Folks, who are tracking Greaves Cotton and E2W industry:

What is the current government stance on E2W subsidy? Government is investigating wrongdoings and stopped subsidy payout to the companies. What is the update here?

How Govt is thinking about EV scale up? Will they continue with subsidy or stop it? If they stop it, then what will be the impact on Ampere?

My Two cents :

Any Business that depends on government subsidies is not going to sustain. If not today govt will end the Fame Subsidy in immediate future. ( my guess it is on the cards). Greaves was not under gov’t scrutiny.

The battery prices are coming down drastically and the battery subsidy will be irrelevant and Greaves is not a discounting company , hence they pass it on to customers.

Govt Subsidy: They do not existing in vacuum. Many govt. have made some commitments on international forums to reduce it’s carbon footprint. Read, India’s COP26 commitment. Promoting faster adoption of EVs. is one of the ways to achieve this kind of target. We know that the subsidy can’t exist for eternity, but at the same time a whole gamut of things are inter-related with the subsidy. Our petrol import bill, environment concerns, we becoming self sufficient in this new technology and then export options etc etc…

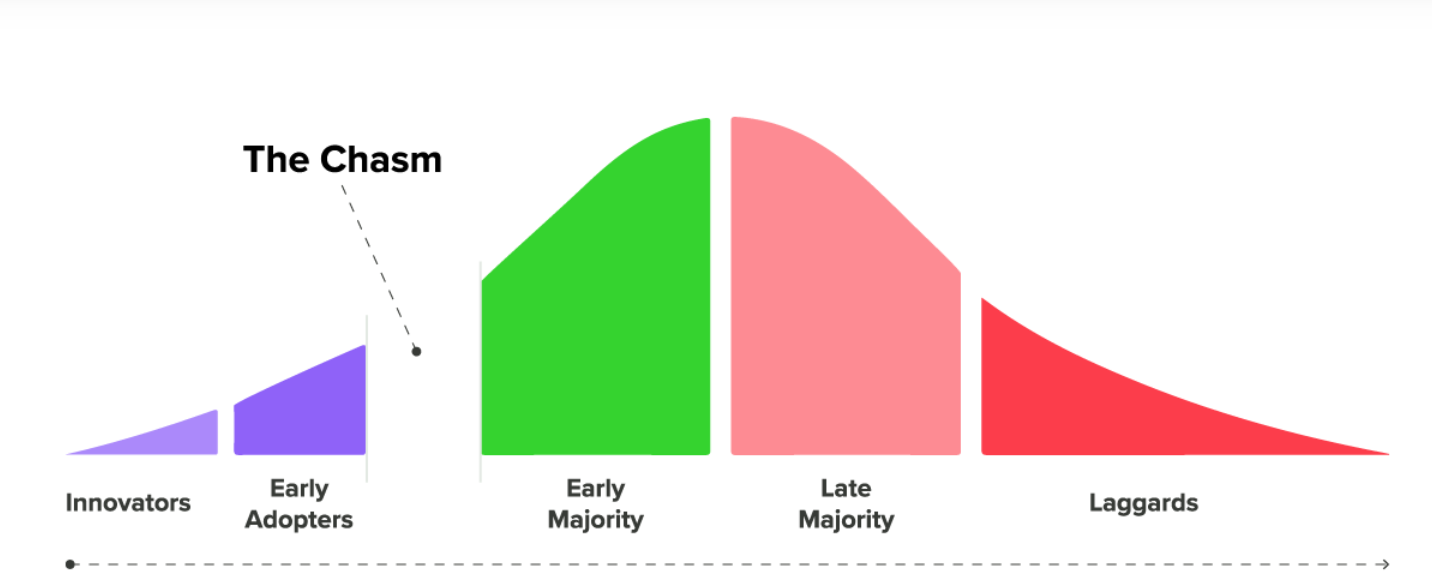

A new product category often goes through what is called as product adoption curve. Notice the chasm between early adopters and Early majority ? This chasm exists for a reason, because the early majority are pragmatic people who want proof that something really solves a purpose for the price they are paying. But early majority is where the real volumes are. A subsidy by reducing price a bit, encourages some in the early adopter & majority category to try the product.

