The adoption of ind-as 115 has reduced the NW of godrej properties by 33%.

1 Like

Godrej Properties Ltd

Highlights of Q1 FY19 results

-

Impact of IND AS 115

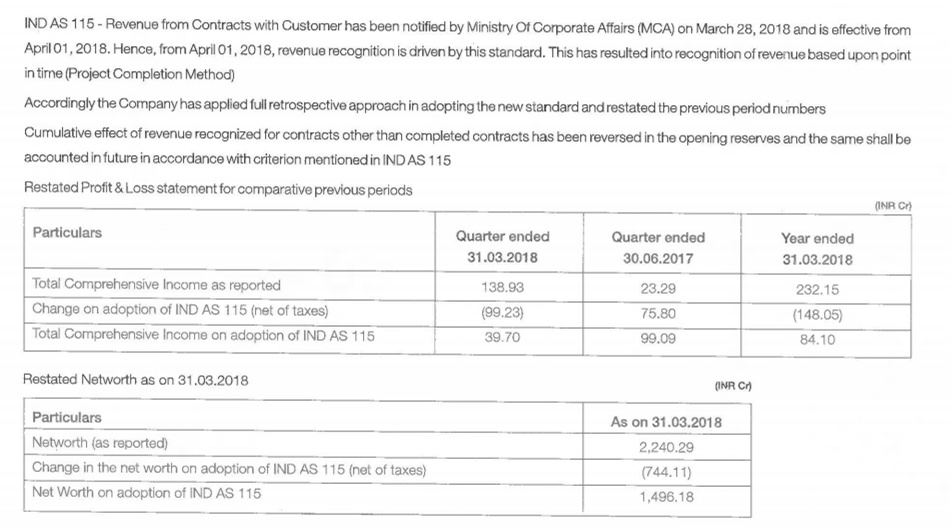

- Resulted into recognition of revenue based upon the Project Completion Method. Accordingly, GPL has applied the full retrospective approach and has restated the previous period numbers as well. The cumulative effect of revenue and profits recognized for incomplete contracts has been derecognized from the opening net worth and the same shall be recognized in the future in accordance with the criterion mentioned in IND AS 115.

- It will not affect the underlying cash flows of the business, so company will continue to focus on maximizing the present value of future cash flows. It will increase the focus on project completion and company have set the goal to reduce construction timelines by 25 – 50% and this new accounting standard will help bring additional focus to this important strategic priority.

-

Financials Under IND AS 115

- Revenue increase by 19% and stood at rupees 1,055 Cr.

- EBITDA increased by 22% to rupees 280 Cr and net profit decreased by 65% to rupees 34 Cr.

-

Key Highlights

- Total value of booking stood at 820 Cr compare to 1000 Cr mark from last 4 quarters. This is because of all new launches happening in the month of June and some of planned launches getting pushed out of the quarter.

- At Godrej Elements in Pune company sold 200 apartments in the launch weekend with a booking value of rupees 147 Cr. Godrej Meridien at Gurgaon saw sales of 115 apartments measuring 225,000 sq. ft. with a booking value of rupees 188 Cr. New project in Thane, Godrej Alive, witnessed a subdued response in the launch quarter with sales of just under 100 Cr, but company is confident of a pickup given the product and the excellent location. Company expect record breaking performance in the financial year.

- In June company has raised 1,000 Cr through a preferential issue. A GIC - managed investment firm invested the entire amount and company is happy to have a high quality investor like GIC take a significant position in company. Company will use the entire capital raised to fund the many growth opportunities across India’s leading real estate markets. Company already concluded 3 new development agreements and 9 new terms sheets in the current financial year.

- On execution front company has set its first precast factory at Godrej Golf Links in NCR, which will help to reduce the construction timelines and deliver a superior quality product.

Q&A

- What is the scenario in portfolio addition going ahead ?

- Company have three new development agreements and nine new term sheets so far in this financial year. The capital which company has raised through preferential allotment in the first quarter is intended to be deployed entirely for business development. It will be strong going forward.

- In Prijosha , the three projects which company have signed are JV or higher proportion of revenue share or they are primarily DM ?

