EPS growth guided by management is enough to cover PE of 12 till FY22. Although I don’t wish to get into PE debate as this is not a metric for me to monitor my investments but considering topline / bottomline growth projected by management and the product pipeline visible through FDA approvals, I don’t see PE shrinking to such a low level.

Although management is guiding and we expect them to walk the talk, one concern raised by them is impact of covid till next quarter end. The impact is mainly on transportation & availability of containers etc. The vaccines are available and vaccinations have started in US / UK and other countries, we expect such concerns should not have visible meaningful impact on topline / bottomline.

@pumba22

Granules is currently very well placed and I can’t see a derating to 12/17. I don’t want to comment on what I see the re rating being since that is upto Mr market… but imagine this… a company usually goes along this cycle… 1. Using debt/pledging in the early years to grow quickly and compete 2. If stage 1 goes well then slowly reduce dependence on pledging/debt. 3. If stage 2 goes well start handling capex via internal accruals 4. If stage 4 goes well and tailwinds are in favour and the right capex decisions were made then the profits come in and then slowly a company ends up in positive fcf.

Granules is currently hovering near stage 3 wherein their debt is manageable, pledge has reduced significantly and internal accruals have begun. If the guidance is correct they’ll be setting a huge base next few years via 70 percent and then 30 percent increases in profit. Margins are improving and approvals look a lot more likely as compared to a few years ago. With all of the above, cash will keep on coming in and we LL be cashflow positive over the next few years if the pharma cycle continues moving upwards after its downcycle. So imo all the signs are there and the triggers are aplenty. I believe the market is just waiting to see if Granules and pharma companies in general can actually walk the talk and manage the figures they speak of next few quarters since there’s some disbelief regards the huge profit guidance given by most pharma companies and if they can actually manage it. Again, who knows when a pe rerating will come but currently the odds look stacked in our favour over the next few years. Rather than talk about pe ratings though let’s wait for the quarter results and commentary which is scheduled for 28th January . Cheers

I have been watching some of the recent chats but I want the members to look from one more angle — recently the big PE firm Carlyle was almost ready to buy stake in Granuels India but the deal could not materialise. This itself shows the strength of the Company and future prospects one can see in short time.

Interest by PE firms doesn’t means success gurrenteed. If Carlyle are successful in all their acquisition, they should be in bigger size than Berkshire Hathaway

There are news that promoters want to sell their stake and get out. The price correction has nothing to do with fundamentals. The fundamentals remain strong and valid.

Good information

3 important points from this I observed are -

Entry in Europe

Target of Billion Dollar Company

The commercialisation plan of some of units is ready, resulting in various new product filings and validations and triggering a regulatory inspection,”

Just went through the concall of previous quarter and investor presentation to try and make forecasts for the next quarters as per management guidance. Their guidance for next 6 quarters or so is basically laid out(70 percent and 25 to 30 percent) but was surprised to find that via their presentations and concall you can basically cover uptil FY 23:

