Any idea what’s the financial status of the companies where promoter group invests after pledging Granule shares

1 Like

2 Likes

Share Holding details ending Q4

https://www.bseindia.com/corporates/shpSecurities.aspx?scripcd=532482&qtrid=101.00

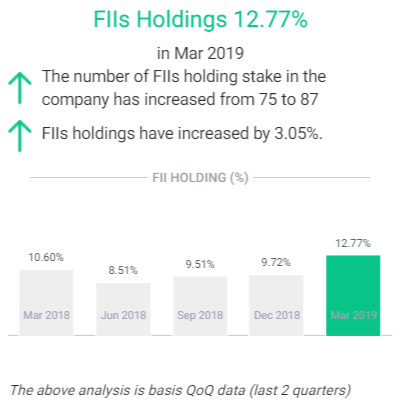

The major changes are KP selling almost 2% to reduce the pledge & big change in FII holding… seems KPs stake was bought by them.

1 Like

Results on expected lines

Granules_result.pdf (562.8 KB)

Granules achieved the growth on back of inherent stability of the molecules in their portfolio combined with their relentless focus on efficient manufacturing. The primary Revenue growth driver for this quarter was US formulation business, which complimented in overall improvement in profitability margins compared with same quarter of the previous financial year.

Owing to the policy offiscal prudence that they adopted, this year witnessed improvement in Debt profile, Working Capital cycle, and culmination of major capex implementation phase. They are geared up to leverage these assets to create value for stakeholders in long term. During the year under review, Granules along with US subsidiary filed 12 ANDAs, 2 DIV/F5 and 2 CEPs which are important indicators of their constant resolve towards accelerated product filling. The other turning point of the year was the launch of their own label product through US subsidiary marking an important landmark in their corporate journey.

Note from results is “Approved the resignation of Mr. K. Ganesh, Chief Financial Officer of the Company with effect from the closing working hours of May 14, 2019 and the Company is in the process of filling the vacancy.”

CFO leaving at this juncture is messy… we need to wait for concall to get more clarity

2 Likes

any idea why cfo resigned > with such a short notice (he is being relieved on 14th May) ? some one must ask this in tomorrow con call

It’s not a short notice. His last working day is May 14. He would ordinarily be on notice period.

But it’s always good to check on whether his resignation was routine.

Granules may be rerating candidate.

Nil observation on USFDA Audits validate quality aspects.

Promotors commited to bring down there pledge position.

Capex in tendum to Growth.

New Products filing & approvals.

Granules indicating successful transition from CRAMs to Formulation Player.

Improving in all aspects

3 Likes

Yes but the need to reduce debtor level and improve cash flows. Also lot will depend on oil prices. Granules management in the last call had guided for 25% PAT growth for next 2 to 3 years. i.e. estimate PAT of 295 cr in FY20. Can we assume it trade at 15x? If yes then we can see Granules trade at market cap of 4425cr. Upside of 53%?

APIs Cos are at sweet spot.

On Quality front there is no doubts post successful USFDA Audits.

Granules have adequate Infra, Capex Plan and Products Cycle that may give quality growth on consistent basis.

Management seems more firm & committed than ever before.

Main issue here is pledging and debt. Mgmt has told in last call by FY20 pledging should be gone.

I don’t think management ever committed this. I recall following

At some point they should think about generating free cash flow, otherwise valuation will never improve. Currently there is huge Cash burn every year.

1 Like

From Earnings call Q319

1 Like

conflicting statement in same Q3 concall

Did you listen to the Q4 concall? Plz let’s not speculate. Debt to EBITDA, fcf, pledge, capex, roce were all discussed with more clarity.

This time the management achieved what they had promised in 2018 Q4.

Running a growing business isn’t easy, so let’s allow them bandwidth but keep watching closely

As per interview on CNBC today, promoter mentioned following -

Pledge - They plan to bring down pledge from 42% to 32% in next 6 months (or 1 yr don’t remember exactly). And bring it to nil by FY21.

Debt - Debt to come down over a period of time. But for sure it won’t go up from current level.

1 Like

Where do you see speculation. The snippets are from Q3 concall & that is mentioned clearly in comments.

1 Like

have doubts still on why cfo karuppannan ganesh left - seeing his profile he is not a person who has left cos so soon in his past career - he has been a long timer in each prior job - he is leaving gi at a stage where it is time to reap the benefits including of some of his strategic initiatives - he spent just 2 years - so i am naturally having doubts as to why he left - did they ask him to do something which he felt would be dangerous or unethical ? but this can be clarified only by him and he will not do that to outsider - unless co comes out with more details than just a dull statement saying he is leaving for better prospects.His ctc was about 1.5 crs as per public information so unless he is getting a hugely better role (which we can anyways verify once we know where he is heading to ) …

3 Likes

How about the most basic reason- they just fired him for poor performance.

His articulation and grasp of the business did not impress me in the concalls.

1 Like