- Company have signed definitive agreement on these three projects, as Pirojsha highlighted Company has not announce it because there are certain critical CPs which company is waiting for and they are at the final stages of completion. Two of these transactions are in very prime city centric locations in NCR, in profit sharing, high deposit profit sharing structures. One transaction is in Thane which is an outright transaction along with partnership with the GFM platform. So that is a kind of deal structure company is looking at. But largely it focuses towards capital deployment of the funds that company raised.

- Does the launch in the pipeline will help to achieve the last year number of Rs 6000 Cr plus sales ?

- If all the launches get done during the year then company will achieve the number Some of the projects are in advance stage of approvals . So company can get some upside from there.

- Kindly brief on the Rs. 744 Cr of net worth which has gone down, extra infusion capital raised. Bulk of it will be Trees but other projects which have been excluded ?

- bulk of it would be The Trees and then some of the BKC de-recognition and re-recognition will kick in. And there are several other JV projects which have not complied with the IND AS 115 standard which has gone into this Rs. 744 Cr de-recognition which will come back as and when company will able to comply with IND AS 115 condition

- Does the interest which company got from JV historically which are under construction will that company continue to recognize?

- Accounting will remain same . That is basis the cash flow deployed and cash flow received. So that accounting does not change, it is only the recognition of revenue and profit that is changing

- Is there any update on when does the development on the rest of the Vikhroli land parcel start ?

- Company have two projects One is on LBS Marg and the other one is on the Eastern Express Highway. So, both of those are being worked on at the moment. Company will launch it in next financial year.

- Will company have more focus on the Noida and NCR market going forward ?

- Company focus is on the top four markets in the country, so Mumbai, NCR, Bangalore and Pune. NCR is important and company is looking for adding portfolio there. But company is looking to do the same in Mumbai, Bangalore and Pune. So all four will see significant pickup in the current scale. And in all four now the strategy is to look on execution timelines being crunched and looking at that more holistically. NCR precast factory is the first one and that can manage the whole market instead of a single project. From this strategy company will roll out all over the country.

- In Mumbai due to new DCR plan it result in delay in project launches in Mumbai because it might take time to understand the new DP rules and regulations. So did the new launches will shift should pick up in second quarter FY19 ?

- Some projects are affected and some are not and the second half will have more launches across cities. But there will be no major change in result of it.

- Does the current sales number is satisfactory or company want to increase it ?

- Sales are as per plan because company have planned sales largely towards Q2 and currently company is running a major sustenance sales campaign called Happy EMIs on pan-India basis. So company will pick up the pace in the next couple of quarters .

- Kindly elaborate the Happy EMI scheme ?

- It is a part subvention scheme where the pitch is that you can own a Godrej Properties home at Rs, 9,999 EMI. The spin is basically that customers are paying EMIs which are lower than their rent. Now, these are all marketing aspects of the project. From a financial perspective the entire cost gets loaded on the price, so for company it does not end up paying anything extra from pocket.

- Is the opening of this precast a signal that company would change the strategy of just focusing on marketing and sales and leaving the construction to people probably who are best at it?

- One of the areas where the whole sector and company included is not really performing up to the mark is on project timeline. Because construction timeline in India even for the best companies tends to be 50-100% longer than global benchmark. So it is one of the key strategic priorities that is worth driving is ensuring that that gap is eliminated entirely. Company look that one of the way that it is best to do that is by looking at modern construction technologies like pre-cast. If it is executed well than there can be significant quality benefit, time benefit, especially because the requirement for labor which tends to be a little bit fluctuating in typical construction technologies is very low for pre-cast. From that company can deliver greater consistency, greater quality, greater predictability and much faster delivery. In a way, this new accounting standard dovetails quite nicely with this, because earlier there was a little bit false focus on this kind of 25% construction methodology which allowed company to recognize revenues but really was in no way meaningful from an actual operations or customer standpoint. Now focus is on actual delivery to make sure to take timeline down. both from financial perspective and churning capital quicker and generating better returns therefore and also from a customer perspective in terms of improved quality and lower delivery time. It is early days for company with the technology so company have to prove itself in term of delivery.

- Going forward does company is forcing contractors to use pre-cast or company will in-source construction for projects where the pre-cast would be?