There are question marks on the FAME II subsidy because of the lack of proper guidelines on how/what will be the process to check that those claiming the subsidy have indeed used 50% locally (by value) sourced components. Govt. has taken some action to streamline this by appointing some external agencies. There was an article yesterday implying Hero Electric and Okinawa have not met those criteria’s. (Hero Electric and Okinawa likely to get recovery notices over FAME-II subsidy: Report - BusinessToday)

On the other hand, some states are taking up the mantle of targeting faster adoption of EVs by offering ZERO MV tax and different other SOPS. Find the details of Odisha govt. initiatives here Odisha enhances subsidy on purchase of electric vehicles Odisha is targeting a 20% EV adoption by 2025.

I feel, at a certain level of adoption by early majority, the debate, if the industry is subsidy dependent will die. Because when subsidy stops, it will be a industry wide event. Each player will be equally impacted. I don’t think the wave of EV adoption will stop just because the bike will be costlier by 15-20%.

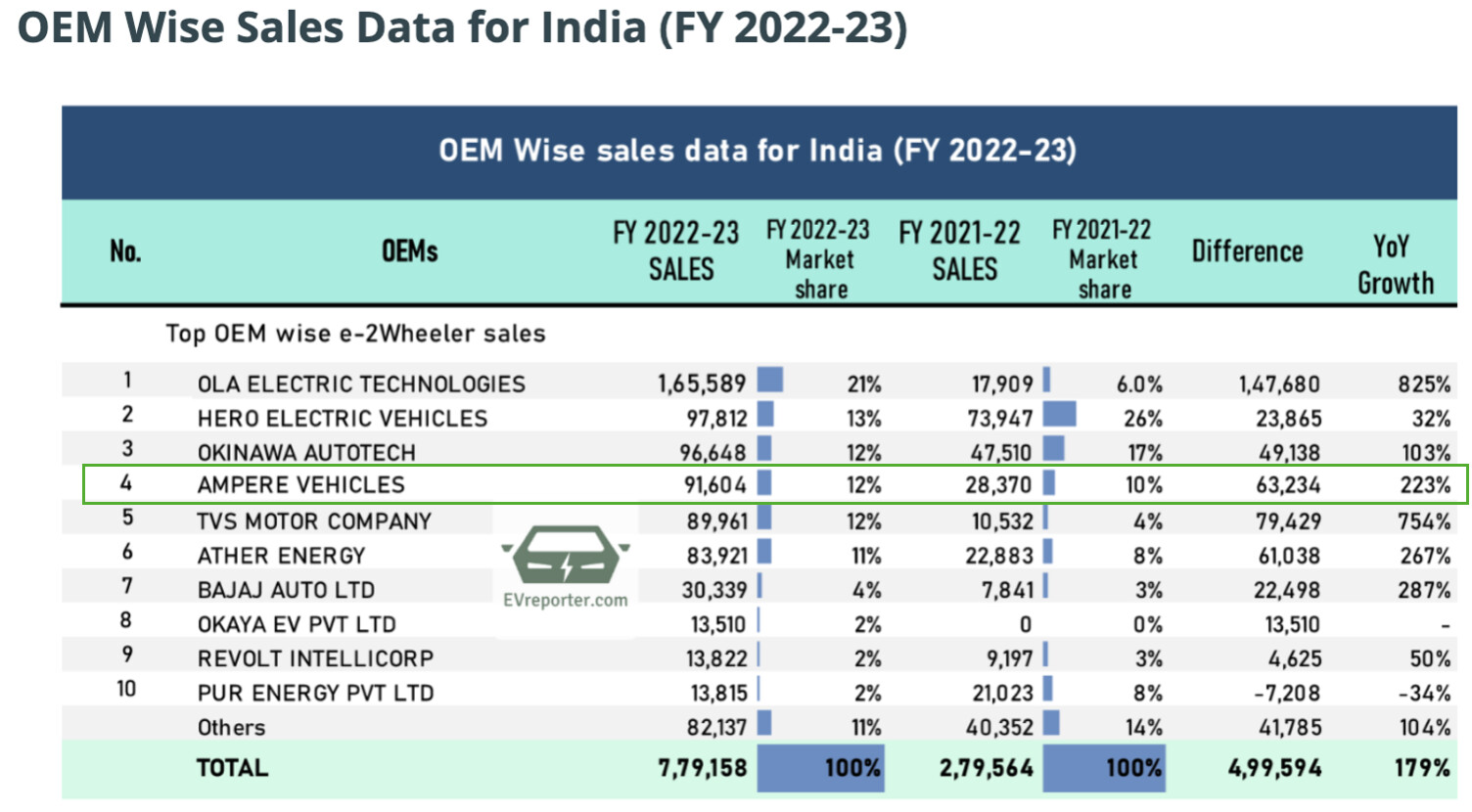

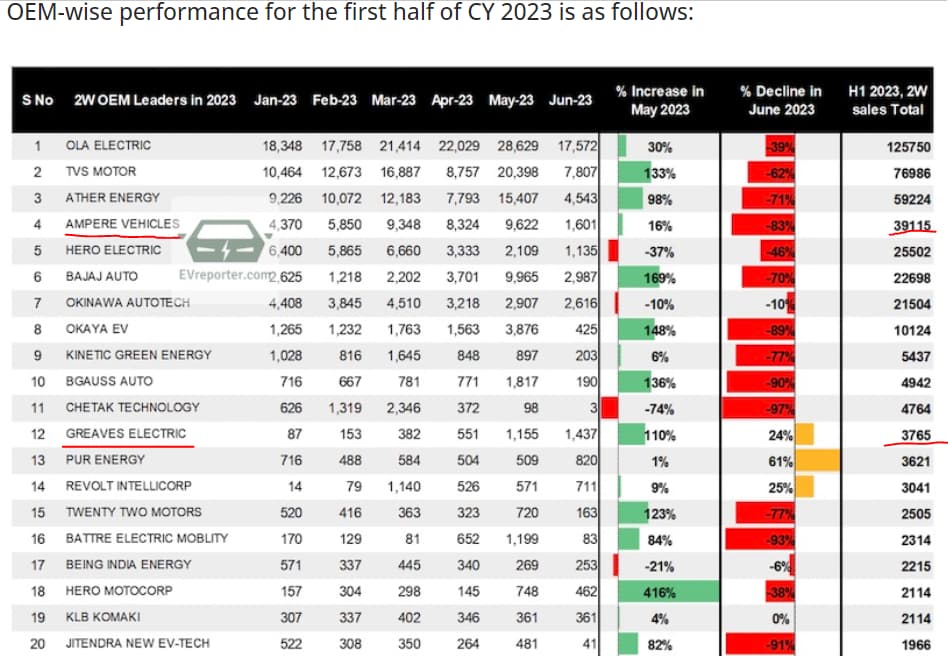

Meanwhile great news on Greaves secondary sales numbers in April. It has shot to 2nd position. I have no clue why TVS & Aether nos. (even hero electric) have fallen off the chart. Could it be related to the FAME-II issues ?

OLA ELECTRIC TECHNOLOGIES PVT LTD | April - 21579

AMPERE VEHICLES PRIVATE LIMITED | April - 8815

TVS MOTOR COMPANY LTD | April - 8722

ATHER ENERGY PVT LTD | April - 7681

Mahindra & Mahindra | April - 3690 (includes 4 wheeler??)

Bajaj Auto LTD | April - 3607

HERO ELECTRIC VEHICLES PVT. LTD | April - 3287

