HDFC securities is bullish on Granules India

Seems that tough days ahead for Indian pharma companies exporting to US under Trump regime.

I feel the promoters are using their salary to pay interest only. It would be very difficult to try and pay the principal amount. But if the share price increases substantially, it would be easy for them to start selling some shares gradually and start paying the instalment of principal amount also.

1 Like

If I understand correctly, Indian pharma exports to US are approx 20% in volume and around 3% in value terms. It is a formidable competitive advantage in any market. With this kind of equation, even if Trump goes after pharma imports, it should actually end up benefitting Indian exporters. Americans are generally very focused on money and profit, including the Govt officials. In any case if Indian pharma companies maintain adherence to USFDA guidelines, they will always have competitive advantage.

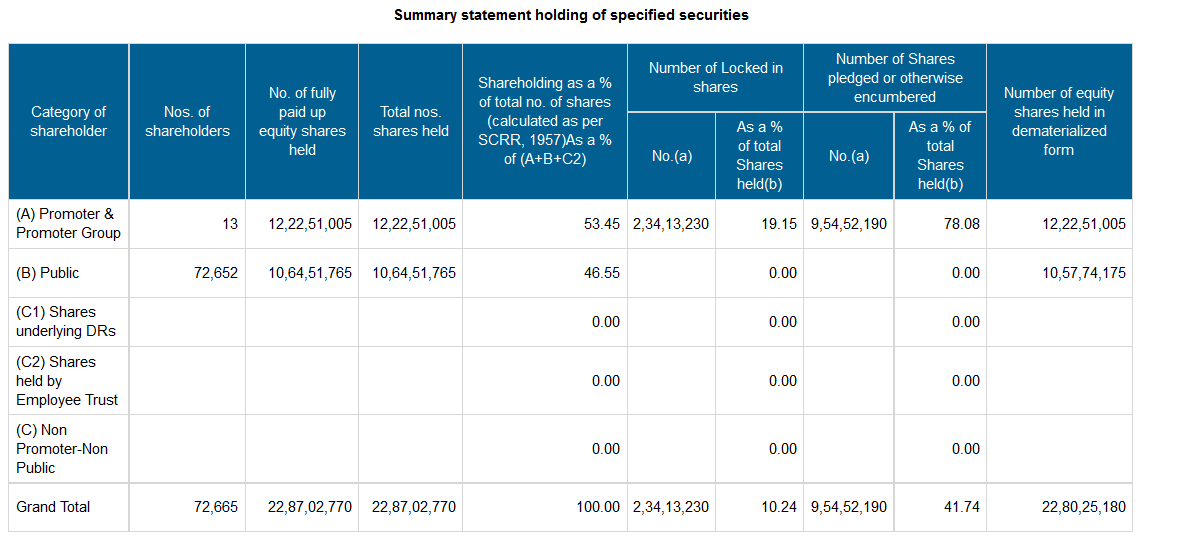

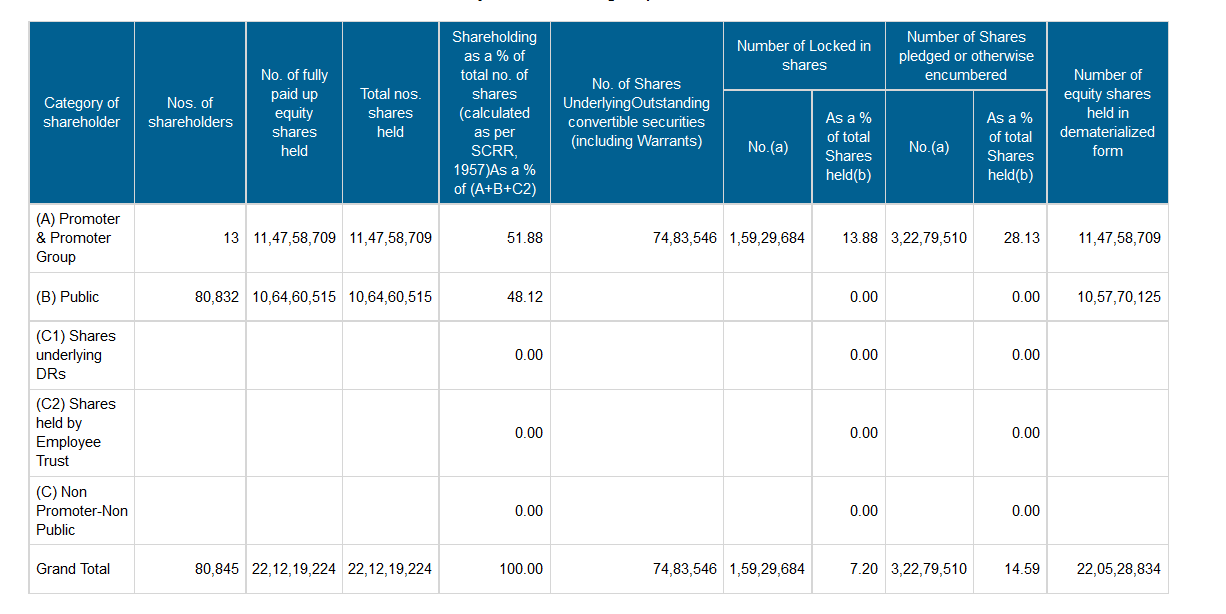

Can someone please explain what “Non Disposal Undertaking” means. Earlier disclosures had type of Encumberence as “Pledge”.

Also so does this mean now they have pledged all their shares? 12.43 earlier + 18.91 now = 31.34 ?

An NDU is an agreement where shares are transferred into a new demat account for the purpose of pledging. The beneficial ownership on the shares, however, doesn’t change and also the new entity (transferee) can’t dispose off the shares.

3 Likes

Promoter pledging of shares has increased from 28.13% to 78.03%. Promoter holdings increased from 51.88 to 53.45 though.

MAR17

DEC16

That means they bought more shares from Market and pledged most of their holdings? How should we take on that?

1 Like

As per bricks work ratings report on 20th March 2017 states that Company has proposed to issue the ncd of Rs.100 crores and as collateral, they must pledge their equity shares for 3.6X of NCD redemption value (includes principal and accrued interest) for the tenor of 3 yrs.

