in FY20 vs. 8% earlier. Management noted that rising compliance (GST,

e-way bill) by the unorganised sector could aid some improvement ahead.

The company plans to draw down working capital days by 4-5 days by

end-FY20.

India plywood margins are guided to hold at current levels of ~11% in FY20 as

the company isn’t facing significant cost pressure.

GIL has two JVs in India each of which can deliver peak revenue of

Rs 1.1bn-1.15bn.

Gabon revenues were lower YoY in Q3FY20 due to reduced demand in India

amid the consumption slowdown. Also, a fall in face veneer prices in India as

Gurjan product prices declined resulted in some shift away from GIL’s okume,

which dampened sales during the quarter.

To diversify from face veneer sales concentration in India (from the Gabon

plant), management has been focusing on other markets such as Europe and

Southeast Asia. During the quarter, revenues from Europe stood at 13% (vs.

1% in Q3FY19) and from Southeast Asia at 27% (vs. 4%).

GIL now believes Gabon operations can deliver ~Rs 1.5bn of revenues in

FY20 (vs. Rs 2bn guided earlier) and maintain current margins of ~18%.

The JV in Myanmar should be PAT-neutral/positive by the end of FY20.

GIL has capex plans of Rs 160mn in India and Rs 220mn in Gabon during

FY20, of which ~Rs 270mn has already been spent.

Hi @zygo23554 ji,

If you can comment on my following observations, it would be helpful. Thanks in advance.

The price action of Greenply is bit perplexing. The Century ply whose major part of business is plywood has not fallen as badly as Greenply during the March massacre and also quickly recovered and reached 52 Week highs where as Greenply is still languishing lot closer to 52 week low than 52 week high. The Q1FY21 results are similar for both Century ply & Greenply. I listened to concalls of both Greenply & Century ply, and I did not find anything alarming specific to Greenply.

Although, I felt, the Century ply’s management to be dynamic & more upbeat. They also seem to be more innovative, which indicates their new “Virokill” ply and associated promotions. Century ply also seems to be implemented SAP hanna for better supply chain management. I am not sure whether Greenply has done same or not. Also, Centryply trying to tap into ecommerce as well is worthwhile try, which Greenply writes off as not much useful idea. We will come to know sooner how successful, these innovative moves from Century ply will prove to be.

Even though the demerger of businesses gives more focus for each individual businesses, keeping them under one roof would probably more helpful in terms of handling dealers, cost on employing more Sales people etc. Century ply might have some edge here having all the ply, laminate, MDF under one roof (this is just a theoretical assumption; have not done any financial comparison to back it up).

It seems to be a consensus agreement that covid crisis is speeding up the unorganized to organized thesis due to cash flow issues and bank’s reluctance to lend. This should help Greenply a lot for few more years despite the threat of market shifting from Ply wood to MDF as per global trends.

Greenply is trading at 3x Book Value/share compared to 3.6x Book Value/share (despite having capex heavy MDF division). If Greenply & Century ply able to get more favorable contract manufacturing opportunities, they can grow easily without employing much capital. Only threat to this thesis is market rapidly shifting to MDF from ply wood, probability of which is low.

I loved the Greenply ads which resemble the ads from Fevicol, which are great fun. My personal belief is in andhra pradesh, they have synonymous brand recall as much as Fevicol.

Disc: Not invested; Have not done any in-depth research into numbers; Evaluating for future investment; Invested in Greenpanel

1 Like

Looking at purely the numbers -

Centuryply trades at a market cap of 3,600 Cr. This entity has the plywood, laminate, MDF and CFS businesses all rolled into one.

Greenply trades at 1,050 Cr, Greenlam trades at 1,800 Cr and Greenpanel trades at 620 Cr.

With this context, the market is being uniformly bullish/bearish about both the leading ply makers. Just that one consolidated business with much steadier cash flows might be valued more than 3 small businesses where the balance sheet risk is assessed to be much higher. This appears to be bear market logic, which frankly is how the market is viewing most businesses that feed off construction and housing. This view might reverse doing good times, other than that I don’t see too much of a disconnect with the valuation across the two leading players.

Unorganized to organized shift appears to be happening for sure but it might take more for the market to get excited about the poster boys of the previous bull run. Many factors at play here.

I guess the more important variable one can keep tracking is the competitive position. As long as that does not weaken and the industry demand does not fall off a cliff, the players will get by with muted results till the cycle turns. All one can say with surety is that the cost structure by the end of the FY is likely to be much lower than it was prior to COVID-19.

A long term investing horizon with a value mindset is not for everyone, one needs to tread with caution in sectors which are out of the market’s fancy right now.