- For the GGL project company have its own Pre-cast Factory. There are two part of it one is the production and other is erection. Even in GGL the erection still continues to happen through contractors, production is done in-house. And for other geographies company is evaluating different technologies like tunnel form or pre-cast. And then company want their contracting partners to go towards some of these technologies.

- Does company have formed up investment plans for Godrej 2 commercial and the Taj Hotel on the Vikhroli land parcel?

- For Godrej-2 company have partnered with fund management arm on a 50:50 partnership. The structure is now finalized and the project will be developed and leased. And only once fully leased, monetized. And Godrej Properties’ stake in that will be 50%. It has received significant amount of cash in the fourth quarter, fund management partners who will now also bear 50% of all remaining cost and Godrej Properties will also benefit from some development management fees and promote based on returns and so forth. So for that project financial structure is fully in place.

- In Hotels company is still exploring different options.

- How is the stress in the system going on ? Is it now more difficult for Godrej Properties to find deals in the market and have the negotiations or profit share reduced or increased currently as compared to 12 months ago?

- Stress has just mounted . Lot of NBFC and banks are under significant pressure themselves to recoup cash. Share of sales is going to the leading developers in most cities is continuing to increase. Infact stress has considerably increase in the last 12 months. Trend will pick up but it is difficult to predict the timing. of that pickup is what becomes quite challenging. But once the sector sees a pickup some of these trends of the sector consolidating and so forth are here to stay, because even in a better market most customers are going to be willing to purchase from the vast majority of developers and many financial institutions are going to be very comfortable lending, given some of the experiences in the last cycle. So some of the structural factors affecting the sector including consolidation will stay and Pace for that consolidation will be aided continued weakness.

- On construction and other outflows this quarter the spend has been around Rs. 850 Cr versus about Rs. 500 average for the last few quarters so does the it is a structural shift that company had made to a higher number ? Kindly elaborate on Rs 311 Cr land CAPEX ?

- Land CAPEX go toward Tree project and Godrej 2 which is a commercial project and several of other residential projects in Pune and NCR. So, this thing does not include only land, it includes land and land related approval cost.

- On Construction outflow as new projects are going into construction stage there will be an increased outflow which will happen on account of construction outflow. Also at this time company have grossed up the entire outflow for all the JV projects.

- What is the broad financial parameter used by company while deploying the capital ?

- IRR is the most important parameter . But company will intend to focus on a lot more into different scenarios and how these structures pan out under them. the profit-sharing structure is probably the most risk mitigated structure one can have and under these kind of higher deposit profit shares company share of upside from the project is also quite considerable. Company also look at the qualitative aspects in addition to the financials, like what is the specific location, how do those micro markets combine with company existing portfolio or cannibalize with existing portfolio, what is the upcoming infrastructure that can benefit.

- How company is looking at balance sheet and leverage progression moving forward ?

- Company will be comfortable between 1:1 to 1.5:1 from a gearing ratio perspective and that is a good combination of not overly stretching ourselves, while at the same time making sure that company is focused on growth and on capitalizing on the opportunities ahead . Company is eagerly looking to invest this capital where the balance sheet is currently certainly underleveraged and company look to make sure to capitalize on new business development opportunities in this year.

- Under IND-AS the profit which has reversed when it can come back ?

- These are all under construction projects. So within this financial year and next two financial years all of this will be recognized.

- Does the lender are looking at gearing differently because of this issue?

- It is only a change of accounting. The fundamentals of the business do not change, the booking value and the cash flow does not change. So, what lender is more concerned is whether the business is generating cash. That would be the prime parameter they would look at. So lender will more or less able to understand and there should not be any issue as far as the borrowing is concerned.

- It would be another trigger for consolidation in the sector and smaller players will be under even more pressure from lenders.

- Does company is acquiring something from an affordable perspective where company get a tax benefit ?

- Several projects of company will get tax benefit that has been extended for affordable housing. Lot of benefits are available for mid-income housing project. So lot of benefit can be captured within current setup and company is not going to launch any separate project for affordable housing but will keep an eye on it.

- On the IND-AS part, so is the development management revenue recognition, is that impacted by it anyway?

- It is not impacted, that remains same as it is because there company are the service providers, and when the service is complete, bills are raised it will get recognized

- On the Rs. 311 Cr land and approval related outflows, how much of this is for company existing project and how much is it for new projects ?

