Now that price is almost 8% higher than buy back price, can the promoter sell in the open market t realize better price

I don’t think promoters wants to reduce their stake. This rise in price is a bummer for them because in the buyback scenario, they could have kept their stake in the company intact and reduce their pledge simultaneously. To be honest with you, the promoters were taking money from the company to save their skin with this buyback. Let’s see now how the situation unfolds.

Kanv

Disc. Have a trading position

1 Like

That would send a negative impression and the promoters will never do it.

As far as I see it the current scenario is very much ideal for the promoters for reduction of pledge. As the market price is at significant premium to buyback price there will be very little shares tendered by other categories of investors other than promoters which will make them enable for tendering maximum amount. I believe this could be one of the reasons why they had delayed the buyback offer a little. In fact the current scenario is very much ideal for reducing the pledge and I think the promoters will make most of it.

Business wise, the removal of restrictions on export of paracetamol api wef 28th May looks good , as they are one of the largest manufacturers of paracetamol api in the world.

Discl:exited around buyback prices tracking dow Jones fall of 6.9% on Thursday. Looks like a bad decision. May buy again

1 Like

It is a good opportunity for promoters to get out of the pledge and make it a clean slate as already stated publicly by the cmd. That would also push up the share price to maintain the market capitalisation. Promoters need to ensure that they are absolutely transparent in their intentions and actions to sustain the improved market confidence in their company. No need to rock the boat at this stage.

Side effects of Covid have started troubling business in terms of increase in prices of raw material imported from China and expenses towards additional safety measures in addition to hike in transportation cost

- PAP, a KSM for paracetamol has seen increase of around 27 per cent

- Logistic cost including sea freight & air freight charges have seen sharper increase.

- Additional expenses towards safety measures are Rs 6-7 crore every month

- Four-fold increase in logistics costs and other expenses

I am not sure if management can pass-on anything other than material cost to their customers (I know that they do it with a lag)… if not then certainly it will have an impact directly on bottom line

4 Likes

Buyback is complete as per latest filing.

Received bid for 142 cr, and appro 100 cr of cash is not used. It is interesting to see how Granules intended to use it going forward. It will be better if they strengthen their balance sheet with the remaining cash.

Promoter has surrendered around 80cr worth of shares. So this will help them reduce the pledge going forward.

2 Likes

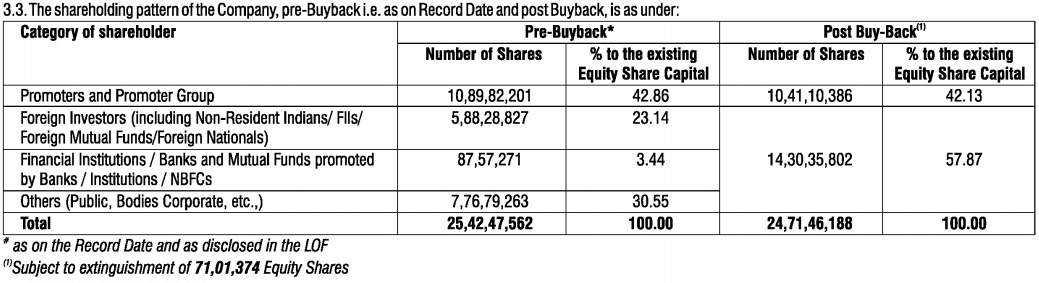

The share Holding details after the buyback are following

As the trading price moved above buyback price, it was a known point that buyback will NOT attract shareholders. It is evident from mute retail participation as well.

Interesting point to note is that even promoters have participated in calculated manner protecting their holding in the company to highest possible level. It is a positive indication that management is willing to grow the business rather sell it off (few months back there were such rumours that promoters are exploring options due to succession issues)

As the business has turned cash flow positive, promoters pledge getting reduced to almost zero or lower single digit percentage, D/E ratio reduced to comfortable levels and improved EPS due to buyback should help Granules and make it re-rating candidate. Let us see how markets respond to such developments.

8 Likes

Promoters walking the talk… buyback money helps them in releasing pledge… Now promoters group has pledge level at 8.64% (Mr Krishna Prasad has 10.43% pledge on personal holding)

Note : % level will change post buyback details are filled with exchanges

In this regard, Mr Krishna Prasad Chigurupati Chairman and Managing Director said "As communicated earlier, I am in line with the timelines committed to reduce my pledge of shares. The pledge was made earlier to fund the share warrants that were taken to fund the Capex of the company. I will be clearing the rest shortly and will remain committed to future growth and development of Granules and remain bullish about our business ability to create long-term shareholders value”.

