the 246 cr is the net worth of the co as quoted in their announcement yesterday. so in my view it is the kind of min valuation that the co has, how much it gets sold for is sth i have not checked. the press release also mentioned that they are setting aside 200 cr for buying out stressed asset. this amount and whatever they generate from the sale of godawari green will be additional. the bls sheet is getting develeraged.

1 Like

Book value of Godawari Green is Rs246 cr. It is likely to be sold around those levels (Conservatively believe).

the company will now be exporting all pellets that they produce as they have started production of high grade pellets which are in good demand currently and get premium pricing.

Now that Godawari Green will be sold, GPIL becomes a solely focused steel company with clean balance sheet. GPIL was perceived to be a conglomerate because of this solar power plant (unrelated diversification - a management error); hence GPIL always traded cheaper. Legendary Fund Manager, Mr. Bharat Shah has stated - a conglomerate will most likely be valued at a multiple of its weak business as markets get confused when there are different business segments. But now there is a scope of re-rating.

Management is rational and will undertake capex only with internal accruals (estimated free cash flows Rs600-800 cr per year based on normal steel cycle…currently Rs1200 cr per year due to strong uptrend in steel)

So i believe it should trade at an EV/EBITDA of 4-6 x of its Rs1000 cr estimated normalized EBITDA (current EBITDA run-rate is Rs2000cr per year).

Now few sequence of events to follow would be:

- Iron ore mining expansion (200 cr mining EBITDA additional will be generated)

- Expansion of billets, sponge (brownfield)

- Company becomes debt free and releases pledge (likely in Q1FY22)

- Next phase of greenfiled project/ acquisition of distressed assets

Also, now iron ore availability has improved a lot in Ardent due to the sourcing skills of the new partner. So expansion of pellet capacity at Ardent likely too…

Looks like exciting times. Steel cycle meanwhile looks sustainable with China going green, curbing capacities, phasing out export rebates.

Hoping for the best.

Disclosure: Invested

6 Likes

-

- Godawari Green EnergyAsia’s biggest solar-thermal plantInformation compiled and brought to you bywww.redocs.coImage source: Bloomberg

- 2. All copyrights to trademark(s) and otherIPR belong to their respective owners. Theinformation contained in this presentationis based on secondary research. No claim ismade towards accuracy of the data.6/17/2013 2www.redocs.co

- 3. Asia’s biggest solar-thermal plant• 50 MWe capacity solar thermal power plant• Started supplying electricity to grid on WorldEnvironment day 2013• India’s first solar thermal power plant underNational Solar Mission• Construction: Nov 2011 – Jun 2013• Status: Operational6/17/2013 3www.redocs.co

- 4. Location27° 36 0.36" N72° 13 24.6" ENokh Village,Pokaran Tehsil,Jaisalmer,Rajasthan, IndiaLand area = 150hImage Source: Google MapsSatellite view of the plant under construction6/17/2013 4www.redocs.co

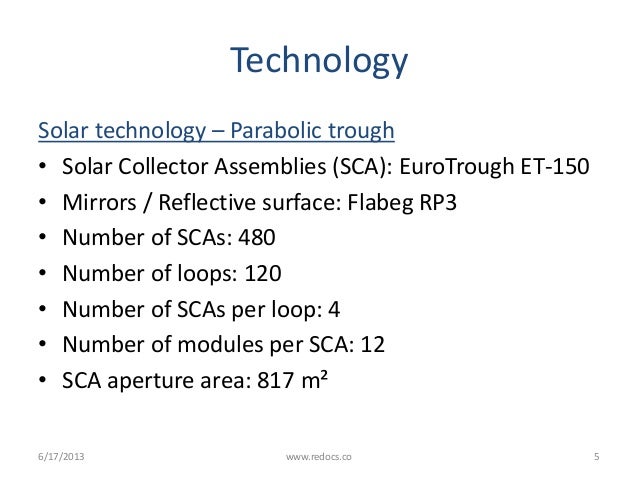

- 5. TechnologySolar technology – Parabolic trough• Solar Collector Assemblies (SCA): EuroTrough ET-150• Mirrors / Reflective surface: Flabeg RP3• Number of SCAs: 480• Number of loops: 120• Number of SCAs per loop: 4• Number of modules per SCA: 12• SCA aperture area: 817 m²6/17/2013 5www.redocs.co