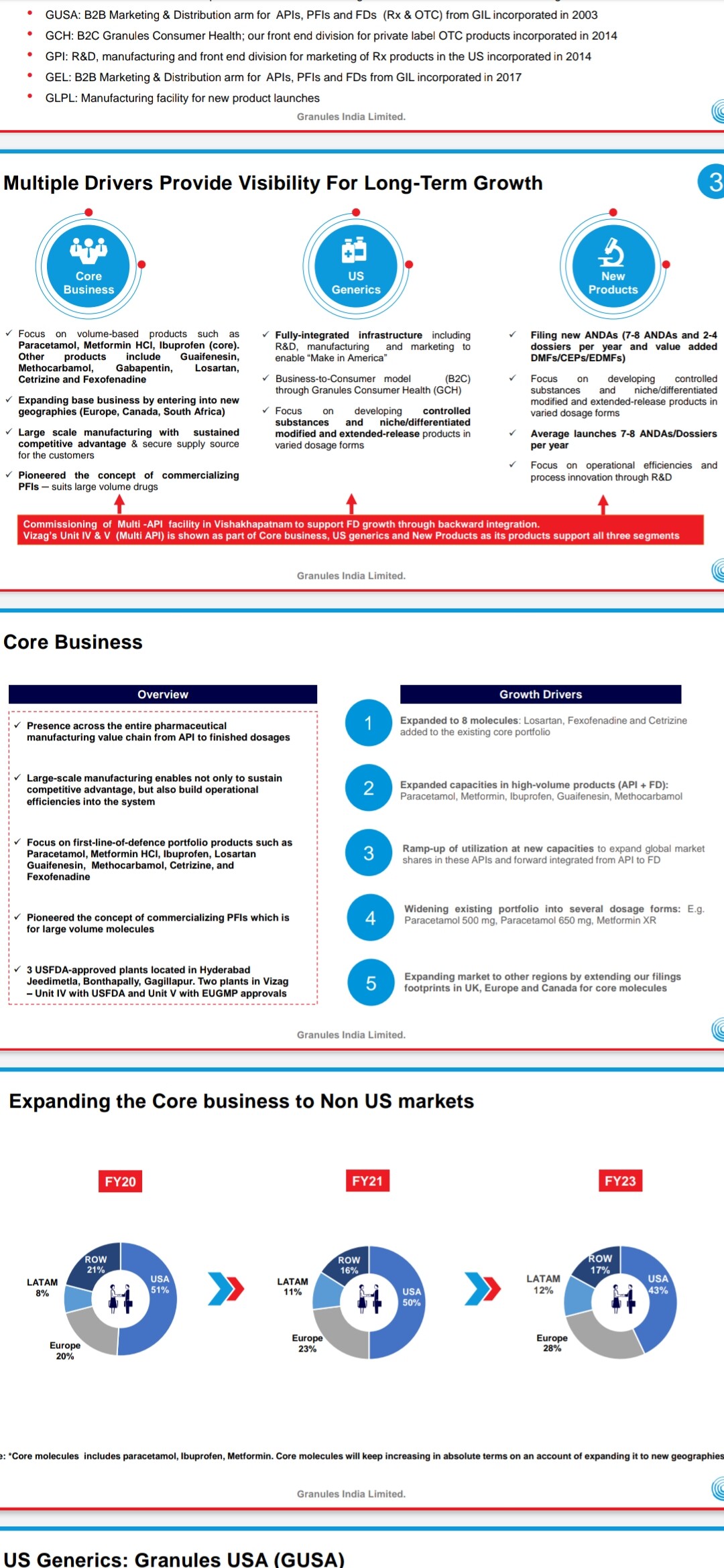

For FY 20 Europe contributed 500 crores ie 20 percent of the revenue. For FY 23… as per concall… Europe will be around 1500 crores. As per investor presentation it should cover approx 28 percent of the revenue. This means overall revenue for FY 23 will be around 5500 crore.

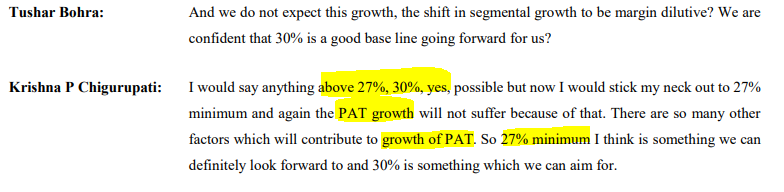

EBITDA margins they are aiming to hit a minimum of 27 though they are hoping to keep 30 as the standard. This means that EBITDA should be in the region of 1500 to 1600 crores (current ttm EBITDA is 864 crores) and PAT of 900 cr to 1000 cr which means an Annual EPS of above 2x current EPS(currently 17.4)

Note: This is just management guidance and obviously isn’t an exact science but is a good measure to see if management can pull it off/go over/under their targets since this is what they are expecting.