OKINAWA AUTOTECH PVT LTD | April - 3127

YC Electric Vehicle | April - 2773

Dilli Electric Auto Pvt. LTD | April - 1717

Okaya EV Pvt Ltd | April - 1508

Piaggio - 1405

Saera Electric Auto Pvt Ltd | April - 1819

kinetic Green Energy | April - 1170

Mini Metro EV | April - 1006

(Listed all the players with higher than 1k vehicle sales in EV in April)

Expecting a bumper set of numbers from Greaves. Lets see if they can cross the 800 cr. revenue mark at consol. level and EBITDA positive at EV level.

3 major players (ola,Okinawa, hero) impacted if we are to believe this report.

Seems like finally some clarity on the FAME-II subsidy may be emerging. No mention of ampere to be on defaulting company list.

Hi Everyone !

Does anyone have any views on the recent resignation by the CFO? It seems, company’s top officials exiting is a regular with this company. Although, top results seem to improve quarter by quarter but KMP exits is a concern. Any views?

Relevant snippet from the Q3Fy23 concall - Vahan Portal gives you data of the registered vehicles. Obviously there are certain anomalies in the sense of time gap, because from the time the vehicles are actually sold to the customer and till the time it is registered to that extent the Vahan database updating take gets delayed.

Transforming from traditional (stagnant growth) engines and auxiliary power systems business to fuel agnostic powertrain, electric vehicles (2W, 3W), aftermarket spares & retail solutions.

Business owns 6 manufacturing locations and is supported by auto aftermarket network with 8000+ retail outlets, 20000+ mechanics and 350+ dealer touch points.

Key products/services:

Automotive Engines: Diesel & CNG engines for 3W and small 4W.