2 Likes

Good interview where confident mgmt highlighting the differentiators of Granules .

Quality of questions is better at Bloomberg

3 Likes

Once again the pattern continues and FIIs increased their holding by 1.25%. This quarter saw around 7000 retailers joining the pharma run (interestingly % share holding of retailers has gone down. Buyback participation by big Retailers could be a reason)

Overall approx 1.25% holdings changed hands mainly from Retailers to FIIs

Promoter holding has reduced by 0.73% during buyback.

Current SHP

4 Likes

GOOD NOS FROM GRANULES. valn still OK. disl invested

1 Like

Even at this price the stock is undervalued. If the management can guide for maintaining the margins and the previous guidance, the stock deserves a re-rating.

2 Likes

Q1 Concall

- Strength of Granules - backward integration of products, different way of manufacturing, regulation

- Current level of production is around 130% - 140% of similar duration of last year

- Expect bottom line to grow 30% from last year

- Q1 Ebitda was 25%… normal guidance is 22% but expect it to be around 23% considering current scenarios

- GPI contributed 11% in Q1 topline, which was less than management expectations. They expect GPI revenue to grow 4 times in next 3-4 years in absolute terms

- FCF was low due to increase in receivable as sales are higher & 2.4% increase in inventory

- Finished product inventory : Increased from 200 Cr (Q4) to 260 cr (Q1)

- Metformin (750 mg) recall - 15 cr accounted in Q1… as product recall is still in process… some part may reflect in Q2 & Q3 as well (but very minimal)

- Recall of Metformin (750 mg) is expected to increase in demand for Metformin (500 mg)

- Regarding some concerns regarding paracetamol in Europe - management received multiple queries in last few weeks but denied having any issue in their products

- R&D expenses will go down in percentage terms but absolute nos will increase to ensure strong pipeline for future growth

- Maintain R&D expense guidance of 150 cr per year

- Target atleast 5 products per year in US, overall 7-9 (ANDA & other regulatory fillings) per year

- Capex will be funded by internal accruals, Remaining FCF will be utilized for buyback

- Future capex investment is in more complex products, which adds more value to company

- Board discussed sharing it via dividend but decided to preserve cash due to uncertain global conditions related to covid

- Only concern in near future is china dependency - we have 3 KSM dependent on China, worked on 2 KSM and finalized alternate source of procurement out of china (working towards reducing dependency on china)

- Company observed price increase for one of KSM in recent past & part of this is passed on to customer

- Rest of the pledge will be removed in near future

- Formulations are the highest margin product… API the least

- Our Onco facility mentioned has multi API facility and one Oncology block - expect revenue generation in near future

- Core molecules have contributed 85% & it will be around 75% in next 3-4 years

- Exploring new geographies including Europe, South Africa

- Europe & South Africa have lesser margin than US but more consistency

- Canada has better margin than US

- In new geographies, we will supply to others who will sell in local markets

Disc : I may have overheard or misinterpreted discussions. Please consume it considering this

22 Likes

Great summary mrai74. Adding more colours from couple of other dimensions from earnings call, earnings presentation, results and past events

1- There seem to be more deep-rooted involvement from the new generation promoter - Priyanka. She did answer many questions in the earnings call, and her answers gave confidence that she is detail oriented - articulated her views clearly on operations, business strategy and financials.

2- 11% of topline came from GPI (US Subsidiary), and per comments from promoters this would get quadrupled in three years. Add to this that GPI focuses on high margin products (can see it in the earnings presentation). Putting both these points to together - the company is going to show higher profitability in near to medium term.

3- ‘Granules is a manufacturing company in Pharma business’, Mr. Krishna Prasad has said this many times in the recent past. Let us go one level deeper to understand what it means. 85% of topline of Granules comes from 5 base products ( Paracetamol => Pain and fever control, Ibuprofen => Pain control, Metformin => Blood sugar control, Methacarbamol => Muscle relaxant, and Guaifenesin => Chest congestion control). These salts do not have a complex chemistry, and they are first defence medicines, and thus used in volume. In volume game optimal manufacturing processes through continuous improvement (Kaizen) is the game changer. Further, management explicitly said that they expect these five molecules would continue to contribute 3/4th of the topline over the next 3-4 years.

4- Onco block => the Vizag (unit V) facility is called Onco facility but it contains multiple blocks; one of the blocks is used for Onco. The Onco block has started producing APIs. Granules is not going to have its own Onco drug, rather they will supply APIs to other players.