Disclosure: Tracking the sector, Greenply and Greenpanel are legacy investments in personal portfolio

1 Like

3 Likes

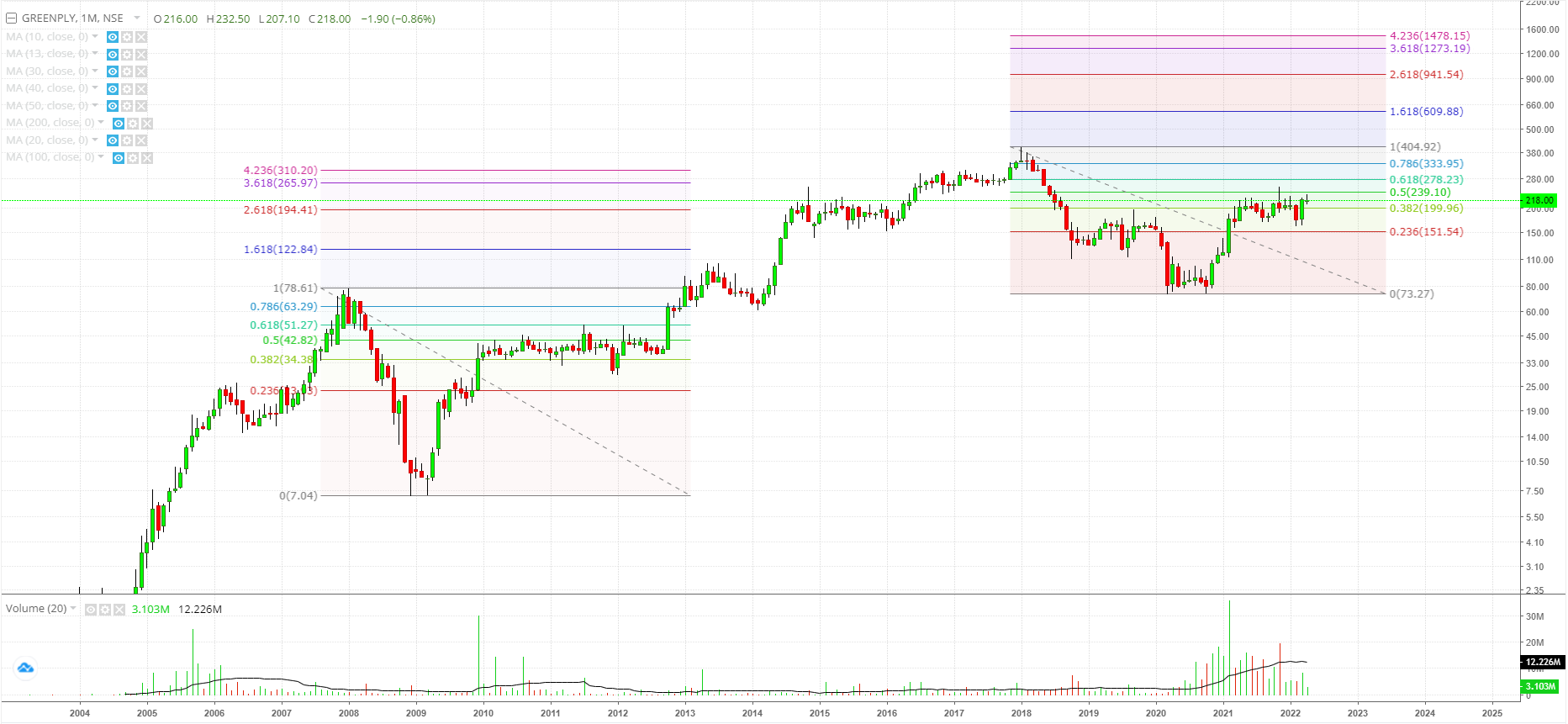

A Technical perspective on Greenply inds:

Monthly chart. Are we seeing similar setups (2008-2012 & 2018-2022) being formed (yellow regions) ? Fibo charts show similarity in consolidation phase between 0.382 and 0.618

1 Like

Can someone please help me with one question, Given that greenpanel was demerged from greenply in 2018 to have a separate entity for MDF business, why is greenply again entering into the MDF business now ? Am i missing something in here ?

1 Like

I guess MDF is the future. thats where growth will be faster. From a long term perspective, it makes sense for any Ply company to get into MDF. Geenply may be running as a independent company but opportunities for MDF are plenty. Plywood business may not grow as fast.

1 Like

both the companies are managed by brothers/relatives. demerger was done to give different pieces to different people and after a period of no-competition they are free to do all things: Plywood, Laminates, MDF

1 Like