Non-Automotive: Farm Equipment (Portable Engines, Portable Pump sets, Power Tiller, Reaper, Rotavator), Portable Gensets 5 to 7.5 KVA and Industrial Gensets 10 KVA to 1250 KVA, and Industrial Engines.

Retail outlets: One stop shop for Sales, Service & Spares (3S). Consists of AutoEVMART, Greaves * Care and Greaves retail.

AutoEVMART: National multi-brand EV retail. 150 Stores.

Greaves Care: Multi-Brand service. Service and Spares of the major brand for 3W, commercial and passenger vehicles. 170 Stores.

Greaves Retail: Spares Sellers. 8000+ stores.

Greaves Electric Mobility (GEM): Manufacturing and Selling of Electric 2W & 3W. Ampere (E-scooters), ELE (E-Rickshaw), & Teja (E-Auto). EV manufacturing facility and an Experience Centre at Ranipet, TN. Acquired Ampere brand in FY20. Ampere ranked amongst India’s top three electric vehicle manufacturers in FY23.

Greaves Finance: Finance options to electric vehicle buyers.

What’s Interesting?

In 2017, business-initiated steps to establish itself as a leading fuel agnostic powertrain solutions & services company, recognizing electric vehicles as an upcoming large opportunity.

Past revenue used to be 100% B2B. However, 66% revenue of Q4FY23 66% came from B2C. This shall lead to overall margin expansion once GEM division attains scale.

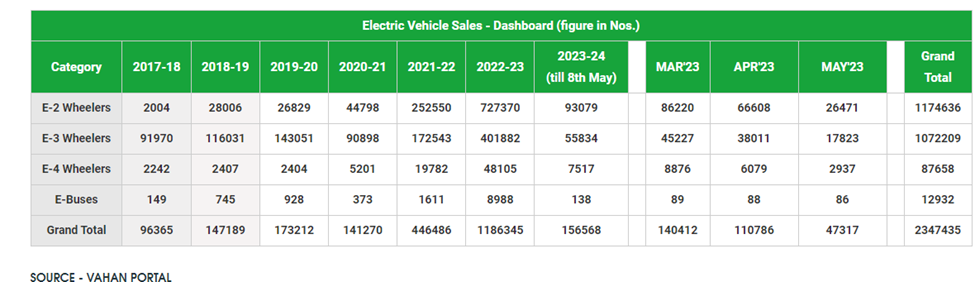

The significant growth opportunities for E-Mobility businesses considering governments push for EV adoption. Below snapshot shows the trend of the last few years:

How I expect numbers to trend?

As a base case, I expect that consolidated margins would double from current 5% and Sales, EBITDA & PAT would grow at CAGR of 19%, 33% and 39% respectively for the next 5 years as the business would earn most of the revenue from B2C channels, which will scale up with time due to huge opportunity and sectoral tailwinds. It will be great to hear counter views from far reaching minds on this aspect.

(Details are shown below).

Revenue

FY23

FY24(E)

FY25(E)

FY26(E)

FY27(E)

FY28(E)