5-Brownfield expansion of FD facility in Gagillapur => new block coming up with a multipurpose sustained release process. This process is used for complex molecules, so expect this to be ‘not’ used for five core molecules. The facility would be up in next 15-18 months. This should further give push to the margin.

6- Capex, Cash to cash cycle, and cash flow => 400 crores of Capex this year and about 300 crores next year. All capex through internal accruals. Cash to cash cycle has been reducing consistently => better sweating of assets. Free Cash (Cash flow from operations minus capital expense) generated in this quarter was 37 crores, but should move up in Q2 and Q3.

7- Would the demand sustain or we just saw a pent up demand in Q1? The management explicitly said that they expect the demand to sustain. It does make sense because (again) company does not derive major business from specialized drugs but from five first defence medicines.

8- So what is Granules competitive advantage? It does seem their manufacturing process, backward integration giving cost advantage, and their deep rooted penetration in the market with their core five molecules. The management also seem to be walking the talk => reduced debt, free cash flow generation, buy back and pledge reduction, and transitioning the business from API to FD.

9- What are main risks? Regulatory risks (FDA and other regulatory bodies), over-dependence on five simple molecules for most of the business, raw material (crude) price increase disrupts the profitability and dependence on China for one KSM (Key Starting Material) which is for their main product.

In the last three years Granules has doubled its topline, tripled its profit, reduced debt considerably, and become a free cash generating company. Can it repeat this performance for the next three years? I am not educated enough to even guess, but based on the little knowledge I possess, it does seem that there is fair possibility of repeat of this performance.

Cheers,

Krishna

PS: I know very little, and market had reminded/humbled me enough number of times. I may have heard/interpreted things incorrectly - sorry about that, please verify from your end before you take my words. Not a buy or sell call, and I have strong ownership bias.

23 Likes

Great summary and interpretation mrai74 and kkrai. We are really fortunate to have professionals like you on this thread.

I feel that the company has made enough capex in recent past and with ongoing capex will continue to grow for at least next two years. Granules strongest point is its market in USA. It can turn into a problem if there are difficulties with USFDA. The company should therefore make sustained efforts to increase its market share in Europe and middle income countries.

Krishna Chigurupati has been a very competent entrepreneur and CEO. It is good to hear that Priyanka Chigurupati is coming along fine. For long term investors it is a very good news.

4 Likes

Iam invested in Granules and one takeaway mentioned multiple times is that we should look at Granules more as a manufacturing company than as a pharma company. We should keep expectations reasonable and not expect the company to be spending money on R&D and bring out blockbuster drugs. I would consider this company as a cyclical, where margins could be affected by raw material prices. I doubt if further process efficiencies could increase margins. However this company would grow steadily and safely.

3 Likes

My only concern is FCF generation.

In the last quarter they had mentioned their focus will be on FCF as majority of capex is done. But they have again come up with a new capex plan

The mgt mentioned that it will be left with little FCF post the capex so do you all think that debt levels will be reduced substantially from here?

Disc: Not invested

BP Equities Institutional Research: Q1FY21 Result Update

Company Name: Granules India Ltd.

(CMP: INR 264, M cap: INR 65bn, Rating: BUY, Tgt Price: INR 312)