- 6. Technology (contd.)• SCA length: 144 m• Reflecting area: 394 000 m²• Heat Collector Element (Tube): Schott PTR70Heat transfer fluid• Heat Transfer Fluid: Dowtherm A• HTF Temp in: 293°C• HTF Temp out: 390°C6/17/2013 6www.redocs.co

- 7. Image source:http://www.csp-world.com/sites/default/files/styles/x-large/public/map/images/xlarge_2926_a.jpgGodawari Green Energy CSP plant6/17/2013 7www.redocs.co

- 8. TechnologyPower Block• Steam Rankine cycle• Turbine Capacity (Gross) :50.0 MW• Turbine Description :SST-700, Siemens• Cooling Method :Wet coolingThermal Storage• None6/17/2013 8www.redocs.co

- 9. Participants• Developer - Godawari Green Energy Limited• Owner - Godawari Green Energy Limited (100%)• EPC Contractor - Lauren-Jyoti• Generation Offtaker - NTPC Vidyut Vyapar NigamLimitedDetailed list of suppliers on next slide6/17/2013 9www.redocs.co

- 10. 6/17/2013 www.redocs.co 10Image source: http://ww1.hdnux.com/photos/22/21/25/4789580/0/960x595.jpg

- 11. Suppliers• Schlaich Bergermann und Partner - Design, detailedengineering, tender documents, manufacturingsupervision, assembly supervision• Schott – Heat transfer element (tube)• Siemens – Turbine• Aalborg CSP – Steam generator• Paharpur – Cooling tower6/17/2013 www.redocs.co 11

- 12. Suppliers (contd.)• Suzler India – Boiler feed pump, HTF pumps• Flabeg – Mirrors• Ravi industries - HTF vessel, expansion tanks,deaerator• Flexim - Flowmeter for HTF• Dowtherm – HTF6/17/2013 www.redocs.co 12

- 13. 6/17/2013 www.redocs.co 13Image source: http://ww4.hdnux.com/photos/22/21/25/4789579/0/960x595.jpg

- 14. Commercials• PPA/Tariff Rate: 12.2 Rs per kWh• PPA/Tariff Period: 25 years• The project has also been registered in theClean Development Mechanism of theUNFCCC to earn Certified Emission Reduction(CER) credits• The project has overshot its budget by about20% reports Bloomberg6/17/2013 www.redocs.co 14

- 15. Visit us onwww.redocs.coyour personal library on REI would be bringing out an updated and very detailedversion of this presentation, to reserve your copy don’tforget to click on “Get in touch” below. Better still log onto www.redocs.co and subscribe to updates (right pane)

- 16. References• Energy

My valuation for GGEL:

GGEL has earned revenue of Rs.88.66 Crores and net profit of Rs.14.28 Crores for the nine months ended on 31st December,

2020.

If we extrapolate it for 12 months revenue comes at around 118.23 Cr. Average revenue had been around 90 to 100 Cr. If we consider annual revenue of Rs 90 Cr then we can safely assume EBIDTA of around Rs 80 Cr.

The PPA with NTPC is for 25 years w.e.f 17/06/2013 i.e around 8 years gave already elapsed and remaining PPA period is around 17 years. So NPV of Rs 80 Cr per annum for 17 years at discount rate of 10% comes to around Rs 640 Cr. (Debt of around Rs 350 Cr has to be netted off from this). I have considered terminal value as Nil

The Company will become debt free not only on stand alone basis but also at group level. The Company will have cash of around Rs 200 Cr with this transaction. The future cash generated by the company will be free cash flow without any requirement of debt or interest payment and can be channelized for future growth without raising any debt i.e the future growth will be self sustainable and not debt funded which will be a great positive for this stock.

3 Likes

Let me give a picture of what is about to come. Q3 eps was 45. Interest outgo is 36 Cr in Q3. If that interest outgo was 0 meaning say co was debt free then the Q3 eps would have been 55. Now with the uptrend in steel cycle the q4 EPs will be even with current debt 55-60. Let’s say 55. Debt is going down, there will be 2 quarters next year where it will be 0. The steel cycle has begun. So safe side one can expect 220 EPs for fy 22. Realistic should be 250.

At current price it means of PE of 4.

I don’t want to comment further.