Disc: Invested

Investor Presentation

http://corporates.bseindia.com/xml-data/corpfiling/AttachLive/ff59c168-29d4-4e9f-95cf-527ace3e9517.pdf

2 Likes

Any one has attended the con call ?

Pls share some info about it

HDFC securities reiterates BUY…Target of Rs 190

http://hdfcsec.com/Share-Market-Research/Research-Details/StockReports/3022579

Granules India guides for a 20% Income growth and Rs 9 EPS for FY18

1 Like

Motilal Oswal latest report on Granules.

http://ftp.motilaloswal.com/emailer/Research/GRAN-20170511-MOSL-RU-PG008.pdf

Disc: Invested

Management could have gone for equity dilution, by sharing the opportunity with minority.

They will keep diluting it and increase their holding percentage till fy19, when their investments start giving returns so that they get to increase their holding around 140 to 180.

I could not figure out the reasons for significant expansion in gross margins. They have also exceeded their capex plans. This looks even more capex intensive biz now. Just hope there are no black swans as balance sheet is stressed for a good 2-3 yrs. Performance of JVs, ANDA filing and progress on complex molecules is heartening though.

Disc: Invested

Sumit… The cCFO of its CPAT of 10 yrs is at 1.3T +… They r gradually

improving their margins and reducing debtor days… And their sales to NB is

around 2…Almost all big pharma names are around this no… To flip the

debate, the industry has a high entry barrier… IMHO, one need not worry

about company collapsing due to stretched BS…

1 Like

Well, I wanted to say with high debt on balance sheet we don’t want any plant related regulatory accidents for the next two years. Else should be manageable given that their product basket provides basic needs.

as per managment they are very particular about plant and also since they are primarily B TO B THE buyers who are big cos they keep inspecting regularly so double check is there …

1 Like

1 Like