I think the past 2 days have been a good lesson regards holding good businesses rather than holding stocks. Selling due to technical/short term reasons almost never makes sense when investing in a good business. In the short term selling and buying could be due to any number of reasons including Noise traders/RSI overbought or oversold etc. The main questions that should be asked and monitored are

-

Do you trust the promoters:

Imo Krishna Prasad has been a fantastic promoter and apart from maybe being too overexcited about his business prospects during the covid period he hasn’t really put a foot wrong. The succession issues seem sorted now considering he has laid out a plan uptil FY 24 or so and his daughter is now on board. Their numbers all look real and balance sheet looks clean. -

Has capital been allocated correctly?

The products they launch and the capex directed for the same has led to healthy returns on their capital employed and stayed respectable even through the downturn last few years. Infact they were one of the few companies that handled the downturn well -

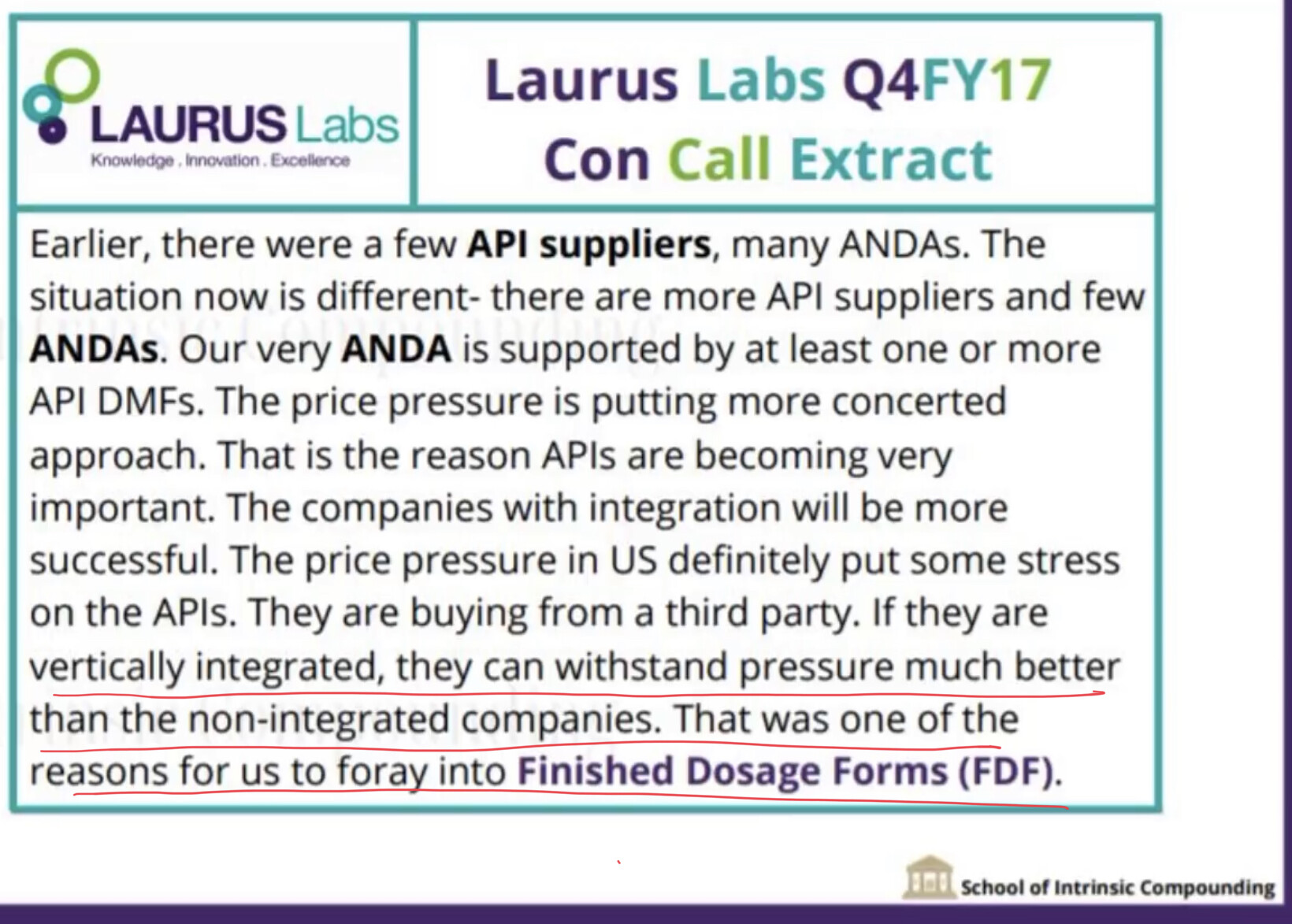

Their moat:

Management has repeatedly said that they should be looked at as a manufacturing company and that’s playing out via their operating margins. They’ve slowly but surely improved over the past few years and finally they are above 25 percent and look sustainable. Dependability on China will reduce in a few years too so expect less volatility in margins. -

Long term plan:

There was not much visibility regards this earlier. However, now we know about MUPS and their capex until FY 24. We also know that they are experimenting with crams which leaves the door open to it in a few years if they desperately need a new source of growth(which they don’t need right now)

If the above factors break down over a couple of quarters and not due to short term one off reasons ie promoters integrity/operating margins collapse/bad capital allocation/Long term plan turns for the worse/Regulatory issues prop up and granules fail/… then maybe selling makes sense.

However, for now the overall bull market has spoilt us. Getting a business with 25 or so percent PAT increase YoY for the next couple of years with improving financial metrics and a long term plan with a history of good execution under ethical promoters in a sector with tailwinds is a goldmine

Disc: invested at various levels and added more during the dip around 320 too. My 3rd major pharma holding after Laurus and Alembic. Not a sebi advisor