Our aim should be to track each quarter to ensure management can walk the talk(europe, margins, mups, new geographies, new products, pricing pressures, overall pharma cycle, sales and pat etc) and can hit these lofty targets starting with the current quarter(result out tmrw)

From Q2 concall:

“Q2 sales - 858 cr vs 700 cr YoY, Gross Margins at 58 pc vs 49 pc YoY due greater share of FDFs, EBITDA margins at 30 pc vs 20 pc, PAT at 164 cr vs 96 cr YoY. Company confident of maintaining atleast 27 pc EBITDA margins going fwd with an aim to keep clocking 30 pc.”

Depreciation was around 30 crores for Q2 so they did manage 253/858 = approx 30 percent ebitda margins. So taken the revised guidance from Q2 concall and not Q1. Guidance has been fluctuating in the short term though so keeping an eye on FY 23 using what they’ve said so far and will adjust as and when things change. There is an error in my post above though: TTM ebitda is 148 more due to depreciation so it’s not 716 but 864 crores currently(editing above)

In the first 10 mins in the concall management spoke about ebitda margins increasing to 30 percent(before adjustments) and explained in detail why but I can’t remember anything about sustainability either.

Post the concall months ago I saved the summary linked above in this forum in my concall notes so took it as gospel. Anyway, luckily we have one more result tmrw so we ll know if EBITDA declines or stays the same.

The investor presentation is the source for 28 percent Europe by FY 23 and the concall does mention 1400 to 1500 crores(double checked) so apart from EBITDA margins the rest looks ok

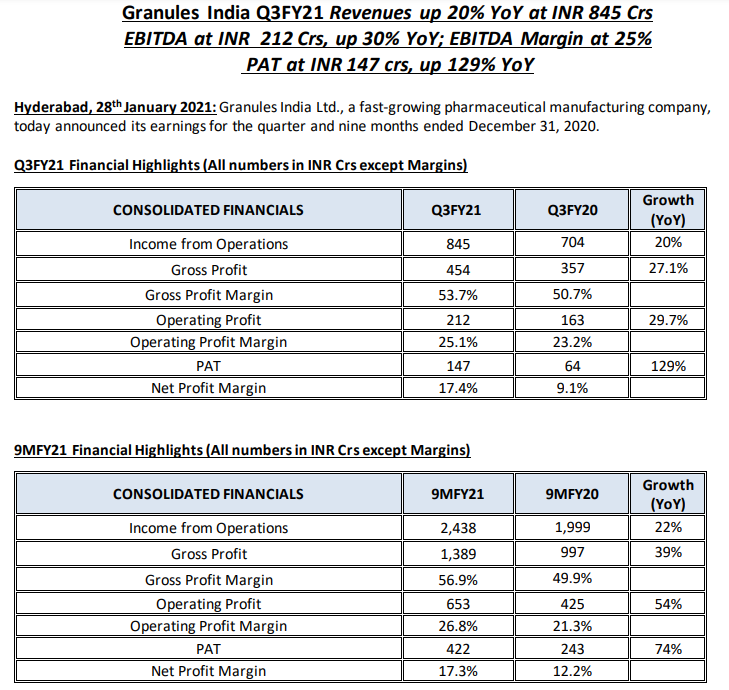

Pretty happy about the result prima facie and eagerly waiting for concall. It’s totally as per guidance imo.

Management said FY 21 would be 80 percent of FY 20 and later said 70 percent. Considering FY 20 was 309 crores they needed to hit 525 to 556 crores for FY 21 to match their guidance.

They’ve now got 422 crores over 9 months.

Considering management confirmed via interview post Q1 that they would beat Q1 in every quarter this year you can expect a minimum of 112 crores in Q4 which would put them at 534 crores for FY 21(though they should get more). EBITDA margins of 25 percent confirm 30 wasn’t sustainable though. All things considered results are very much in line.

Last quarter had a one off 7 crore profit too so this isn’t much of drop QoQ either.