4 Likes

@Rakesh_Arora Sir,

https://forum.valuepickr.com/uploads/default/original/3X/0/0/0019eaee239574a64a100c2b76da5ab9f048bbde.png

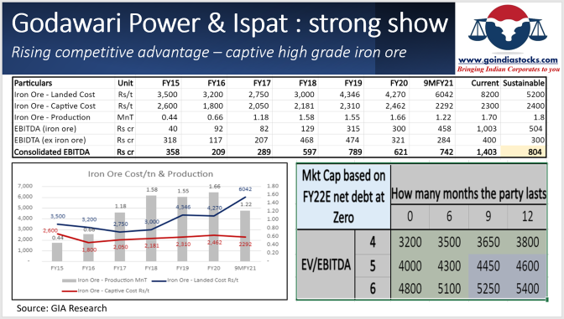

Can you please share the bifurcation for arriving at EBIDTA (Ex Iron Ore) of Rs 400 Cr at current pricing.

At current pricing I found your calculation to be very conservative. As per my calculation it should be at least Rs 800 Cr( at current pricing)

Rakesh sir has already shared the details

I have just copied and shared his link

@Rakesh_Arora, he has given consolidated figure of Rs 400 Cr for EBITDA (Ex Iron Ore) . I have requested him to give the details/bifurcation of this Rs 400 Cr because as per my calculation it is conservatively coming at Rs 800 Cr.

Hi, please note that Ardent steel will not be consolidated in EBITDA as holding has fallen to 37%, so that’s a loss of Rs70-100cr. It will be part of associate income. Secondly, once you take the profit of iron ore out, what is left is just steel conversion margin. Which currently is high but we are talking sustainable margin, so ultra conservative. Finally there is Rs90-100cr for power business.

We are not predicting actual profits, but what Godawari can make across cycles including downcycles

3 Likes

Got it , actually I was just working on EBIDTA for whole year at current pricing which as per your calculation is Rs 1403 Cr( Iron ore 1003+ Ex Iron ore 400)

Please note that this was done at the end of March. Since than pellet prices have moved up from 11500 to 15000/t now.

2 Likes

So effectively iron ore EBIDTA will increase from 1003 cr to 1300 cr minimum…

2 Likes

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

I know that many senior members of this forum have assess to the management of GPIL. With recent price run up, is it not right to go for stock split? I am sure it will also increase liquidity.

1 Like

The Company should think of splitting the stock in the ratio of 1:5 as the total number of equity shares are only 3.41 Cr with around 67.5% held with promoters. So liquid shares are only around 1.1 Cr. Its a good suggestion.

1 Like

Good news for godawari

3 Likes

https://www.cnbc.com/2020/12/16/as-china-australia-trade-tensions-rise-beijing-needs-iron-ore-alternative.html

China -Australia tension will keep Iron ore prices at elevated level.

61 per cent of China’s iron ore was imported from Australia in 2020, UBS found.

CRU Group principal analyst for steel, Erik Hedborg said reduced production in Tangshan, China had driven up prices.

This was due to China’s emissions crackdown in Tangshan.

“Recent production cuts in Tangshan have boosted demand for higher-quality ore and prompted mills to build iron ore inventories as their margins are on the rise,” Hedborg said.

Godawari Power valuation is proxy to Iron ore prices.

3 Likes

In recent months China has imposed restriction on a lot of Australian Imports including lobsters, wine, barley , beef and timber as part of the deteriorating relationship with Australia.

The geopolitical situation between Australia and China is only said to worsen with Australia hardening its stance against China instead of backing down.

This ban is extending to coal and LNG as well which were considered hitherto untouchable commodities, as they are essential to fuel china’s gowth.

Any retrospective ban or increase in duties/ tariff in iron ore might further sustain the iron ore at current levels or even increase the prices for a prolonged period of time.

The current pellet price is 16400 per MT. An increase of 1000 per MT adds about 40 cr to per quarter EBIDTA.

The EBIDTA in Q3 at 9000 per MT was about 347 cr so we are looking at a current quarterly EBIDTA with the increased prices (increase of 7400 per MT) at about 643 Cr .

We should expect stellar results from Godwari for FY 22. It not only helps pare off the debt entirely but also adds to significant cash reserves for future expansions. This should IMO lead to rerating of the stock as business metrics have changed.

7 Likes

It is definitely up for rerating as company will be debt free and will generate free cash from which expansion will take place, also another good announcement was company divesting its stake of its energy business which is low yielding and having a debt. It is possible that it can also move to high grade pellets or some special alloys to enhance margin.

4 Likes

NMDC announces revision of Iron Ore rates dated 12/05/2020:

NMDC IRON ORE PRICES.pdf (172.6 KB)

2 Likes