- For the new project it is quite low and more for existing projects. It is more towards the land and approval related cost.

- On net worth reduction of Rs 770 Cr What is the timeframe through which it comes back into P&L?

- All these will be come back within the next three financial years.

- How the persons or investors who are buying with their own money will react to the reduction timing of project completion to 25-50 % ?

- Reaction will be positive. But certainly the pressure on people’s cash flow etc. will be greater. Company will take care of that in terms of educating customers, in terms of signing payment plans and so forth. And of course, there is a big benefit to customers also in getting this quicker delivery, including investors who can then start getting rentals and so on. So overall it is certainly a huge positive for customers and a big positive for the company. As company will get visibility of company ability there will be some amount of education and tweaking of current practices that will be necessary to make sure that customers fully benefit from it.

- The strategy is very clear, there are two kinds of projects in the portfolio, there are projects which are very city centric, end user demand kind of projects and there are projects which are slightly more infrastructure led projects which could take longer horizon from an end user perspective. So, the choice of technology use is largely for end user driven projects, because end users do not mind, they actually prefer houses to be delivered early and Sobha’s Dream Acres project actually it has been major USP for their sales. So customer actually are quite positive if it is end user driven market.

- How company is choosing land location and what are the risk associated with putting more capital ?

- Company is very bullish on the overall macro story for the sector. Company have made few choices . The first is the geographies which company want to play in and there company have defined top four markets. The data suggests that about two-thirds of the value of real estate sold in India is sold in these four markets. So company can deliver leadership positions in each of these markets and company would be capturing a very large share of the overall market. Within those cities there are many different things to look at like financial returns . Company look at lot of qualitative aspects, including how the new project fits within company existing portfolio. is it likely to lead to cannibalization or is it likely to open up a whole new avenue of demand. Company look quite closely at city level infrastructure and how that is likely to impact various locations. So all these will remain in focus. Company has scaled both from a financial perspective and an operating perspective. there is a preference and a priority towards looking at better locations within each of the focus cities. Company will look for it by deploying more capital in the form of refundable advances. If the project get delayed or stuck for any reason than company will have more capital now deployed in some of these projects. Overall structure is risk mitigated.

- Why there was tepid response to that Thane project?

- Company had timed it wrong because by the time got the approvals and move ahead the rain come in Mumbai. In the first weekend company had cancel the launch because of major rain threat in Mumbai for that weekend. In second weekend company go ahead with the launch but the customer walk-ins doesn’t happen. So, biggest learning was not to push the launch in the rainy season. And the second thing was the feedback received from the customers regarding the possession timeline which company were mentioning very long. This is largely because this project was RERA approved and company was not having MOEF approval, this was a past approved project. And customers were not happy actually with the longish duration, given that is an end user market. So, the learning and feedback has been taken, company want to get all the construction started on the site and then re-launch this project. Company is very confident that when company will bring it back to the market it will get a good response on this one . Location is very strong.

- What is the location of company NCR and Noida project, apart from 150 and Golf Links in Greater Noida. ?

- Noida Project include GGL which is Greater Noida Township project and also have a project in sector 150 in Noida, two projects actually there.

- Does company signed any new project in Noida apart from these two ?

- Yes, one of the three new projects company mentioned is in Noida.

- Of the booking value of around Rs. 6,000 Cr, how much of that would be because of subvention scheme versus normal payment kind of plans? And any risk to the subvention scheme company foresee ?

- Company don’t have too much subvention schemes in the previous year’s numbers. Company have a strict policy on subvention, company is very particular about subvention and the amount. In subvention schemes , the investment by the customer is 15-16% because 10% he has to pay from his own pocket and there is stamp duty and registration which are 5-6%. Then the customer again has to invest another share of his capital somewhere during the middle. So company has to make sure that the risk gets hedged and company do not do those 1-5% subvention schemes in the market

- Minimum entry for an entry for a customer today on a subvention is 10%, and then immediately registration is done which is another 5-6% from his pocket so there is a lock in .

- Any update on the Mumbai market of the debris issue, any clarity, is it all sorted?

- There is a six months window currently open for approval . it will again be by the board, so there is no final resolution on that.

- What is happening on the ground in some of company focused markets ?