Exp. CAGR

Engines

1015

1015

1015

1015

1015

1015

0%

Retail Spares+Care+Evmart

535

589

647

712

783

862

10%

Excel Controlinkage

-

200

220

242

266

293

10%

Electric Mobility

1124

1461

1900

2469

3210

4173

30%

Consolidated

2674

3265

3782

4439

5275

6343

19%

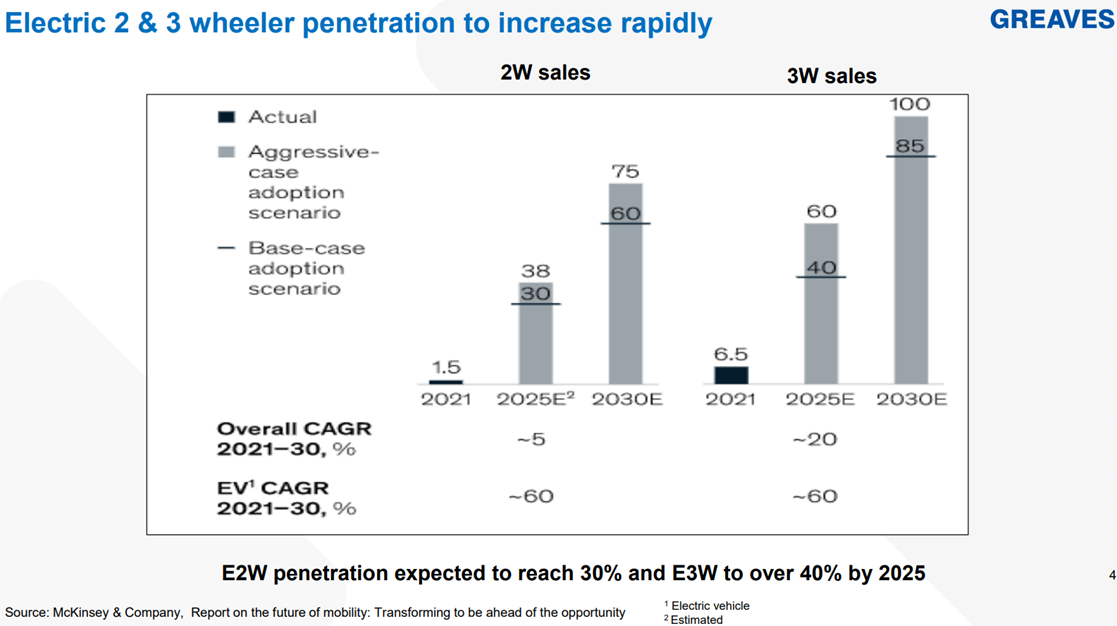

If assumed CAGR of 30% under ‘Electric Mobility’ materializes, business would sell 3.7 Lacs vehicles from their current production capacity of 5 lacs. On conservative basis, I assumed that ‘Electric Mobility’ sales for Industry and Greaves would grow at the rate of 30% over the next 5 years. With this assumption, Expected EV Penetration in 2W mkt. would be less than 30% by 2030 although Mckinsey’s base case (in below slide @ https://www.bseindia.com/xml-data/corpfiling/AttachHis/62d1739b-df19-4484-8a04-8f6fd37c9fb9.pdf) pegs it at 60%:

Diesel parts business may remain stagnant or decline.

New entrant in 2W and 3W industry as an OEM.

Recurrent Executive Directors and CFO churn.

EV manufacturers are yet to breakeven at operating level. To maintain level playing field with the competition, margins of the GEM division would remain under pressure in the near term.

Valuation:

Considering all the above data, business looks overvalued on the basis of PE and EV/EBITDA compared to industry stalwarts (Bajaj Auto and Hero MotoCorp) in the near term (horizon of < 2 Yrs.) even though it does not carry the burden of phasing out ICE portfolio. Going forward, the key trigger for me to change my opinion would be better than expected Growth Rates and Margin Improvement in the ‘Electric Mobility and Retail’ division. 16May2023: Most players in the EV space are still loosing money at the operating level even with government subsidy in place. Hence, I think that industry stalwarts like Bajaj Auto are moving at slower pace in the EV space, avoiding dilution of their existing OPMs.

In turn, players such as Greaves Electric Mobility (GEM) will have ample opportunity to growth for the next 5 Yrs. It would be interesting to monitor that at what pace GEMs expenses (and OPM) move closer to that of Bajaj’s.

Indian Govt has demanded clawback of a subsidy amount of approximately Rs 124 crore along with interest for violations of Phased Manufacturing Programme (PMP) guidelines from Greaves Electric Mobility Private Ltd (GEMPL)

what a jump in 2W EV nos. for most players in May. Was the market buying them in anticipation of the FAME withdrawal ? Top 5 composition has changed, but they all had good MoM growth.

Greaves Cotton Ltd, an engine maker in India, is experiencing significant revenue growth driven by its electric mobility division, which includes the Ampere brand of electric two-wheelers. In the fiscal year 2022-23 (FY23), the electric mobility division contributed 42% to the company’s revenue, surpassing its core internal combustion engine business. The division’s contribution increased further in the March quarter, reaching over 46% of the company’s revenue. To maintain profitable growth, Greaves Cotton is diversifying its business by expanding its traditional internal combustion (IC) components and non-automotive businesses.

Greaves Electric Mobility (GEM), which owns the Ampere brand, played a key role in the company’s revenue growth, with its revenue contribution reaching its highest ever. Additionally, Greaves Cotton is expanding its auto businesses through a 60% acquisition of Excel Control Linkages, an Original Equipment Manufacturer (OEM) specializing in push-pull cables, motion sensors, and controls. The company has also partnered with UK firm Eta Green Power to manufacture electric powertrain solutions, such as battery packs, electric motors, and battery management systems (BMS).

While the newer businesses, particularly electric mobility, are expected to grow faster at the top-line level, there may be bottom-line pressures due to the investment phase of the e-mobility industry. Greaves Cotton acknowledges that the traditional IC engine business is evolving and transforming, and will continue to grow, albeit at a slower rate. The company aims for sustainable profitability in the medium to long term, anticipating growth in both the top line and bottom line.

