I have tried to look into possible areas of manipulation, fraud and mis-governance at GNA Axles and have assessed the company on the following dimensions:

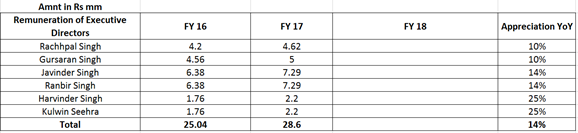

I. Mgmt salaries: As seen below, there is a 14% hike in mgmt salaries in FY17. Doesn’t look very high. I read in another VP thread related to triangulation (Forensics and the art of triangulation) , owner mgmt should take their due via means of salaries so that there is no incentive to manipulate and siphon money from the company in any other way.

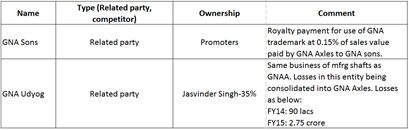

II.Subsidiary and RPTs:

-

Promoter Rachchpal Singh sold 5 crore property in Greater Kailash, Delhi to GNAA which is 50% amount back in 2015. Rest 50% is owned by Gursaran Singh. This place is used as guest house by the company. Fair value of this place was assessed at 10.5 cr in Nov’15.

This transaction does not indicate any red flag and there has been no RPT reported in FY17 AR. -

As far as subsidiaries are concerned, out of a total of 15 odd companies they have, most are dormant with negligible numbers, except GNA Sons and GNA Udyog. I will raise some questions about GNA Udyog particularly since it’s in similar line of business and is incurring losses. Satisfaction with respect to the nature of relationship with these 2 cos is very important:

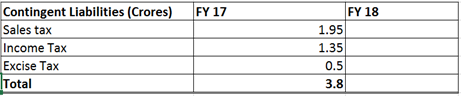

III: Contingent liabilities/off balance sheet items: Read in the same VP thread (triangulation), if a company has actual sales, it is bound to have sales/excise tax issues. As seen below, its contingent liabilities are all related to tax issues. Nonetheless, I will question the mgmt via email on how they are planning to resolve these issues since these have been pending for long (sales tax since 2014 and income tax since 2016) and the amount is material.

IV: Loans and advances to group cos/related cos: There are a couple of group cos (GNA Udyog and GNA GNA Sons) where promoters have made a “security deposit” of approx. 10 crore in 2014. Though they have not made any such deposit after that - meaning they have not used IPO money for this activity. (Could have been a major red flag for me at least particularly because this GNA Udyog is loss making). Nonetheless, in FY17 AR, there is a 1.5 crore addition to this security deposit which I will ask about in my questions.

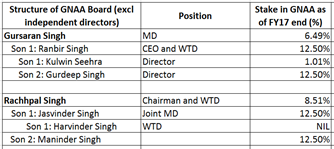

V: Promoter selling/pledging of shares: As of Dec’17, promoter shareholding is down to 65% from 70% till Sep’17. I will ask in my email about why promoters are divesting the stake. Will also ask about the Rs. 55 crore pledged shares as this would form about 9-10% of their holding. Promoter holding, though, is still high after all this so IMO there is no reason to worry unless this becomes a trend. Below is the break-up of ~65% in brief as of FY17 end:

VI: Dividend and taxation policies: Will ask them about dividend policy going ahead as till now they have not declared any dividends. Company has regularly income and other taxes as reported in the IPO prospectus and FY17 AR.

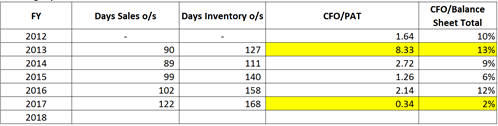

VII: Receivables and Cash flow position : This is one area where company has scope for improvement. Days sales outstanding has increased from 3 months to 4 months over 4 years from 2013. Out of the total receivables of 182 crore as of FY17, 161 crore is due for less than 6 months. Company should start providing for these receivables IMO which will be a good sign of conservatism. Their Operating cash flow position has also deteriorated a bit in 2017 due to high receivables and inventory. But the CEO has guided for 60 crore a month order book so I am fairly optimistic inventory position will improve. Will include in questions:

I will update the answers to all the questions here. @smant @rushikesh.k25

Based on what I have seen till now and shared here, I think there is still room for this company to grow in the coming 2-3 years and there are no major red flags at present to scare away investors.

Others may weigh in!