- Today there are 10,000 – 15,000 or more real-estate developers in the country. So all cannot exist in the market and in last few years the top 10 to 20 players in each city double their share of the market. But at an overall level that share is still quite low, so there is significant room to grow. Earlier company was having most of the project in partnership with land owners and now 80-90 % is with developers.

2 Likes

Companies which has short term debt liabilities are the most impacted by this liquidity crisis…godrej properties is one of them.

What’s your view on buy on dip?

1 Like

Cannot say for sure at what price it will be a value buy. RE is not doing well. Margins are falling, supply is plenty and the ground level economics is not helping the demand scenario.

The management is reputable. Ten-on-ten on that front. But the numbers are not good.

Debt is notable. Interest cost has been half of operating profits in 2018; in that respect the recent quarters have not been encouraging either.

I was doing my research in the RE sector recently and came across so many folks unhappy with Godrej products. They have taken up too many projects by lending their brand name. It seems they did not have bandwidth to take up these projects. Complaints regarding missed deadlines, poor quality of construction and failed promises are piling up. They have few flagship projects which are owned by them and they are doing well. I have actually interacted with quite a few in their non-Mumbai projects (Bangalore and NCR) and did not feel good. There is high probability that they are diluting their brand name by taking up projects of erstwhile chor developers. It seems they do not have full control over the projects.

Oberoi realty is way better player in my view and in the affordable segment Purva appears to be a rising star.

5 Likes

They have a very high current ratio as well. I wonder what are it’s implications in reality.

I really wonder about the interest level in this thread. It clearly seems a multibagger stock . All the key characteristics are there , here’s my list

a) A long runway of growth

b) From a reliable promoters house

c)Restructuring in the sector.

d) Consumers getting mature and bad players getting out

e) Godrej brand as a moat

f) Asset light model- tie-up with land-owners .Market the project with Godrej brand name,collect the money in advance , give it to builder.

g) Big potential , can keep growing despite with 3-4 competitors

h) All India presence. Weakness in one geography can always be compensated from other geographies

i) Proven track record

Would request senior boarders to please point out the negatives .There may be certain raitos or balance sheet issues but I feel people are caught up in too much analysis paralysis.

Disc: 25% PORTFOLIO. Entered 4 months back between 460-480 levels

1 Like

While godrej properties is one of the better cos in real estate with no liquidity issues, a lot of capital needs to be invested to generate good growth rates as far as real estate goes esp for large projects in good locations.

In my view, investing in real estate cos can be a good bet provided you find a co with really cheap valuations focused on cities where there are good job opportunities.

Best

Bheeshma

This is a seemingly a good company but as I live in Kolkata and having seen the 2 properties they have built here, it is difficult to take a positive view. The properties in Kolkata are relatively in poor locations, significantly overpriced and not selling well at all.

They do have a major advantage in Mumbai with their Vikhroli land parcel.

4 Likes

Even in Vikhroli, with exception of the Trees project, I believe the land belongs to godrej & Boyce and godrej properties is only entitled to a 10% or so development fee.

Q3 Concall Summary (source: capital market)

- Q3FY19 was the best ever quarter for residential sales in GPL’s history with total sales bookings in value for the quarter growing at 89%QoQ.

- Booking for Q3FY19 and 9MFY19 was 2.80 million sft (or value Rs 1528 crore) and 5.04 msft (or Rs 3155 crore) up from 1.43 msf (or Rs 1220 crore) and 4.79 msft (or Rs 4029 crore) in corresponding previous period.

- In Q3FY19 the company has added 1 new project with a saleable area of about 1 msft of prime office and retail space.

- Entered into a joint venture agreement with Hero Cycles and Godrej Fund Management to develop a prime office development on Golf Course Road, Gurgaon. Site is in close proximity to a multitude of established and leading commercial, retail, and residential destinations. GPL will hold 30% stake in project specific company.

- The company had strong launches across Mumbai, NCR, Bangalore, Pune and Ahmedabad. During Q3FY19, the company has 6 successful new project/phase launches across these 5 cities. Of these six projects two were new projects launches i.e. Godrej Reserves at Bangalore with a launch area of 1.92 msft and Godrej Air in NCR with about 1 msft. The balance four launches are all new phases of existing projects.

- The company delivered about 1.7 msft across 4 cities in Q3FY19.