Extraordinary performance; Positive outlook: Maintain BUY

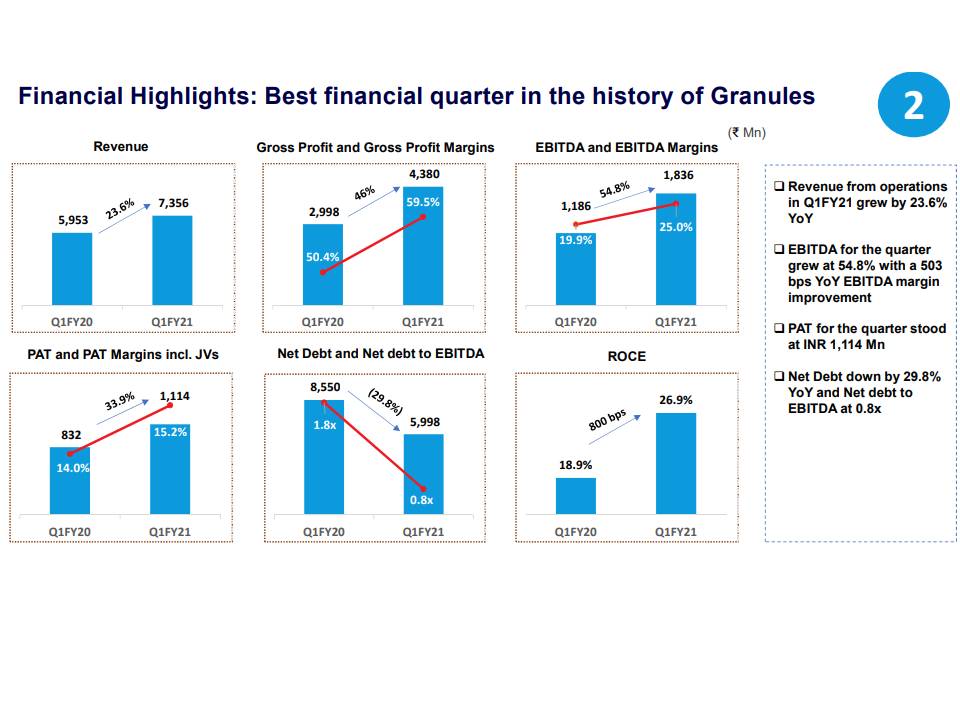

Granules (GIL) posted revenues of INR 7,356mn with 23.6% YoY growth, which was ~6% above our estimate of INR 6929mn. Revenue growth was mainly driven by new product launches and an increase in market share of existing products. Gross margin improved (918bps YoY) due to higher formulation sales (52% of revenue vs 48% in Q1FY20). Subsequently, EBITDA margin expanded by 503bps to 25% level was 475bps higher than our estimate. EBITDA was partially impacted by one-off INR 280mn related to metformin recall (INR150mn) and COVID-19 related expenses (INR130mn). As per management EBITDA margin can be sustainable (~23% for FY21) as continued traction in the formulation business. GIL reported PAT of INR 1114mn, was above our estimate of INR 744mn driven by strong operational performance and lower tax rate (25.3% vs 32% in Q1FY20). Management expects to achieve 30% PAT growth in FY21 compared previous year and 25% for FY22 given the strong traction in base business along with new product launches in the US generics business. Post the buyback of shares, the promoter pledge comes down to 8.6% (vs. 37.6% earlier) and expect to be zero by FY21 end.

☆ Formulation vertical to remain a mainstay of growth

Formulation segment contribution increased from 48% to 52% (YoY) in Q1FY21. APIs and PFIs contributed 29% and 19% respectively vs 36% and 16% a year ago. Geography-wise the regulated market contributed 71% to the revenue. Management expects approval of 4-5 high value and volume ANDAs in the next two years. Thus, guided for additional capex of Rs2.5bn to meet increasing demand. This facility will be ready by H2FY22 and will provide additional PFI & compression capacity with a payback period of 2-3 years. This project will be funded through internal accruals. For FY21, capex guidance stands at INR3.5bn and INR 3bn for FY22. We believe FY21-22 to be much better on a revenue front, on the back of ramping up of fresh capacities and expected 7-8 US generic launches in FY21 with addressable market size of ~USD2.5bn. During the quarter, GIL has filed 3 ANDAs/Dossiers in North America and European markets and received 6 ANDAs approval (including 1 tentative approval) from the USFDA. We modelled 19.6% top-line growth for GIL over FY20-22E as we believe most of the benefits from capacity addition and ANDA approval would be seen in FY21-22E. The company plans to file 20-22 ANDA filings from India and Virginia’s facilities put together over the next three years.

☆ Valuation & Outlook

Over FY20-22E, GIL is expected to post 19.6%/27.3%/ 23.9% revenue /EBITDA/ PAT CAGR with +20% return ratios. Considering the expected strong growth in profitability, healthy balance sheet and improving return ratios, we are optimistic about the long-term growth prospects of the company. At the CMP (INR 264), the stock is trading at 13x its FY22E EPS of INR 20.8. We keep our estimate unchanged and maintain our BUY rating with an upward revised target price of INR312 (earlier INR227) by valuing the stock at P/E of 15x (20% disc to 5 yr avg P/E) on Its FY22E EPS.

For disc ref: www.bpwealth.com/disclaimer

Agree with you !

When Govt is going all out to support API to take head on with China and when the entire world is rethinking their outsourcing strategy and when our API makers are receiving a lot of enquiries from overseas, it is prudent for all API makers to plan Capex… Liquidity in india is no issue at all…a lot of PE funds are flowing in…

API Capex is the need of the hour…

Look at Q1, 2020, when our country’s overall exports contracted by 12%, pharma sector exports as a whole grew by 10% in dollar term ( includes API )

Discl: Entered today in Granules @267…already invested in Divi’s… I see a great future for pharma/API makers in India…

It is not a recommendation…

I may be biased…I am not a Sebi registered stick advisor…

2 Likes