Despite the success of its Ampere brand, Greaves Cotton is facing allegations of violating localization norms under the government’s FAME-II scheme for electric vehicle (EV) incentives. The government has sent a notice to recover subsidies amounting to ₹127 crore, while around ₹300 crore remains pending.

Greaves Cotton is also focusing on high-margin components, with the acquisition of Excel Control Linkages expected to improve group margins. The company’s strategy to increase the share of e-mobility and new initiatives aims to drive long-term growth and transform and de-risk its business. Consolidation of manufacturing operations into Megasites is expected to bring operational efficiencies and reduced fixed costs in the long run.

The company believes that subsidies for electric vehicles should continue until EV penetration reaches a double-digit figure in the automobile market. They consider the current market penetration of 5% for electric two-wheelers in India as nascent, and subsidies act as a catalyst to boost customer confidence and offset the higher upfront cost of batteries compared to internal combustion engines. However, they recognize that long-term subsidies are not a sustainable solution for the country.

Can someone please help me with this. According to yesterdays press release they crossed cumulative 100,000 units of 2 wheelers in FY23 and now in 1st quarters crossed cumulative 200,000 units, so they sold 100,000 april-june ?? Did I read something wrong ?

Primarily it’s case of Huge opportunity, if they will succeed then it will. Be multibagger .

Warren Buffett had invested in such cases many time. I hope not comparing to orange .

There is lot of buzz due to stock marketing agent Shri Vijay Kedia ji, on Atul auto. See they have not even launched any EV . And valuation almost doubled after announcing story. At same time Greaves had done tremendous job , they have rolled out the story almost. And the stock is getting dipper and dipper.

That’s the fantasy of stock market.

Few questions

what about EV motor and bettery? They have any collaboration? Like Atul had .

or they developed their own BMS ,EV MOTOR, BETTERY AND CHARGING INFRASTRUCTURE.?

Net Sales for June 2023: Rs. 568.59 crore (down 13.87% from June 2022)

Quarterly Net Loss for June 2023: Rs. 5.08 crore (down 131.61% from June 2022)

EBITDA for June 2023: Rs. 8.00 crore (down 83.66% from June 2022)

Stock Performance: Greaves Cotton shares closed at 139.75 on August 09, 2023 (NSE), with a 0.43% return over the last 6 months and -14.05% return over the last 12 months.

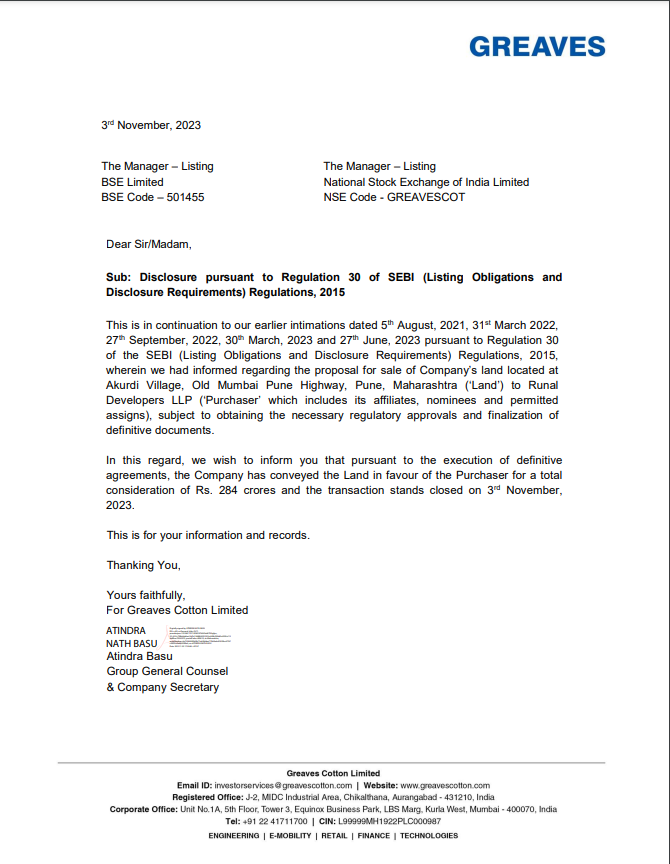

Greaves Cotton has successfully sold a piece of land in Pune for Rs. 284 crores to Runal Developers LLP after obtaining the necessary approvals and completing the required legal procedures.