- The company looks forward to building on this momentum as the company enters the final quarter of the current fiscal.

- In Dec 2018 the company has launched Godrej Green Glades, a new phase at Godrej Garden City in Ahmedabad after quite some quarters.

- Net debt as end of Dec 31, 2018 was Rs 1795 crore up from Rs 1539 crore as end of Sep 30, 2018 but down from Rs 3088 crore as end of Dec 31, 2017. The net debt equity ratio the company is comfortable with is 1-1.5: 1.

- Expect another launch by FY2020 at Vikhroli land parcel.

- Other income includes the JD interest income and income from mutual fund.

- Of current quarter top-line of Rs 340 crore, two projects account for majority of income of about Rs 255 crore of which about Rs 150 crore has come from Godrej Prakriti. About Rs 30 crore from commercial projects and balance from various smaller projects. In corresponding previous period about Rs 170 crore of sales came from BKC project and balance revenue from various small projects.

1 Like

Today saw the billboard in Pune from Godrej properties, that they booked 600+ flats in 2 days for the latest project.

I’d try not to assume information found on billboards to be hard-truth. Among billboards, real-estate billboards probably have the lowest truth per sq. inch.

7 Likes

Godrej is a trusted brand…They will be top 2 in all markets.Consolidation is happening. They sre in sweet spot in a business where trust is very low.

I just mentioned some information I observed today. The billboard for this particular society is there for sometime now in Pune and they may be trying to create sensation about the current project. But in the past I have read in some article (could not recall exactly where) about large no of booking in the initial days of the project announcement. So trying to make head or tails of this info

Realty firm Godrej Properties Monday said it sold 2,900 flats for over Rs 2,100 crore during the fourth quarter of last fiscal.

In a statement, the Mumbai-based developer said “it has achieved its highest ever bookings numbers in Q4 FY19.”

“The company sold over 2,900 homes with a total area of approximately 3.75 million sq ft and a booking value in excess of Rs 2,100 crore during the quarter,” the statement said.

The January-March quarter of 2018-19 was Godrej Propert …

I was looking at Godrej Properties and here are my thoughts.

- Since 2009, sales has grown 10x from 200 Cr to 2000 Cr while EBITDA has become negative and PAT has merely doubled.

- Most of the income is from ‘Other Income’. Maybe this is some sort of accounting thing, but if you look at PAT as well, the accounting PAT is still mediocre at best at 2x in 10 years.

- CFO since inception seems to be around -2500 Cr. So at an operating level, this business is poor

- With CFO itself deep in the red, it is redundant calculating FCF or looking at dividends.

- Return ratios are very mediocre, along with the sector

- Working capital management as well is poor due to the extraordinarily long inventory days, along with the rest of the sector

- Coming to valuations, how do you value this company at Rs.22000 Cr? At 10 times sales, 100 times earnings and about 10 times book, what exactly are you paying for here?

- Coming to the (so-called) asset-light nature of the business, the Fixed-asset turnover, has actually deteriorated in the last 3 years. Besides, is lending the brand-name really a reasonable business strategy? Sooner or later the quality issues are going to catch up and sully the brand name?

- The base rate for finding a good business is low in the real-estate sector and long-term returns have been very mediocre here with even the Nifty outperforming them.

- Last 10 year returns here have come from speculative growth than real growth. P/E has re-rated from 30x to 80x and PAT has just doubled, giving it a 4-5x return but even this is just about 14% CAGR. Buying this at 80-100 P/E, what are the odds for making even a similar return in the next 10?

I might be missing something very big that the market is seeing but I personally find it hard to justify even a 6k Cr valuation here due to the above reasons.

17 Likes

1.In the latest earnings call the management said that now they are able to get better deals ( in terms of JVs with the parties having land) than earlier. This may be attributed to tough regulatory environment which has forced out small players and also to easing land prices. It were the small builders, diverting funds from one project to another, who pushed the land prices to astronomical heights. GPL stands to benefit a lot if they are able to get good deals.

2. Given the failure of builders to deliver the projects in time , people are looking at more reliable names. GPL scores high on this account.

3. GPL has demonstrated very high execution ability.

Market is assuming that all this will cause exponential growth in GPL’s revenue and profitability.

Disc: Invested a small amount recently.