Disc: invested

Visibility regards growth now looks fantastic(from investor presentation)

Medium term growth driver:

MUPS:

• GIL will invest INR 2,400 Mn over FY21 to FY22; to be funded entirely via internal accruals

• The products that will be manufactured in this block will be integrated with APIs from the Multi API block from Unit 5 in Vizag

• The MUPS block will have a capacity to manufacture 2.5 – 5 Bn FDs per annum will be operational by Q3FY22

• Received approval for one product in FY21. This product is under production in an existing facility and will be launched in Q1FY22

Long term growth driver:

During the quarter, we acquired land in Genome valley for the construction of a PFI & FD manufacturing facility for ~10 Bn units of solid

orals, other finished dosage forms and additional capacity for PFIs. The facility will be operational in early FY24. The expected CAPEX is

~INR 4000 Mn, to be incurred over the next 3 years(concall should give more info regards how they’ll handle this)

Challenge for the current quarters

- Supply chain.

- Increase in raw material cost.

- Foresee more supply chain destruction.

- MEIS, incentive withdrawal scheme, has impacted.

Expecting a major launch of MUPS based products. Expected a few other MUPS based products.

-QOQ-Degrowth due to logistic issues and MEIS incentives.

Yet to launch 10 products. Expecting 1 or 2 approval this quarters. Will be launching 1 or 2 in current quarters.

ANDA acquisitions:

Raw material price hike- Historically, GI has passed on most of the price hike to the customer. They shall be able to pass on the current raw material price by Q1- FY22

Focus on EBIT- Long term goal aim is towards 27%.

Cost of Genome Valley- Cost of Land 28 cr. Capex will be 400cr

-CAPEX - Total 21-22- 300- 400cr.

CAPEX 800 cr total up to FY 22/23(?).

Inventory increase due to the launch of new MUPS based product. GPI build 4 months inventory for new product launch.

No PE deal now or in long future also.

NO revenue lost - Disruption of raw material supply resulted in destruction in production, but no revenue loss

-Global Supply change destruction. Normally it takes 18 days for a container from China to India. Now it taking around 45 days. It has resulted in compression in margins.

GPI (US) is not suffering from logistic and supply-chain related issues.

R&D- impacted due to Covid.

PAT growth expectations for FY 21 60-70%.

80% of US revenue from RX and 20% OTC products.

15 Products Approves Granules India- All products launched.

GPI- 6 launched and 15 approved. (Not sure why so many products are waiting for launch after approvals).

Metformin all products are in the US. However, from this quarter some of it going to Europe and other parts of the world.

Core Molecule contribution around 85%. Last quarter is was same (wrong info provided last time).

-Capacity Utilisation- More or less full. Other than Multi API (20% capacity).

Dependence on China will reduce in the next 1.5 year (I guess for some of the products) as we have signed contract locally.

Note- As I took notes during the call. Some of the things may be unclear or incorrect due to call quality. Please feel free to correct.

Management has started reducing their own guidance,

PAT growth for current FY was projected as 70-80% has tuned down to 60-70%…

PAT growth for next FY was projected as 30% has tuned down to 25-30%…

We see similar approach in EBITDA

The stock had seen much action due to interest of PE fund houses, which is no more (atleast for near future - management has moved from “No Comments” to “No Discussion”)

Is the stock loosing its long term moat where market is presenting better opportunities even in Pharma sector

60 to 70% YoY PAT - isn’t that still great? Yes I agree management should not over promise and under deliver. I think this kind of results would have been fantastic, if management had guided only for 50% PAT growth over previous year. Also, why the company would loose long term moat just because management guidance was missed. I think with Chairman’s daughter onboard, succession issues are atleast over for next few years. In last 10 years, granules sales grew at a rate of 19% which is fantastic. This is a capital intensive business and doesn’t leave much of cash. Valuation wise the stock is reasonably valued so downside looks limited. Can company sustain 18 to 20% of revenue growth in next 5 years?